Irc Section 414 V

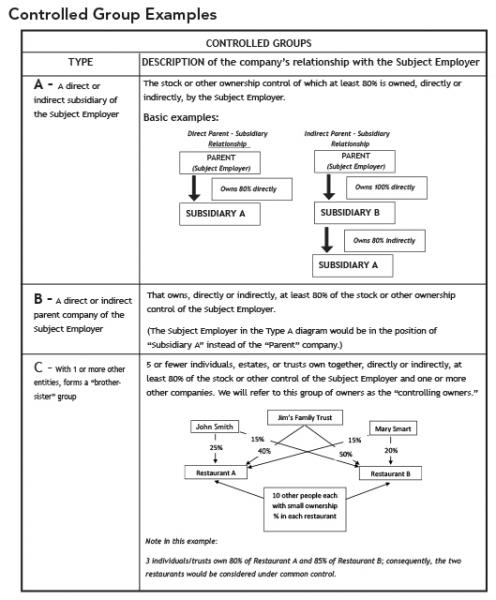

Is Your Organization Part Of A Controlled Group Common Controlled Group Basics Parker Smith Feek Business Insurance Employee Benefits Surety Northwest Beyond

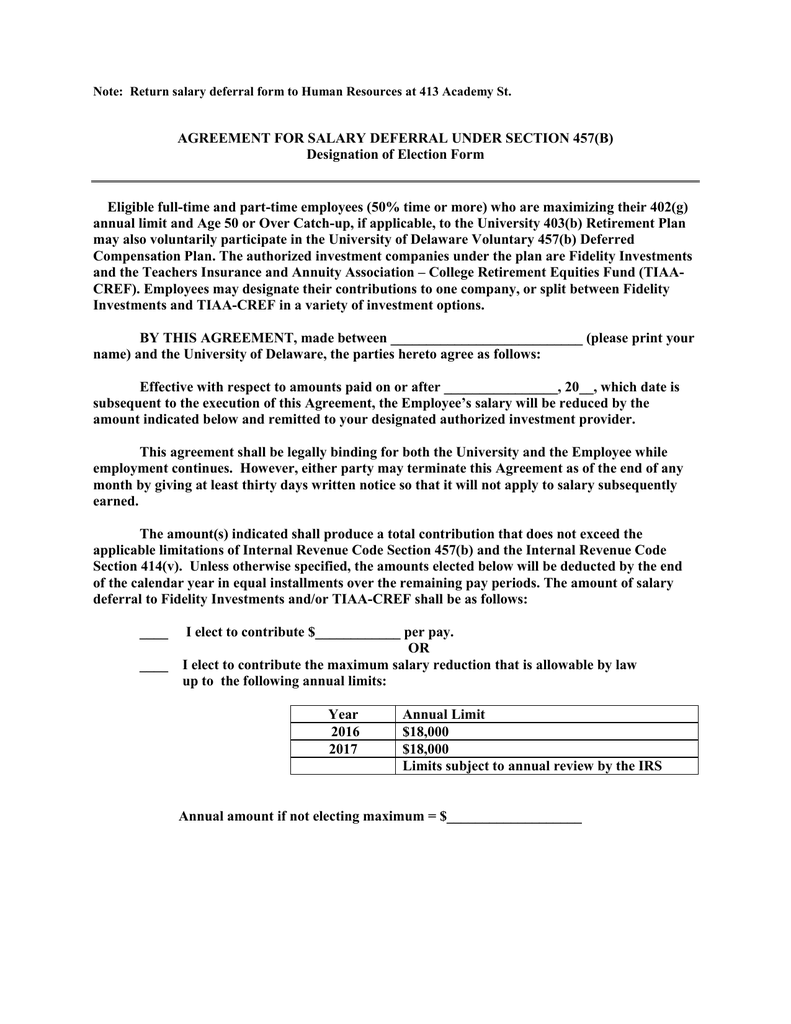

457 B Salary Deferral Agreement Manualzz

Https Persi Idaho Gov Documents Retirees Choice Plan Legal Document Pdf

Https Www Myfrs Com Complaints Dismissals 11 30 18 20 Dennis Sciullo Pdf

Tax Advantaged Retirement Plan Strategies For Small Businesses

Https Www Bradfordtaxinstitute Com Endnotes Irc Section 415c1a Pdf

Paragraphs through of this section apply to contributions in taxable years beginning on or after january 1 2004.

Irc section 414 v. Section 414 v applies to contributions in taxable years beginning on or after january 1 2002. 38 effective for years beginning after december 31 2001 permits an individual age 50 or older to make additional elective deferrals each year up to a dollar limit if certain requirements provided under that section are satisfied. In any case in which the employer maintains a plan which is not the plan maintained by a predecessor employer service for such predecessor shall to the extent provided in regulations prescribed by the secretary be treated as service for the employer.

International building code 414 6 1 1. Subpart b special rules statute sec. Irc section 414 plr.

Internal revenue code section 414 v definitions and special rules. Section 414 v added by the economic growth and tax relief reconciliation act of 2001 egtrra public law 107 16. For purposes of subparagraph a all plans maintained by employers who are treated as a single employer under subsection b c m or o of section 414 shall be treated as 1 plan except that a plan described in clause i of section 410 b 6 c shall not be treated as a plan of the employer until the expiration of the transition period.

A the plan was not a multiemployer plan because the plan was not a plan described in section 3 37 a iii of the employee retirement income security act of 1974 and section 414 f 1 c as such provisions were in effect on the day before the date of the enactment of the multiemployer pension plan amendments act of 1980. Section 414 v added by the economic growth and tax relief reconciliation act of 2001 egtrra public law 107 16. V catch up contributions for individuals age 50 or over.

38 effective for years beginning after december 31 2001 permits an individual age 50 or older to make additional elective deferrals each year up to a dollar limit if certain requirements provided under that section are satisfied. Location in internal revenue code title 26 internal revenue code subtitle a income taxes chapter 1 normal taxes and surtaxes subchapter d deferred compensation etc. Definitions and special rules.

Whether contributions made by employer a to plan x on behalf of its peace officers who are licensed by the board are considered contributions by an agency or instrumentality of state m or political subdivision thereof for purposes of code section 414 d and participation in plan x by such peace officers of employer a will not adversely affect the status of plan x as a governmental plan within the meaning of section 414 d. Part i pension profit sharing stock bonus plans etc.

Galicposam32017 Ex4b9

Irs Announces Adjustments To Retirement Plan Contributions And Benefits Limits For 2020

Https Home Treasury Gov System Files 131 File 2a Application For Benefit Suspension Exh 17 Redacted Pdf

Https Hr Msu Edu Benefits Retirement Documents Msu403bretirementplandocument Pdf

Http Ldsco Com Wp Content Uploads 2015 06 Non Elected Church Plans Pdf

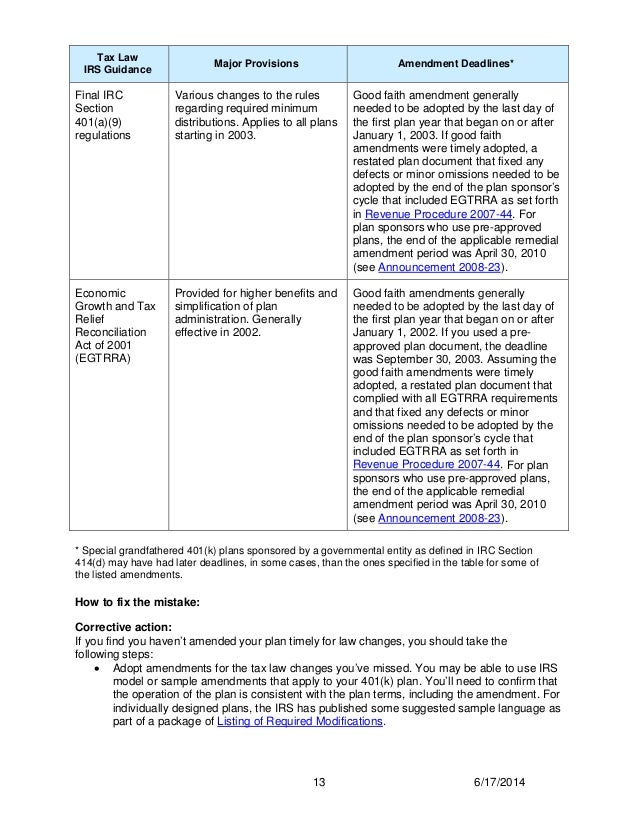

401k Mistakes Irs Updated 401k Fix It Guide

Https Www Scers Org Sites Main Files File Attachments 20191218 Item 13 Pdf

Http Louisville Edu Hr Benefits Retirementplans Uofl457bplan Pdf

Maximum Benefits And Contributions Limits For 2015 To 2020 Employee Benefits Legal Resource Site

Http Www Midvalecity Org Home Showdocument Id 2466

Https Www Stamfordpublicschools Org District Current Employees Files Term Sheet Ryan Fealey 2019 2021

401 K Plan Fix It Guide Pdf Free Download

Https Www Napa Net Org Sites Napa Net Org Files Plain 20language 20version 20of 20secure 27s 20mep 2c 20pep 2c 20and 20group 20of 20plans 20provisions Pdf