Section 1250 Property Sale

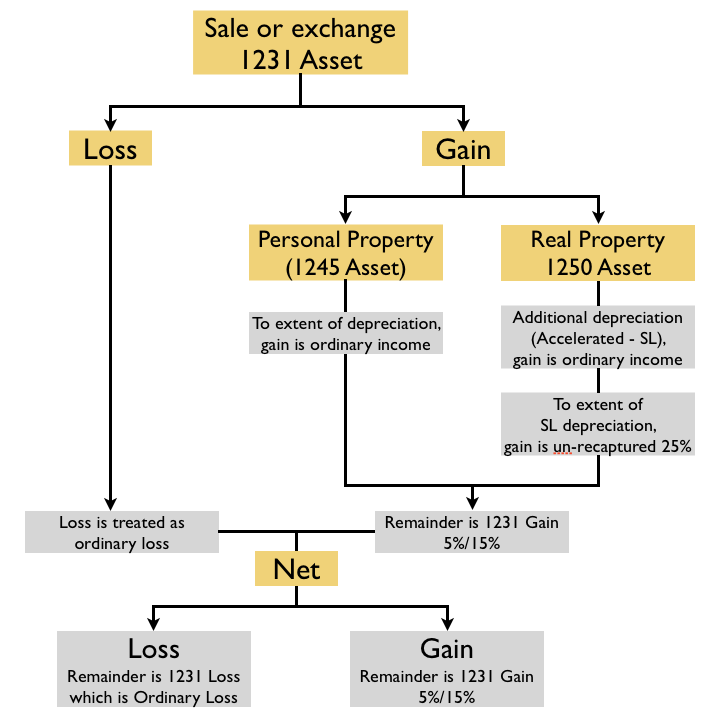

Flowchart Of Sale Or Exchange Of Property Section 1231 1245 And 1250 Assets Reg Notes Cpa Exam Club

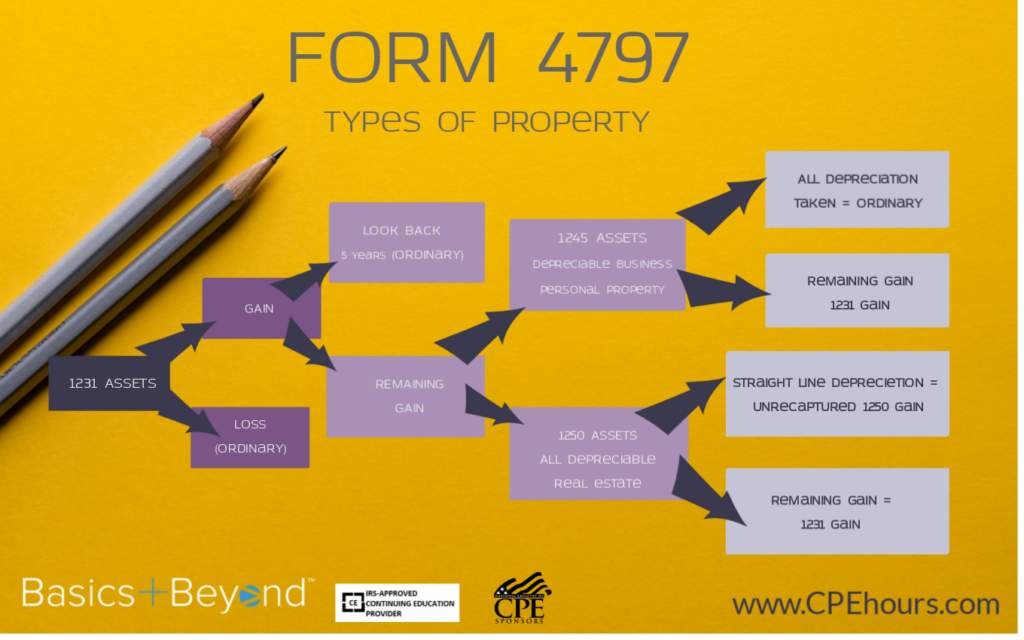

Sale Of Business Assets What You Need To Know About Form 4797 Basics Beyond

Https Www Calt Iastate Edu System Files Premium Video Files Powerpoint 20 20sale 20of 20business 20assets Pdf

Session 7 Sales Of Business Assets Ppt Video Online Download

Personal Financial Planning Ppt Video Online Download

Section 1231 And Depreciation Recapture Use This I Chegg Com

Susan has a gain of 52 885 her adjusted basis is 100 000 2885 97 115.

Section 1250 property sale. Section 1250 property depreciable real property including leaseholds if they are subject to. The additional amount treated as ordinary income is 20 of the excess of the amount that would have been ordinary income if the property were section 1245 property over the amount treated as. But 2885 is an unrecaptured section 1250 gain.

This type of property includes tangible personal property such as furniture and equipment that is subject to depreciation or intangible personal property such as a patent or license that is subject to amortization. If you are a foreign person or firm and you sell or otherwise dispose of a u s. The section 1250 recapture provisions only apply to gains not losses.

Example of unrecaptured section 1250 gains. If susan is in the 28 tax bracket her tax rate for the 2885 gain will be 721 25 25 of 2885. None of the gain is subject to section 1250 recapture because the property was placed in service after 1981.

Real property interests by foreign persons. Learn about 1231 1245 1250 property and its treatment for gains and losses. Corporations other than s corporations must recognize an additional amount as ordinary income on the sale or other disposition of section 1250 property.

A section 1231 gain is a capital gain realized from the sale of either a section 1245 property or a section 1250 property. Section 1250 of the united states internal revenue code is a rule establishing that the irs will tax a gain from the sale of depreciated real property as ordinary income if the accumulated. Jack an individual sells nonresidential real property on aug.

Capital gains and losses from both categories are added to determine the. The sale of section 1250 property at a loss produces a section 1231 loss and is deducted as ordinary loss which can reduce ordinary income. As i m sure you can see it is not as simple as just selling a business asset.

:max_bytes(150000):strip_icc()/GettyImages-1174783581-020e7504020947dc979f864f2ebee096.jpg)

Section 1250 Definition

1231 1245 And 1250 Property Used In A Trade Or Business

Recaptured And Unrecaptured Real Estate Rental Section 1250 Gain Taxcpe

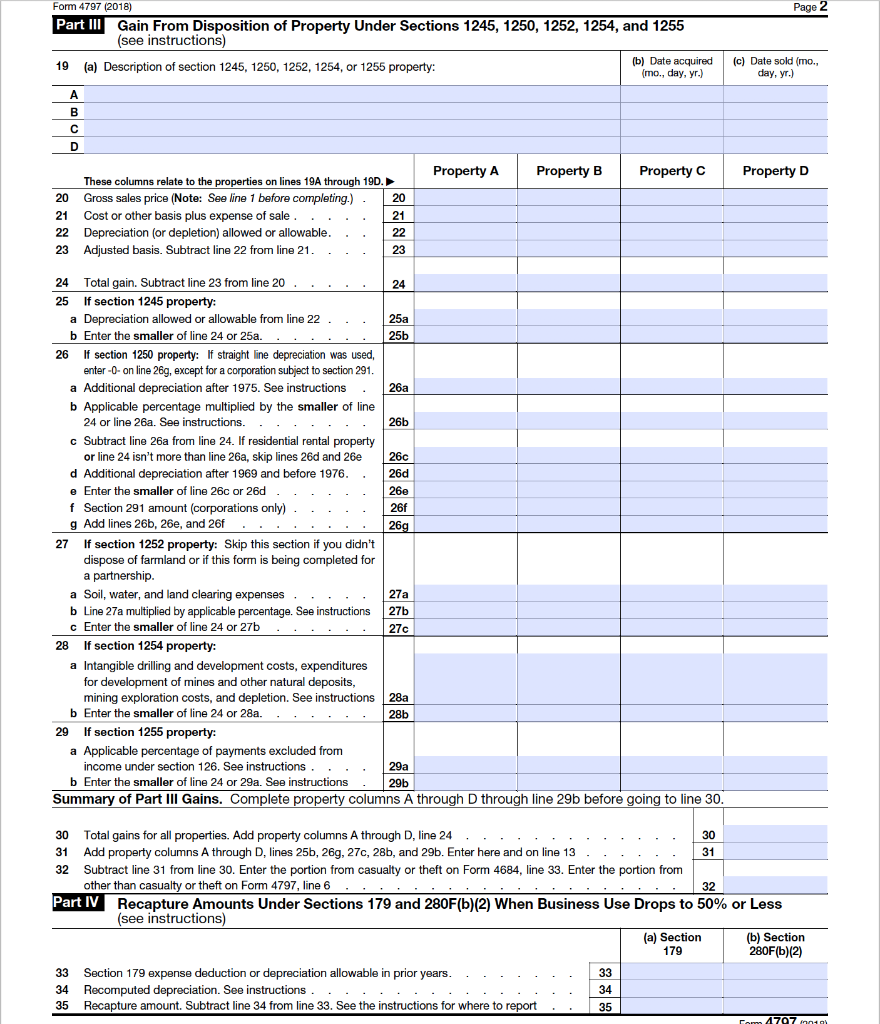

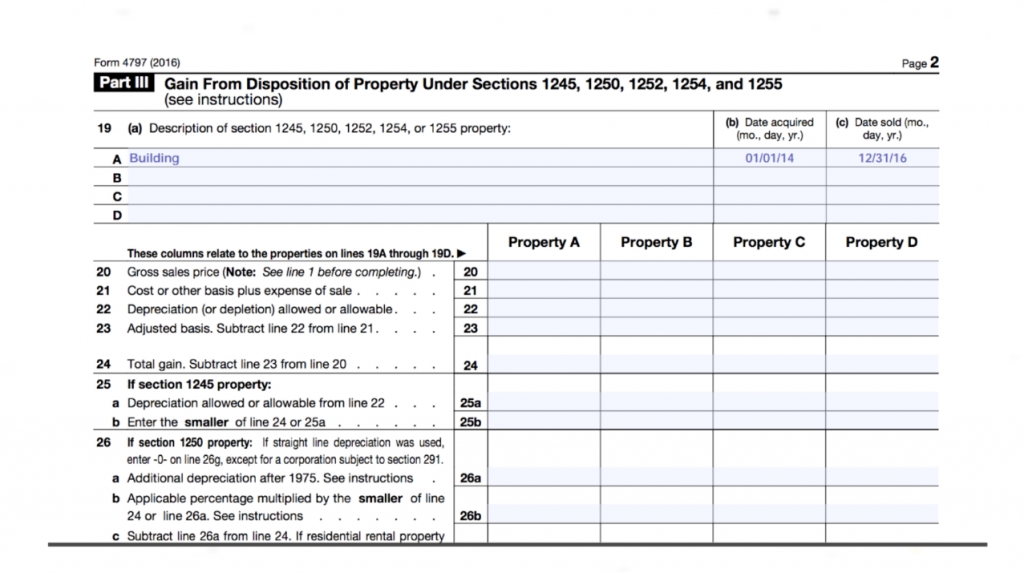

Https Farmoffice Osu Edu Sites Aglaw Files Site Library Taxpdf Ch 203 20form 204797 281 29 Pdf

How To Report The Sale Of A U S Rental Property Madan Ca

Form 4797 Sales Of Business Property

Publication 908 02 2020 Bankruptcy Tax Guide Internal Revenue Service

:max_bytes(150000):strip_icc()/architecture-building-urban-facade-property-professional-1364228-pxhere.com-cfab579cc3b64694913efdb2ea4d85c0.jpg)

Unrecaptured Section 1250 Gain Definition

Partnership Taxation What You Should Know About Section 754 Elections

Solved Sale Of Rental Property

Http Media Straffordpub Com Products Tax Issues In Sale Of Partnership And Llc Interests Structuring The Purchase Agreement 2018 07 19 Presentation Pdf

How To Sell Rental Property Without Paying Taxes

What Is 1245 Property And How Is It Taxed Millionacres