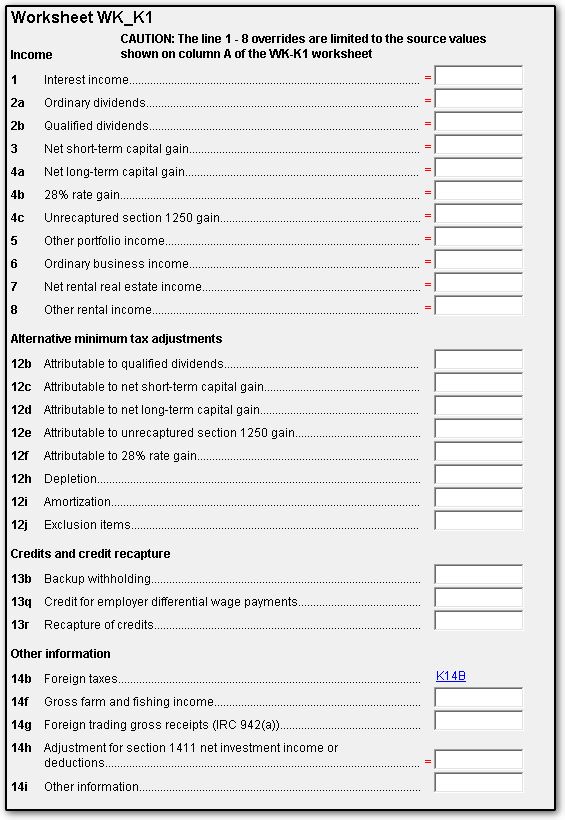

Section 1411 Adjustment On K 1

1041 Wkk1 Screen For Worksheet K1 K1

8960 Net Investment Income Tax 8960 K1 Schedulec Schedulee Schedulef

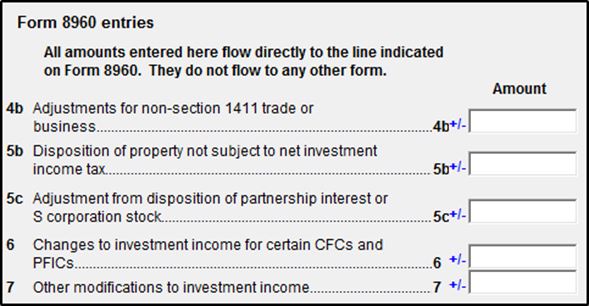

Knowledge Base Solution How Do I Change The Amount Flowing To Form 8960 Line 4b In A 1040 Using Worksheet View

Taxprepsmart How To Figure The Amount For Form 8960 Line 4b

I Really Like This One Bullet Journal July Cover Page Bulletjournal Bullet Journal Mood Bullet Journal Month Bullet Journal Inspiration

5227 Distributions

There was no carryover from last yr.

Section 1411 adjustment on k 1. It imposes a new 3 8 tax on net investment income of individuals trusts and estates effective for tax years beginning in 2013. The term net investment income shall not include any distribution from a plan or arrangement described in section 401 a 403 a 403 b 408 408a or 457 b. Schedule e part v line 42.

Schedule k 1 line 14 code f. Income entered on screen k1t is considered on form 8960. Section 1411 was enacted by the affordable care act in 2010.

The niit applies at a rate of 3 8 to certain net investment income of individuals estates and trusts that have income above the statutory threshold amounts. The niit applies at a rate of 3 8 percent to certain net investment income of individuals estates and trusts that have income above the statutory threshold amounts. Gross farm rental income.

The net investment income tax niit is imposed by i r c. Where do i put this amount on the receiving fiduciary. The niit went into effect on january 1 2013.

Line 14 h adjustment for section 1411 investment income amounts reported in box 14 code h represent the taxpayer s share of any adjustments to the net investment income of the trust or estate that occurs as a result of an election under section 1411 regulation section 1 1411 10 g to exclude certain income derived from the ownership of stock in a controlled foreign corporation cfc or a qualified electing fund qef. The net investment income tax is imposed by section 1411 of the internal revenue code. The schedule k 1 has a new code h in box 14 to report the amount of net investment income distributed to the beneficiary.

6 special rule net investment income shall not include any item taken into account in determining self employment income for such taxable year on which a tax is imposed by. On line 5 of the k 1 is the amount 2 814. Enter any adjustments to those amounts on screen 8960 taxes folder.

Pulse Model 39k Mobile Home Floor Plans Single Wide Mobile Homes Floor Plan Layout

My Technics Sl 1411 1978 Turntable Hifi Technical

Ulyssenardin Granddeck Rose Gold B Jpg 950 1411 Luxury Watches For Men Seiko Watches Timeless Watches

Nwt Slipper Socks Nwt Fuzzy Slipper Socks Despicable Me Minion Pattern Size Small Fits Shoe Size 5 1 2 7 1 2 K Fuzzy Slippers Minion Pattern Slipper Socks

Is Your Gq Needing That Flex You Ve Dreamt About The Lift You Need For Your Next Adventure Or A Fridge To K Superior Engineering 4x4 Accessories Nissan Patrol

20 1 3 Estimated Tax Penalties Internal Revenue Service

Bulletin Board Ideas Events Math Bulletin Boards Middle School Bulletin Boards Classroom Bulletin Boards

The Ladybird Blog Childrens Illustrations Baby Posters Cute Illustration

Pin By Kimmie G On Proud Uscg Sister Proud Army Girlfriend Army Sister Army Girlfriend

4264 Newberry Palo Alto Palo Alto El Cerrito Eichler Homes

What Is Form 8960 H R Block

Https S2 Q4cdn Com 170666959 Files Doc Downloads 2019 2018 Cedar Fair K 1 Instruction Booklet Pdf

Pin On Classroom