Irs Code Section 754

Https Checkpointlearning Thomsonreuters Com Liveevent Download Location Prod Ecom H0191 Westlan Com Cpl Prod Marketing Webinarattachments 1369 12 29 16 20w238t Pdf Filename 12 29 16 20w238t Pdf

Section 754 Elections Theory Practice Youtube

Section 754 And Basis Adjustments Pdf Free Download

Https Www Irs Gov Pub Irs Wd 201717038 Pdf

Important Tax Considerations When Living Abroad In 2020 Tax Preparation Services Living Abroad Tax Preparation

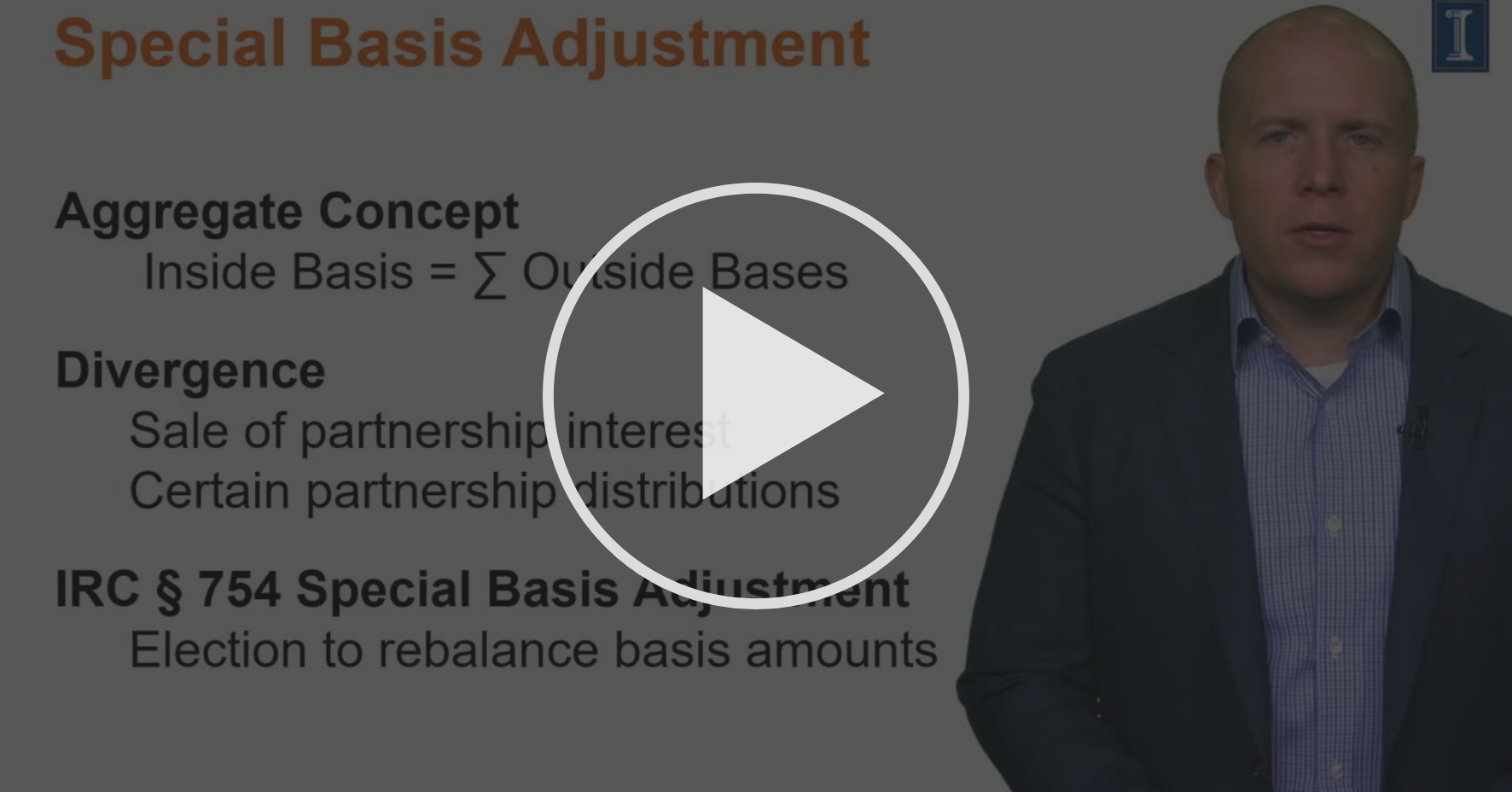

Partnership Basis Adjustments

This election allows the new partner to receive the benefits of depreciation or amortization that he or she may not have received if the election was not made.

Irs code section 754. Manner of electing optional adjustment to basis of partnership property. If a partnership files an election in accordance with regulations prescribed by the secretary the basis of partnership property shall be adjusted in the case of a distribution of property in the manner provided in section 734 and in the case of a transfer of a partnership interest in the manner provided in section 743. 743 b 1.

Section 754 allows a partnership to make an election to step up the basis of the assets within a partnership when one of two events occurs. The purpose of a section 754 election is to reconcile a new partner s outside and inside basis in the partnership. Under section 754 a partnership may elect to adjust the basis of partnership property when property is distributed or when a partnership interest is transferred.

Section 754 of the us internal revenue code provides a set of rules that govern the tax allotted for a partner. You can verify that the adjustment does not need to be entered by reviewing the supplemental information to see if the depreciation adjustment is reducing the net income. In the case of a transfer of an interest in a partnership by sale or exchange or upon the death of a partner a partnership with respect to which the election provided in section 754 is in effect or which has a substantial built in loss immediately after such transfer shall i r c.

Distribution of partnership property or transfer of an interest by a partner. A section 754 election can be a favorable tax efficiency tool that is unique to partnerships as compared to corporations. A section 754 depreciation adjustment reported on the supplemental information page of a k 1 does not usually need to be reported anywhere on the individual tax return.

754 could substantially benefit the owners of entities treated as partnerships for tax purposes i e general partnerships limited partnerships limited liability companies limited liability partnerships and other multimember entities for which a check the box election was made to treat the entity as a partnership for tax purposes or for which the default classification in the absence of an election is to treat the entity as a partnership because it allows a. Eiseman a principal in cummings lockwood s private clients and corporate and finance group published an article entitled a review of code section 754 and its tax consequences which appeared in bloomberg bna tax management real estate journal vol. Section 754 requires each partner to determine their adjusted basis in order to determine the exact tax liability of the partner.

Bloomberg bna tax management real estate journal. Every general partner of a partnership should be aware of these rules and their implications. To read a pdf of the article see below.

Partnership Taxation What You Should Know About Section 754 Elections

Https Www Enterprisecommunity Org Sites Default Files Media Library Financing And Development Asset Management 2019 Tax Return Prep Guide Pdf

The Importance Of Tax Preparation Services Tax Preparation Services Tax Preparation Business Tax

Https Www Oataxpro Com Assets Files Presentations Be 21 Partnership Termination On Sale Etc Pdf

For More Information About The Ncic Missing Persons Deport And In Depth Detailed Description Please Click On This Link H Missing Persons Word Find Informative

Partnerships And Llc S The Basics Of Making A 754 Election Marcum Llp Accountants And Advisors

How Much Do Accountants Make

Understand The Tax Implications Of Practice Buy Ins Buy Outs

Could The 754 Election Benefit Your Partnership Ds B

Section 754 Inside Basis Vs Outside Basis Taxation Of Partnerships

Making A Valid Sec 754 Election Following A Transfer Of A Partnership Interest

Ppt Partnership Termination And Transfer Of A Partner S Interest Amanda Wilson February 21 2013 Powerpoint Presentation Id 3321120

We Can Help You Sell Your Home Quickly In 2020 Investment Advice How Are You Feeling Community Involvement