Section 1411 Business

Taxprepsmart How To Figure The Amount For Form 8960 Line 4b

New Sec 1411 Brings Difficulty Defining Real Estate Trade Or Business

Applying The New Net Investment Income Tax To Trusts And Estates

8960 Net Investment Income Tax 8960 K1 Schedulec Schedulee Schedulef

Why Section 965 Transition Tax Inclusions Are Not Subject To The Sec 1411 Net Investment Income Tax Taxconnections

Understanding The Net Investment Income Tax

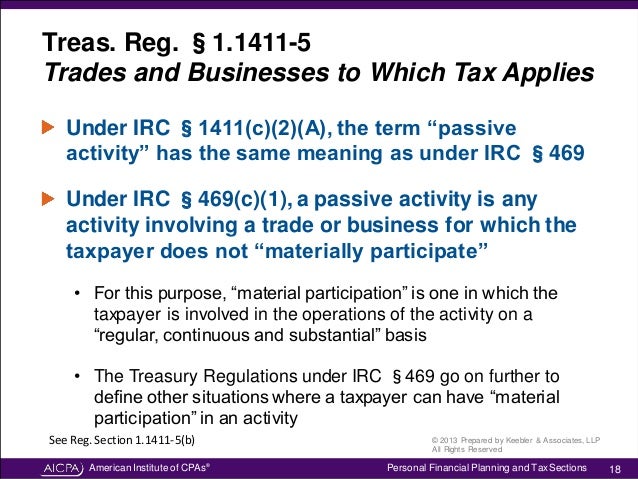

1 1411 1 d provides that the term trade or business when used by code sec.

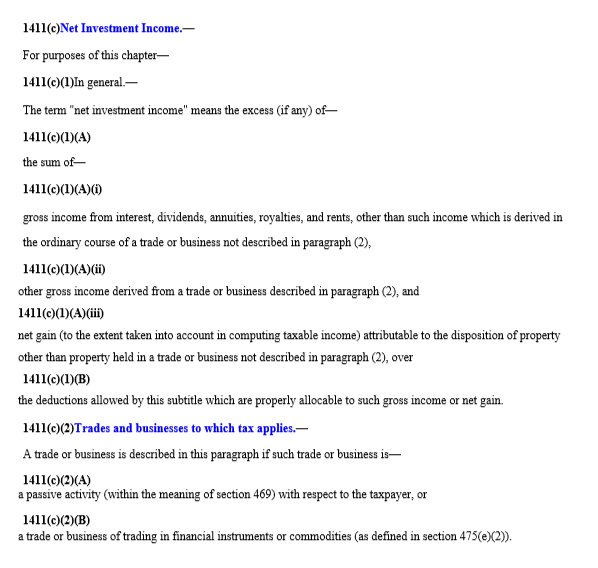

Section 1411 business. 3 income on investment of working capital subject to tax a rule similar to the rule of section 469 e 1 b shall apply for purposes of this subsection. For purposes of section 1411 and the regulations thereunder net investment income means the excess if any of 1 the sum of i gross income from interest dividends annuities royalties and rents except to the extent excluded by the ordinary course of a trade or business exception described in paragraph b of this section. Section 1411 of the irs code imposes the net investment income tax niit.

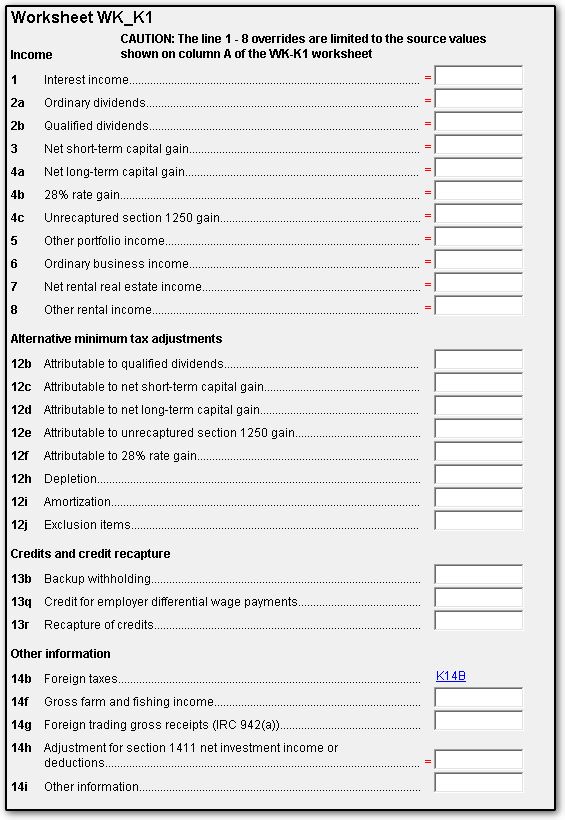

See section 1411 c 2 and regulations section 1 1411 5 a. On line 5 of the k 1 is the amount 2 814. Generally a trade or business that s either a passive activity for the taxpayer or is a trade or business of trading in financial instruments or commodities.

Questions and answers on the net investment income tax internal revenue service skip to main content. 1411 do not provide a definition of trade or business for taxpayers engaged in rental real estate activities and thus potentially subject to the tax on net investment income on income from these activities. Section 1411 c 4 states that in the case of a disposition of an interest in a partnership or s corporation gain is taken into account for purposes of the tax only to the extent of the net gain that would be taken into account if all property of the partnership or s corporation were sold for fair market value immediately before the disposition of such interest.

Taxpayers will be surprised by the breadth of the new. This tax which was further clarified in recently finalized regulations will affect many entities and taxpayers including s corporations and their shareholders. One of the more significant changes to the tax landscape in recent years is the new 3 8 tax on net investment income under sec.

On line 14 under other information the trust officer has code h section 1411 adjustment and then a negative number 2 814. 1411 brings difficulty defining real estate trade or business the proposed regulations under sec. 1411 and the final regs means a trade or business within the meaning of code sec.

Section 1411 trade or business. When i plug all this information into our return it shows the 2 814 as taxable income. There was no carryover from last yr.

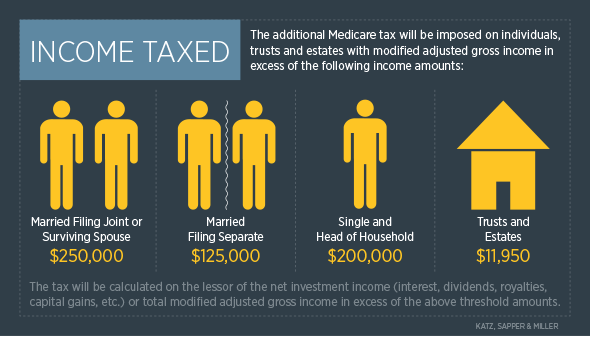

The Affordable Care Act And The 3 8 Medicare Tax Katz Sapper Miller

Planning For The Parallel Universe Of The Net Investment Income Tax

1041 Wkk1 Screen For Worksheet K1 K1

Baker Newman Noyes Section 1411 Self Rental Income

Https Www Claconnect Com Workarea Downloadasset Aspx Id 4598

Section 1411 Net Investment Income Tax Income Tax Investing Income

Directions Create A Tax Research Memo Based On Th Chegg Com

Trusts Can Materially Participate In Trade Or Business Wealth Management

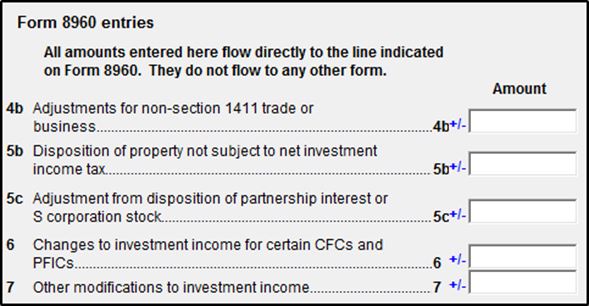

Knowledge Base Solution How Do I Change The Amount Flowing To Form 8960 Line 4b In A 1040 Using Worksheet View

Application Of Net Investment Income Tax To Section 453a Interest Blank Rome Llp Jdsupra

Https Www Drakesoftware Com Sharedassets Manuals 2018 Fiduciaries Pdf

Https Keitercpa Com Wp Content Uploads 2013 10 The Net Investment Income Tax 11 2013 Pdf

5227 Distributions