Section 338 H 10 Election Impact To Seller

(10).JPG?cbcachex=262393)

Gt S Quick Guide To Section 338 H 10 Elections Insights Greenberg Traurig Llp

Tax Issues To Consider In Common Acquisition Scenarios Ppt Download

338h10 Elections V10 31 16

Cft 2004 02 Corporate Franchise Tax Information Release The Franchise Tax Effects Of The Irc Section 338 H 10 Election Issued June 2004

Understanding The Section 338 H 10 Election Youtube

Buying Selling A Business Tax Considerations

This election applies to acquisitions of corporate subsidiaries or s corporations the election is made jointly by the acquirer and sellers before the deal is consummated and the seller bears any incremental tax cost from the deemed asset sale.

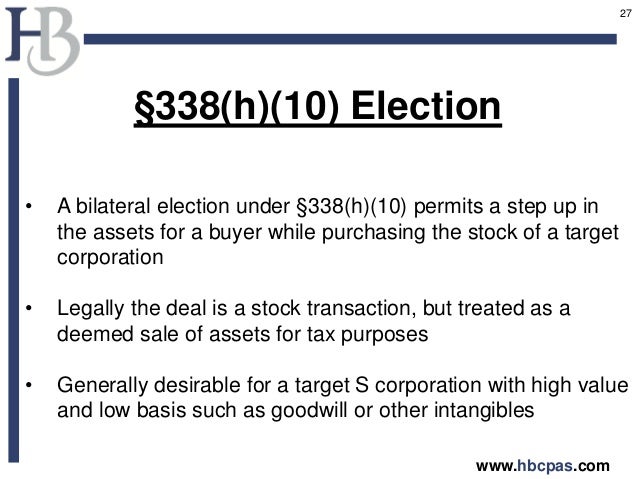

Section 338 h 10 election impact to seller. Section 338 h 10 internal revenue code section. As a result of a section 338 h 10 election a stock sale for legal purposes will be treated as an asset sale for tax purposes for both the buyer and seller. Gt s quick guide to section 338 h 10 elections provides you with a quick reference to understanding the 338 h 10 election when and how it can be made and its impact on buyers and sellers.

338 h 10 the section 338 election provides a particu lar federal income tax advan tage in transactions involving the sale of s corporation equi ty when compared to the sale of the c corporation equity. The section 338 election allows the buyer that acquires. Legal business and financing strategies.

As a result the 338 h 10 election is often a compromise on behalf of a seller in order to close the deal. Not admitted to the practice of law. If various conditions are met the election allows the parties in a sale of stock of a corporation to treat the transaction for federal income tax purposes as if it had been structured as an asset sale.

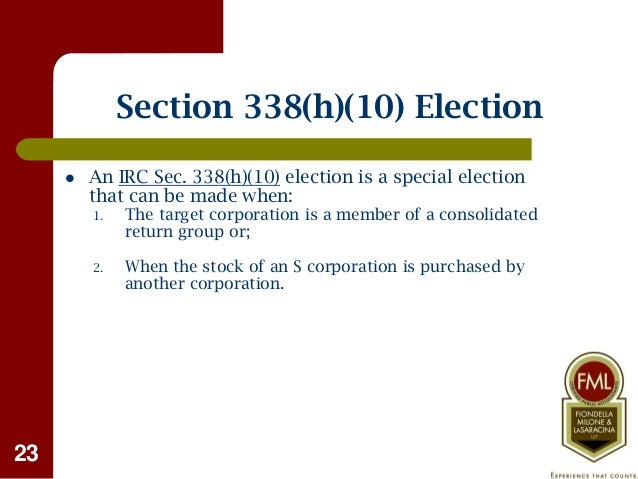

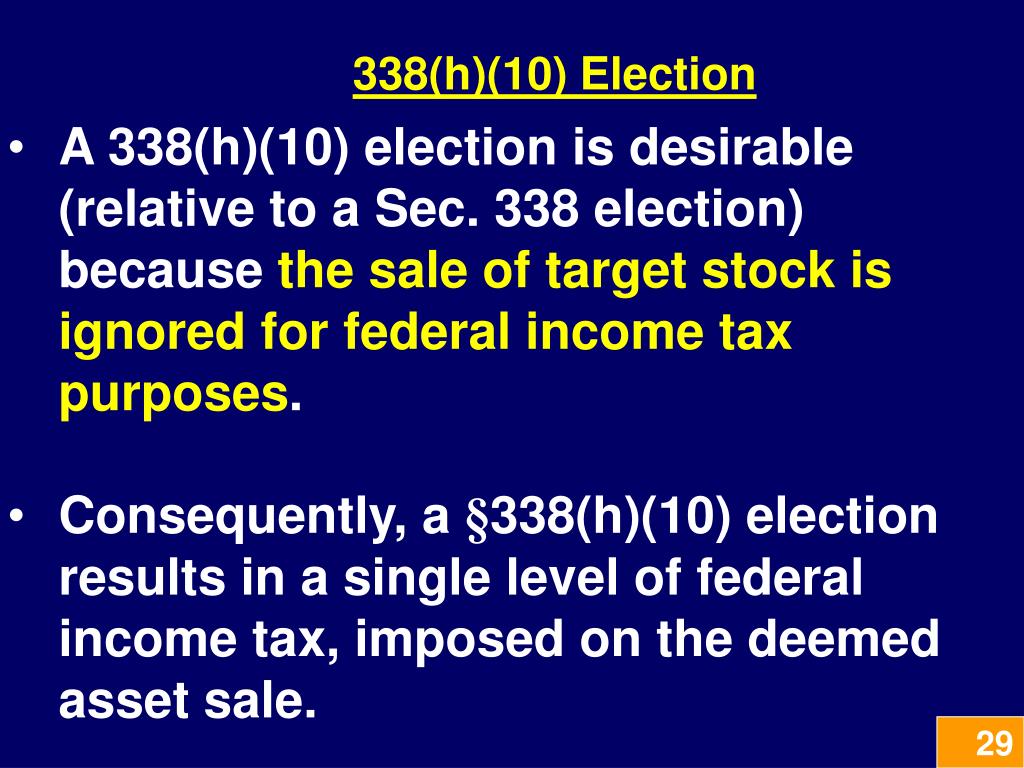

In a regular section 338 election two levels of tax are imposed. A section 338 h 10 election is jointly made by the purchasing corporation and the common parent of the selling consolidated group or the selling affiliate or s corporation shareholder s. Quick guide to section 338 h 10 and section 336 e elections 8 15 2016 roger royse upcoming webinar upcoming event june 9 12 00 pm 1 30 pm pacific time.

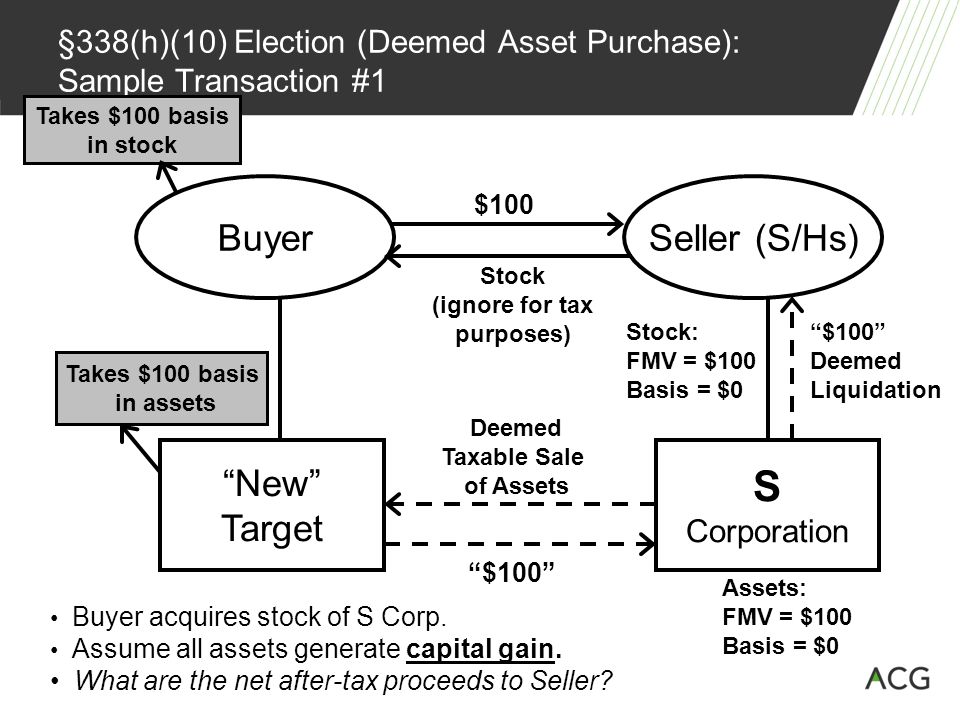

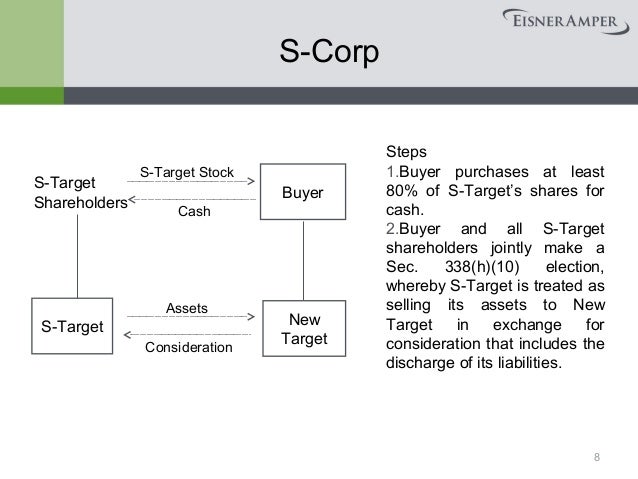

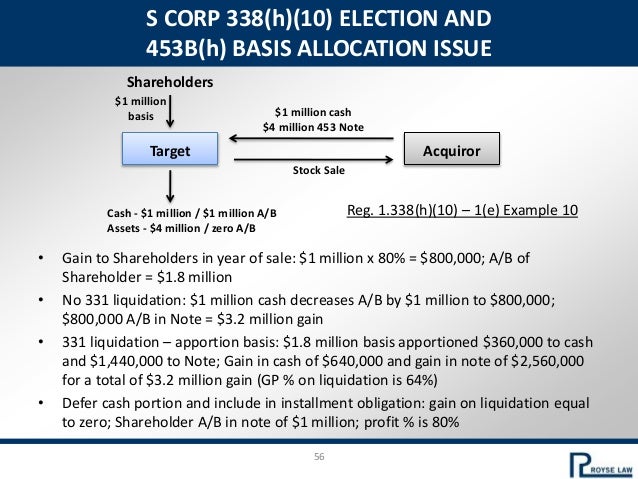

A section 338 h 10 election is a joint election that requires agreement between and among all of the selling shareholders and the prospective corporate buyer. Having said that as part of the negotiation sellers will frequently demand a higher purchase price in response to a 338 h 10 election as additional compensation to offset the additional tax burden they will incur. A section 338 h 10 election allows an electing buyer p and seller t to treat p as having purchased t s assets for tax purposes even though p purchased t s stock for legal purposes.

Special thanks to kathleen hooban for her assistance with this alert. One on the shareholders upon their sale of the target stock and the other on the deemed. Roger royse will make a presentation on startups in a down economy.

Tax Issues In Private Equity Venture Capital Aba Section Of Business Law August 12 2007 Julie Divola Jonathan Axelrad Pillsbury Winthrop Shaw Pittman Ppt Download

Section 338 Election Overview Asset Sale Tax Implications

Https Www Ftb Ca Gov Tax Pros Procedures S Corp Handbook S Corp Chapter 16 Pdf

Tax Consequences Of Asset Vs Stock Sales

M A Tax For 2019

Valuation Plays Key Role In Section 338 Elections Valuation Research

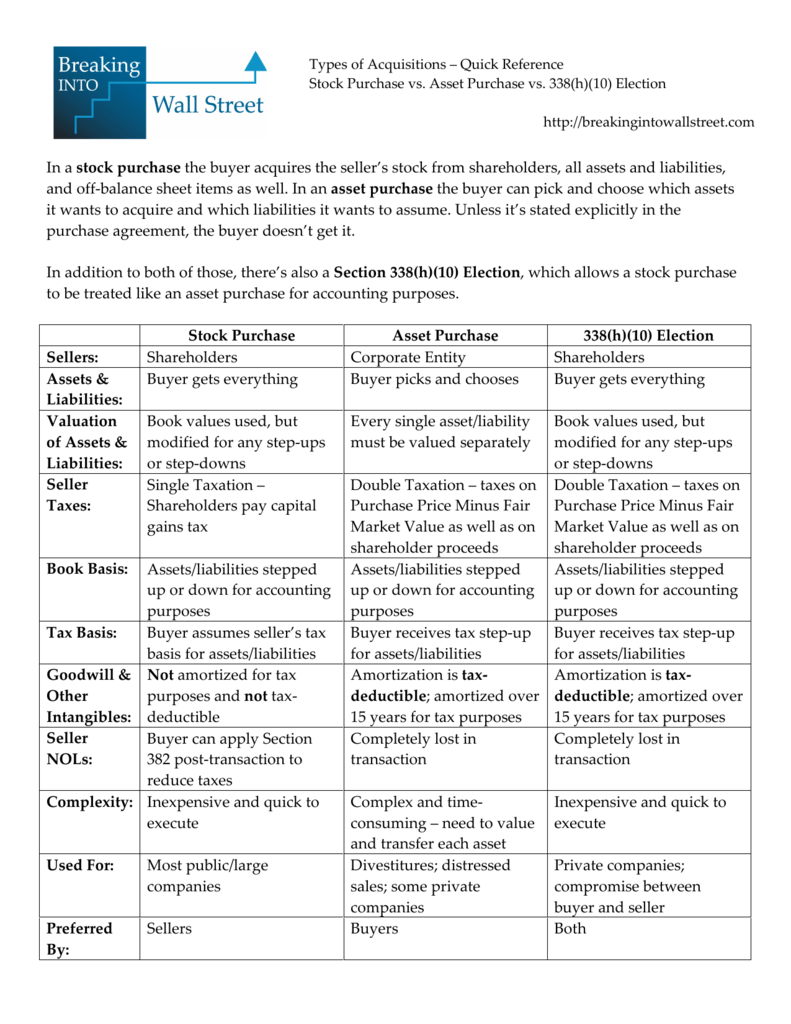

Types Of Acquisitions

Ppt Taxable Acquisitions Powerpoint Presentation Free Download Id 3850409

State Tax Matters

An Alternate Route To An Ipo The Up C Partnership Structure Part 1

Harvard Law School December 3 Ppt Download

338 H 10 Election A Negotiation Tactic

Robert Bushman Complex Deals Class 8 Ppt Download