Irs Code Section 415

Https Www Bradfordtaxinstitute Com Endnotes Irc Section 415c1a Pdf

Https Www Asppa Org Sites Asppa Org Files Pdfs Acopa 2019 Symposium Materials Gs08 20irc 20415 20limitations Pdf

:max_bytes(150000):strip_icc()/Individual-Roth-401k-Plan-56a093553df78cafdaa2d8e7.jpg)

Are Catch Up Contributions Included In The 415 Limit

401k Mistakes Irs Updated 401k Fix It Guide

Mercer Projects 2021 Retirement Plan Limits Mercer

Flow Through Business Owners Line Up For Advice On New 199a Deduction Deduction Business Owner Internal Revenue Code

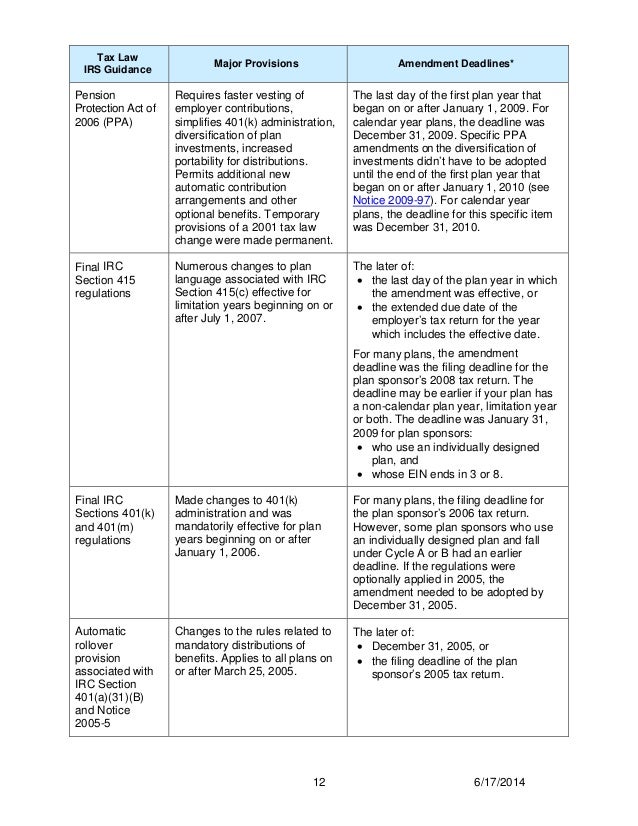

Section 415 limits the benefits that may be paid by defined benefit plans and contributions that may be made to defined contribution plans.

Irs code section 415. In the case of a plan which satisfied the requirements of section 415 of the internal revenue code of 1986 for its last year beginning before january 1 1987 the secretary of the treasury or his delegate shall prescribe regulations under which an amount is subtracted from the numerator of the defined contribution plan fraction not exceeding such numerator so that the sum of the defined benefit plan fraction and the defined contribution plan fraction computed under section 415 e 1 of. In addition to participating in the promulgation of treasury tax regulations the irs publishes a regular series of other forms of official tax guidance including revenue rulings revenue procedures notices and announcements see understanding irs guidance a brief primer for more information about official irs guidance versus non precedential rulings or advice. A trust which is a part of a pension profitsharing or stock bonus plan shall not constitute a qualified trust under section 401 a if i r c.

Internal revenue code section 415 b limitations on benefits and contributions under qualified plans. See 26 cfr 1 415 c 1 b 6 i a. In general employer contributions are not deemed credited to a participant s account for a particular limitation year unless they re actually made by 30 days after the period described in irc 404 a 6 for the tax year with or within which the limitation year ends.

Section 415 d requires that the secretary of the treasury annually adjust these limits for cost of living increases. Named for section 415 of the internal revenue code irc the 415 limit reflects the maximum allowable contributions to a qualified retirement savings plan in a given year. On april 5 2007 the irs proposed new regulations under section 415 of the internal revenue code irc as amended.

Under this rule the irc 415 b limits must be satisfied as of each annuity starting date considering the benefits provided or will be provided at all of the annuity starting dates. Other official tax guidance. Other limitations applicable to deferred compensation plans are also affected by these adjustments under 415.

Section 415 of the internal revenue code the code provides for dollar limitations on benefits and contributions under qualified retirement plans.

Https Files Nc Gov Retire Documents Files Retirees 415qebafactsheet Pdf

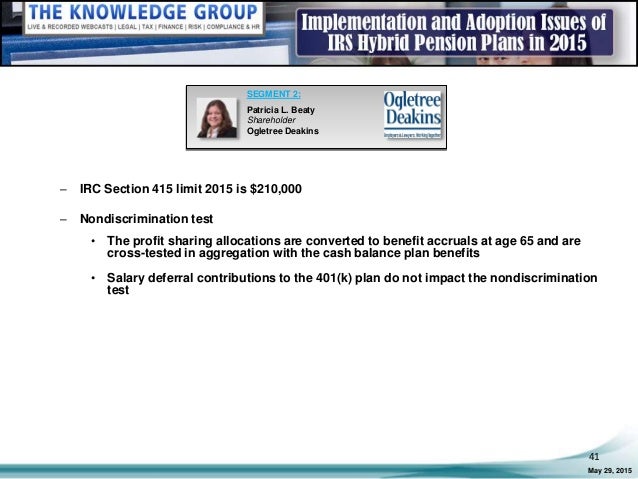

Implementation And Adoption Issues Of Irs Hybrid Pension Plans In 201

Http Ncsssa Org Qualifiedvsqualifying Pdf

Irs Announces Retirement Plan Limits For 2020

Http Www Menke Com Documents Menke Technical Issues Seminar 2010 Sessions 5 8 Pdf

Profit Sharing Plans Chapter 17 Employee Benefit Retirement Planning Copyright 2009 The National Underwriter Company1 A Profit Sharing Plan Is A Defined Ppt Download

Https Persi Idaho Gov Documents Retirees Choice Plan Legal Document Pdf

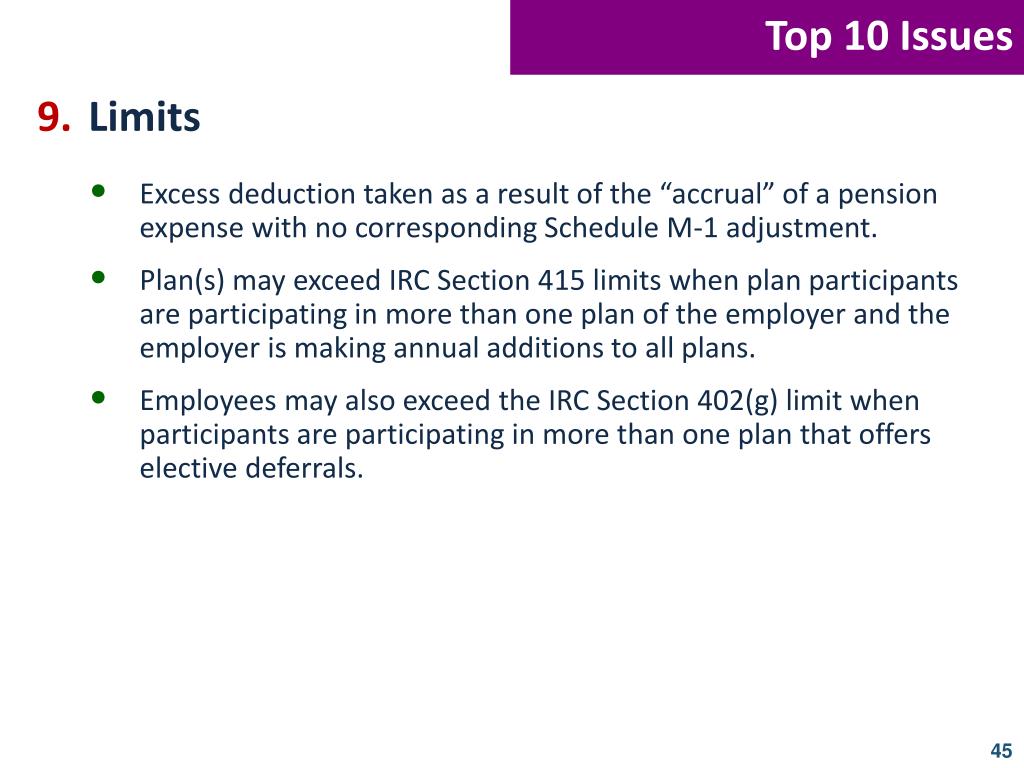

Ppt Audit Crossfire Powerpoint Presentation Free Download Id 826413

For Financial Professional Use Only Not For Client Presentation Ola Life Insurance In Split Funded Defined Benefit Plans Bill Schatz Regional Ppt Download

Https Www Soa Org Library Newsletters Pension Section News 2006 January Psn 2006 Iss60 Maclennan Pdf

Quick Compensation Primer The Basics Pension Consultants Inc

The Mega Back Door Roth Using A Solo 401k Plan My Solo 401k Financial

Mercer Projects 2020 Retirement Plan Limits Mercer