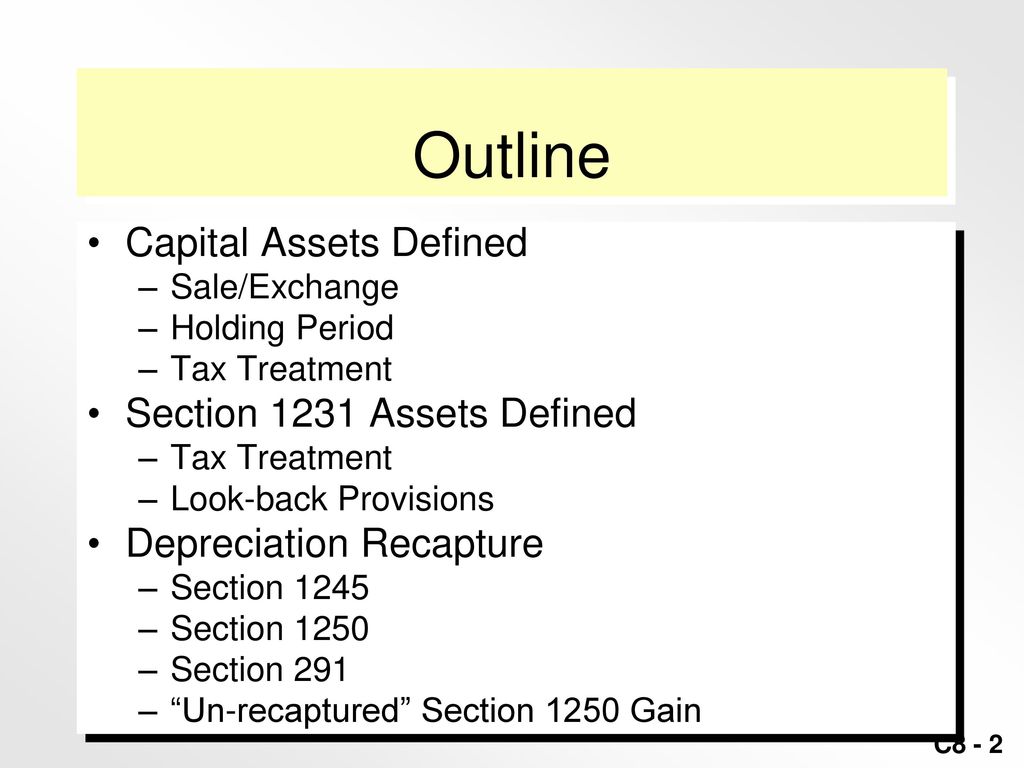

Section 1250 Property Recapture

Understanding Depreciation Recapture Taxes On Rental Property Rental Property Being A Landlord Military Housing

The Best Charts Of Inflation Adjusted Historical Real Estate Prices Available On The Internet Real Estate Prices House Prices Chart

Sales Of Business Assets Taxconnections

Lazy Portfolios Bogleheads Lazy Portfolios Early Retirement

Solved Capital Gains And Losses Section 1245 Recapture R Chegg Com

Http Media Straffordpub Com Products Calculating Depreciation Recapture Under Irc 1245 And 1250 Minimizing Tax Through Transaction Planning 2017 08 15 Presentation Pdf

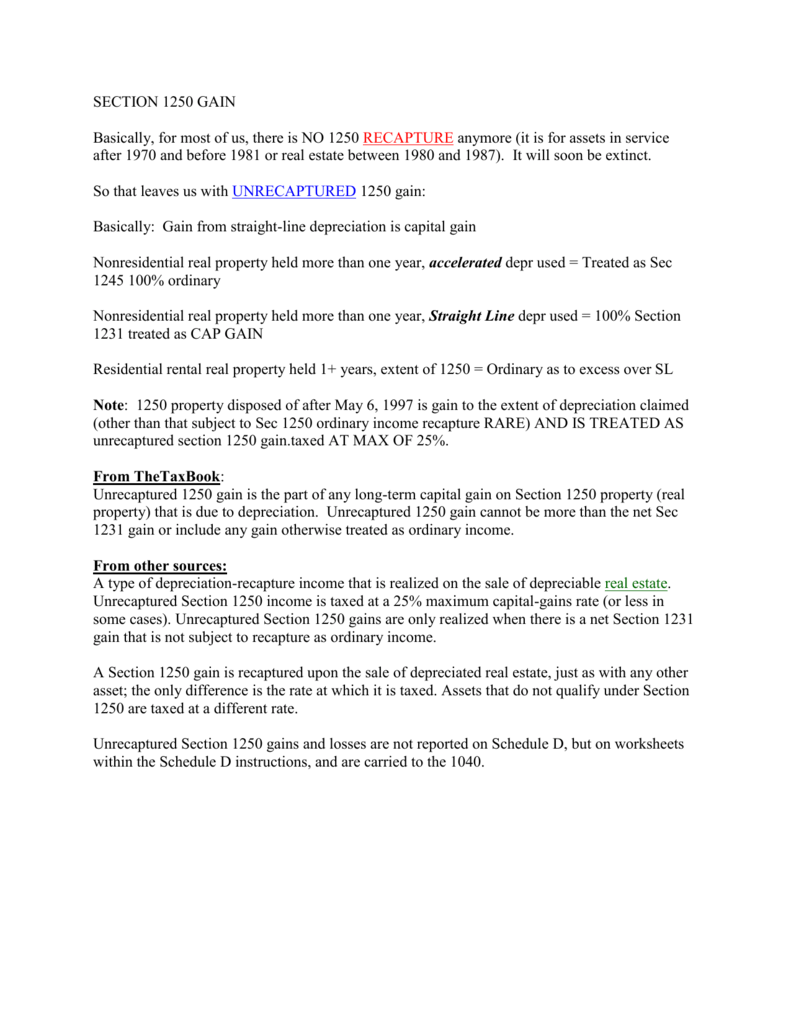

Example of unrecaptured section 1250 gains.

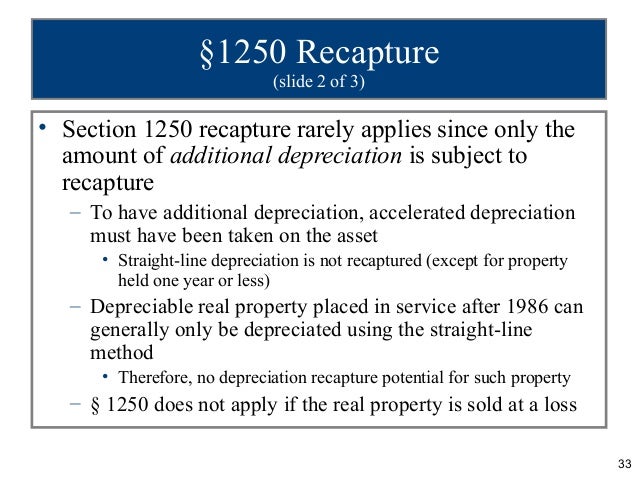

Section 1250 property recapture. Capital gains and losses from both categories are added to determine the. But 2885 is an unrecaptured section 1250 gain. Depreciation taken by other taxpayers or on other property.

Section 1250 property defined. Deck shingles vapor barrier skylights trusses girders and gutters. Retired or demolished property.

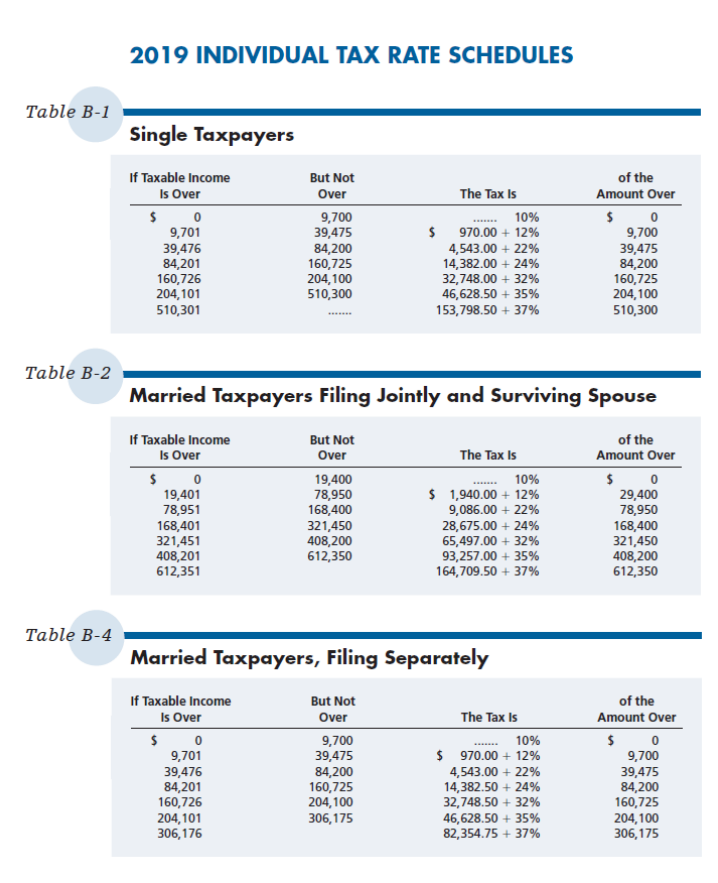

If a property was initially purchased for 150 000 and the owner claims depreciation of 30 000 the adjusted cost basis for the property is. If susan is in the 28 tax bracket her tax rate for the 2885 gain will be 721 25 25 of 2885. Recapture rules for section 1250 real property.

But the amount of depreciation claimed on sec 1250 property that is not recaptured as ordinary income under the sec1250 recapture rules is unrecaptured section 1250 gain and is subject to a special capital gain tax rate of 25. In the case of section 1250 property with respect to which a mortgage is insured under section 221 d 3 or 236 of the national housing act or housing financed or assisted by direct loan or tax abatement under similar provisions of state or local laws and with respect to which the owner is subject to the restrictions described in section 1039 b 1 b as in effect on the day before the date. Of the cost of construction of the building and.

15 for 200 000 realizing a gain of 50 000. A section 1231 gain is a capital gain realized from the sale of either a section 1245 property or a section 1250 property. Depreciation allowed or allowable.

Under section 1250 the recapture of gain as ordinary income is restricted to the actual gain recorded on a real property sale. Section 1231 property is a tax term relating to a depreciable. Property held by lessee.

Section 1245 And 1250 Recapture Provisions Youtube

Https Farmoffice Osu Edu Sites Aglaw Files Site Library Taxpdf Ch 203 20form 204797 281 29 Pdf

Lazy Portfolios Bogleheads Lazy Portfolios Early Retirement

Https Resources Taxschool Illinois Edu Taxbookarchive 2013 C1 20form 204797 Pdf

Sample Mean Reversion Algorithm Algorithm Educational Tools Investing

Https Farmoffice Osu Edu Sites Aglaw Files Site Library Taxpdf 2 202017 20agricultural 20tax 20issues Part 20ii Section 20b Transfer 20of 20farm 20assets September 2024 202017 Pdf

Vol 01 Chapter 17 2015

Section 1250 Depreciation Recapture Corporate Income Tax Cpa Reg Ch 14 P 6 Youtube

Recaptured And Unrecaptured Real Estate Rental Section 1250 Gain Taxcpe

Section 1250 Gain Basically For Most Of Us There Is No 1250

Dor Adjusting The Wisconsin Basis Of Depreciated Or Amortized Assets

Http Investor Apachecorp Com Static Files 92f9e587 Ae4a 4b89 9fcc 33a78f9a7d13