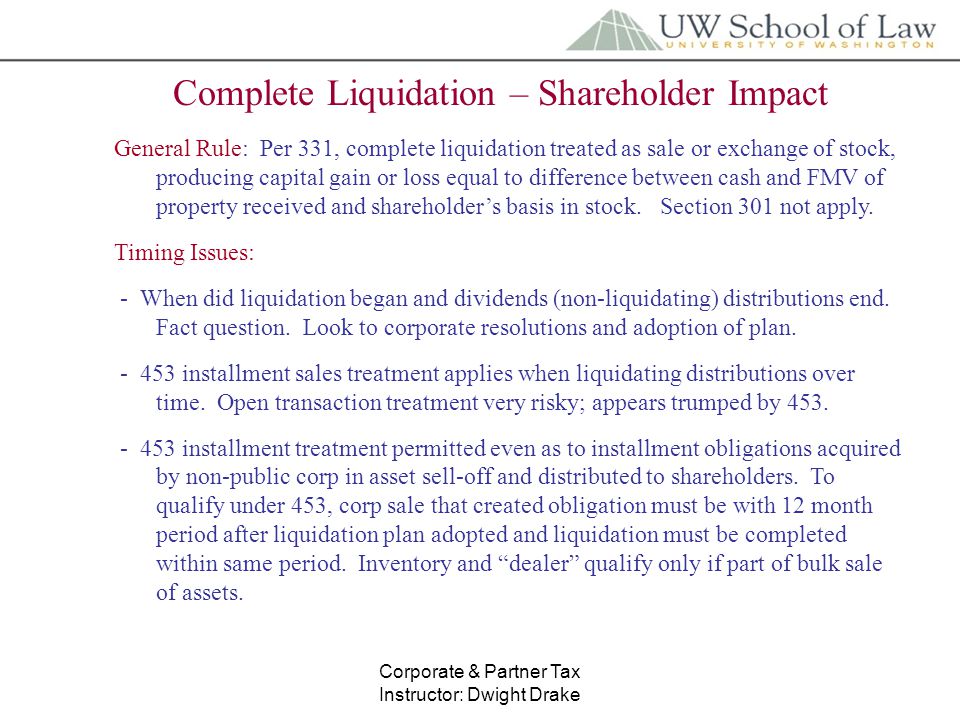

Section 331 Liquidation Distribution

Https Resources Taxschool Illinois Edu Taxbookarchive 2015 B6 Planning For C Corp Termination Pdf

Chart Of Rev Rul 90 76 Foreign Corporations Liquidating Distributions Of Usrpis International Tax Blog

International Tax Blog 331 332 Liquidations

Deferring Shareholder Gain By Distributing Installment Notes

Corporate Partner Tax Instructor Dwight Drake Two Liquidation Modes Corp Shareholders Corp Corporate Assets Stock Cancelled Straight Liquidation Mode Ppt Download

Https Www Ftb Ca Gov Tax Pros Procedures S Corp Handbook S Corp Chapter 15 Pdf

The irs mandates in section 331 a of the irs tax code that distributions of 600 or more must be reported on.

Section 331 liquidation distribution. For a complete liquidation section 331 a 1 provides for exchange treatment and section 1101 c requires the recognition of gain or loss on the sale or exchange of property. 331 a liquidating distribution is considered to be full payment in exchange for the shareholder s stock rather than a dividend distribution to the extent of the corporation s earnings and profits. 1 1966 except for certain liquidations to which section 332 of this title applies.

Section 331 contains rules governing the extent to which gain or loss is recognized to a shareholder receiving a distribution in complete or partial liquidation of a corporation. Often proceeds from cash liquidation distributions are reported on form 1099 div. Amounts received by a shareholder in a distribution in complete liquidation of a corporation shall be treated as in full payment in exchange for the stock.

The shareholder who treats the fair market value of the property as received in exchange for his or her stock also recognizes a gain irc section 331 a. The critical issue for tax planning is whether the assets distributed are considered property under irc section 336 and whether the corporation owns them. Section 331 contains rules governing the extent to which gain or loss is recognized to a shareholder receiving a distribution in complete or partial liquidation of a corporation.

Under section 331 a 1 it is provided that amounts distributed in complete liquidation of a corporation shall be treated as in full payment in exchange for the stock. G 3 of this section the amendments made by section 225 of pub. 88 272 do not apply if there is a complete liquidation of such corporation and if the distribution of all the property under such liquidation occurs before jan.

Gain or loss to shareholder in corporate liquidations a distributions in complete liquidation treated as exchanges. G 3 of this section the amendments made by section 225 of pub. 1 1966 except for certain liquidations to which section 332 of this title applies.

B nonapplication of section 301. For purposes of section 1248 a the term sale or exchange includes the receipt of a distribution which is treated as in exchange for stock under section 302 a relating to distributions in redemption of stock or section 331 a relating to distributions in complete liquidation of a corporation. Under section 331 a 1 it is provided that amounts distributed in complete liquidation of a corporation shall be treated as in full payment in exchange for the stock.

Tax 4022 5022 Federal Income Tax Ii Chapter 20 Dr Robert R Oliva Professor And Chairperson Department Of Accounting University Of Arkansas At Little Ppt Download

Determining Tax Consequences Of Corporate Liquidation To The Shareholders

Corporate Tax Copyright Ppt Download

Corporate Liquidation Corporate Distribution Shareholder Perspective Cpa Exam Reg Youtube

M A Tax For 2019

Https Www Ftb Ca Gov Tax Pros Procedures S Corp Handbook S Corp Chapter 16 Pdf

Ppt Taxable Acquisitions Powerpoint Presentation Free Download Id 3850409

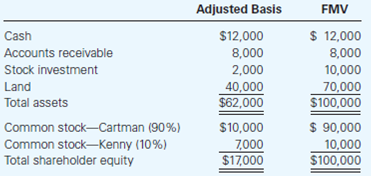

Solved Cartman Corporation Owns 90 Shares Of Sp Corporation T Chegg Com

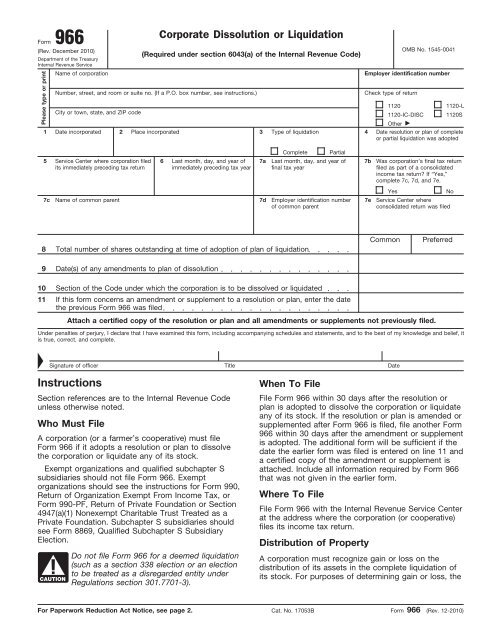

Form 966 Rev December 2010 Internal Revenue Service

Https Edens Com Wp Content Uploads 2018 01 Amreit 2015 Liquidating Distribution Pdf

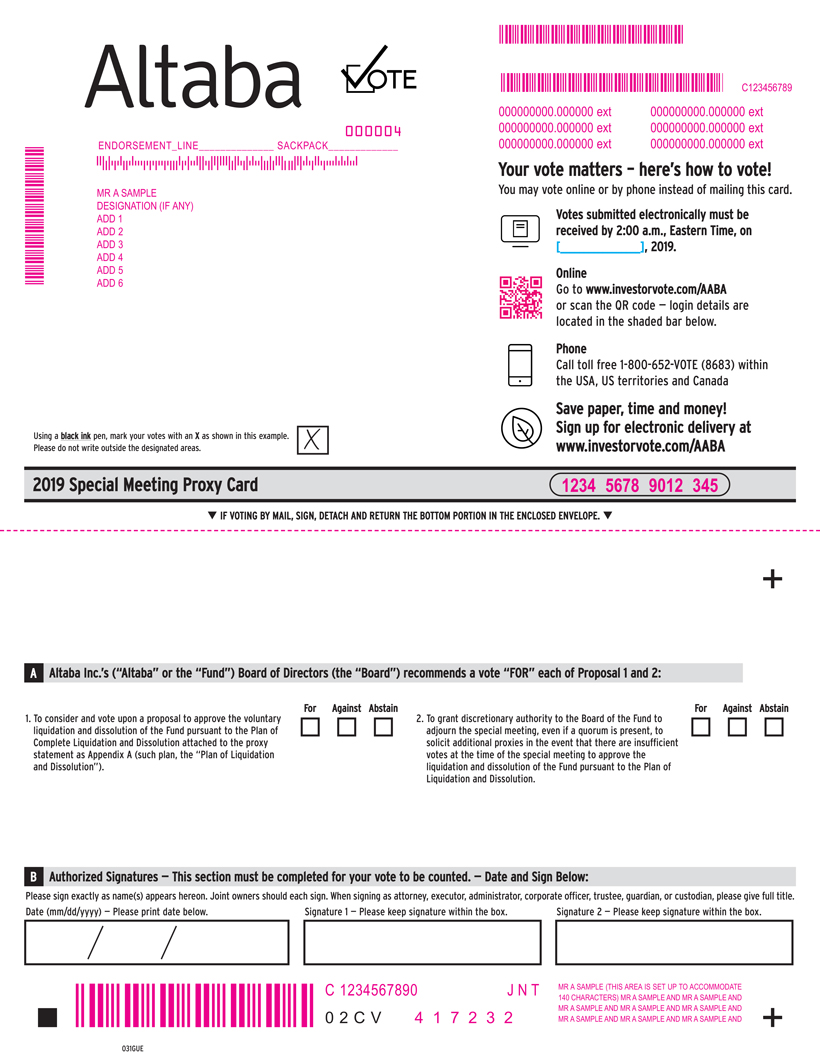

Pre 14a

/GettyImages-1072169588-bca5025d11374f30bf1fdc1c3c0cfe4f.jpg)

Cash Liquidation Distribution Overview

Tei 56th Midyear Conference Federal Tax Seminar Ppt Download