Section 338 H 10 Election S Corporation

(10).JPG?cbcachex=262393)

Gt S Quick Guide To Section 338 H 10 Elections Insights Greenberg Traurig Llp

338h10 Elections V10 31 16

Methods For Maximizing Value In M A Tax Structures

Buying Selling A Business Tax Considerations

Tax Consequences Of Asset Vs Stock Sales

Section 338 Election Overview Asset Sale Tax Implications

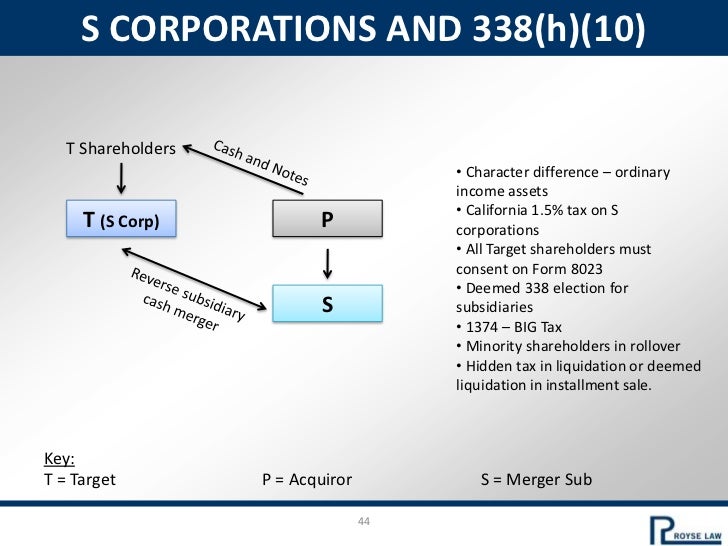

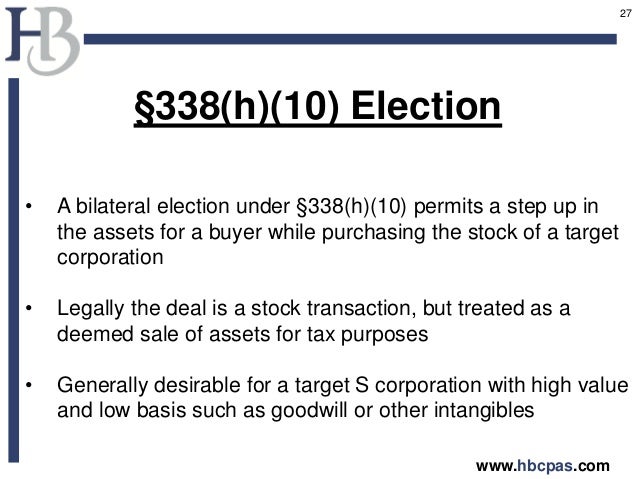

338 h 10 the section 338 election provides a particu lar federal income tax advan tage in transactions involving the sale of s corporation equi ty when compared to the sale of the c corporation equity.

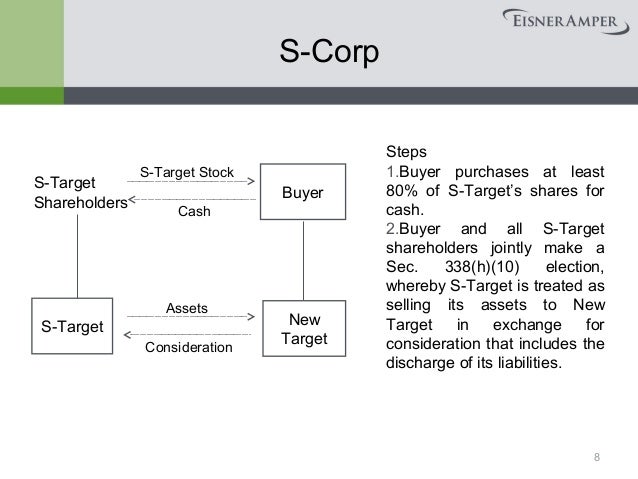

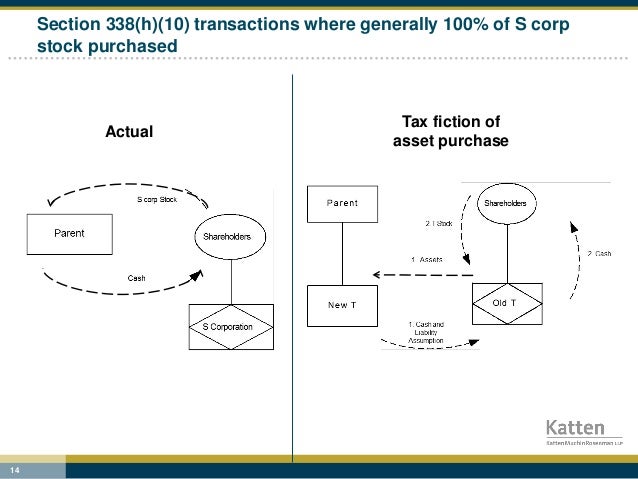

Section 338 h 10 election s corporation. A selling s corporation shareholder may also be negatively impacted when agreeing to a section 338 h 10 election by the presence of an entity level state tax that could be avoided for a straight. Limitations of 338 h 10 election. For legal purposes a 338 h 10 election remains a stock sale despite being deemed an asset sale.

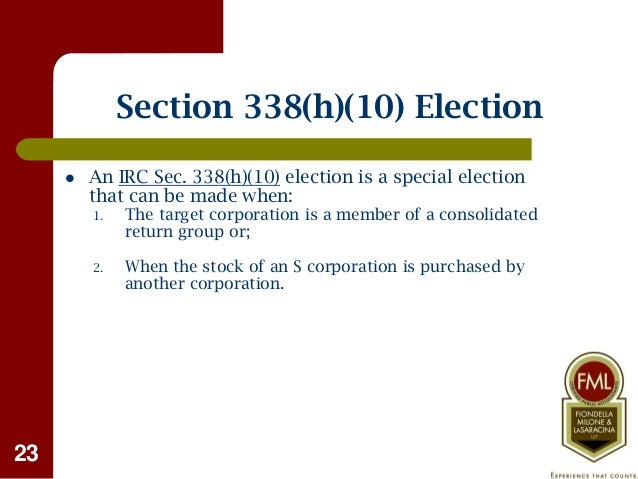

Section 338 h 10 of the internal revenue code can provide significant tax benefits to a buyer of 80 or more of a target corporation. As mentioned above s. A 338 h 10 election allows a buyer of stock of an s.

The section 338 election allows the buyer that acquires. Section 338 h 10 internal revenue code section. Section 338 h 10 of the internal revenue code can provide significant tax benefits to a buyer of 80 or more of a target corporation.

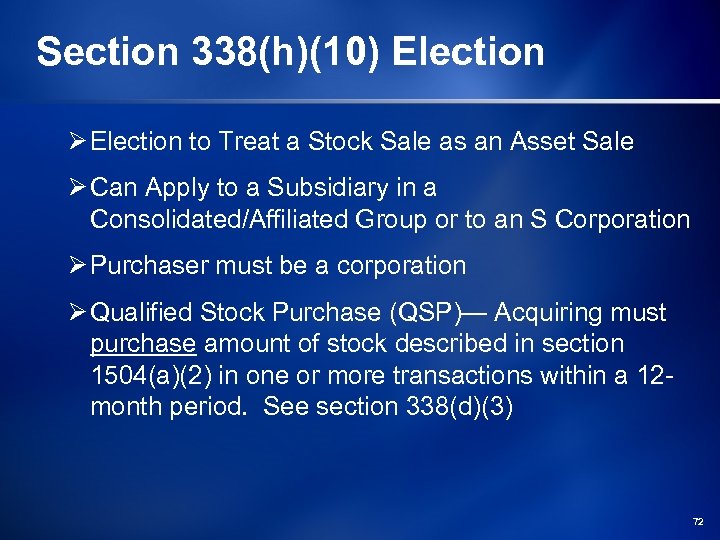

The section 338 h 10 election must be made not later than the 15th day of the 9th month beginning after the month in which the acquisition date occurs. A section 338 h 10 election is jointly made by the purchasing corporation and the common parent of the selling consolidated group or the selling affiliate or s corporation shareholder s. The s corporation equity but.

If the target is an s corporation all of the target s shareholders including shareholders who do not sell target stock in the qsp must make the election. Tax code allows corporate buyers and sellers of the stock of an s corporation to make a section 338 h 10 election so that a qualified stock purchase will be treated as a deemed asset purchase for federal income tax purposes. Corporate subsidiary of a parent company or an s corporation.

In this regard if stock of a purported s corporation is purchased in a qualified stock purchase qsp it is critical to ascertain that the target corporation has a valid s election in effect at the time of acquisition if a section 338 h 10 election is intended. Benefits and risks of a section 338 h 10 election. S corporations and section 338 h 10 if the target is an s corporation and a stock purchase is desired for non tax reasons but an asset purchase is desired for tax reasons it is common for the target s corporation s shareholders and the acquiring corporation to agree to make an election under section 338 h 10.

Https Www Ftb Ca Gov Tax Pros Procedures S Corp Handbook S Corp Chapter 16 Pdf

Tax Issues To Consider In Common Acquisition Scenarios Ppt Download

Complex Deals Class 10 M A Tax Issues And Acquisition Accounting Ppt Download

M A Tax For 2019

Https Www Revenue Pa Gov Generaltaxinformation Taxlawpoliciesbulletinsnotices Letterrulings Crp Documents Crp 14 001 Pdf

Valuation Plays Key Role In Section 338 Elections Valuation Research

Tei 56th Midyear Conference Federal Tax Seminar Ppt Download

Https Www Hcvt Com Media Publication 49 Structuring The Acquisition Of An S Corp Torosyan Bowman 2016 Pdf

Tax Issues In Private Equity Venture Capital

Https Www Thompsonhine Com Uploads 1136 Doc Domestic Taxable Mergers And Acquisitions Pdf

Harvard Law School December 3 Ppt Download

Https Www Ftb Ca Gov Tax Pros Procedures S Corp Handbook S Corp Chapter 15 Pdf

Pdf Section 338 Transactions Why Adsp And Agub Can Differ