Section 280g Change In Control

Golden Parachute Payments Under Section 280g Valuation Research

Noncompete Agreements For Section 280g Compliance For Banks Mercer Capital

What Is A 280g Parachute Payment Understand The Risks Involved

Change In Corporate Ownership Or Control May Result In Golden Parachute Payments The Cpa Journal

Mercer Capital S Noncompete Agreements For Section 280g Compliance

Section 280g Golden Parachutes Meridian Compensation Partners Llc Executive Compensation Consulting

Golden parachute payments.

Section 280g change in control. 1018 d 6 substituted section 1361 b but without regard to paragraph 1 c. Internal revenue code section 280g also known as the golden parachute payment rule is the federal tax provision that covers these payments. 280g impacts both the corporate entity and its executives shareholders and other highly compensated individuals associated with the corporation and imposes harsh tax consequences if not properly addressed.

Congress added section 280g to the internal revenue code in response to critics of the arrangement to discourage companies from paying golden parachutes. A golden parachute is a payment or benefit made by a corporation to certain executives managers or others called disqualified individuals by the irs when there is a change in control of that corporation. 280g b 2 a ii.

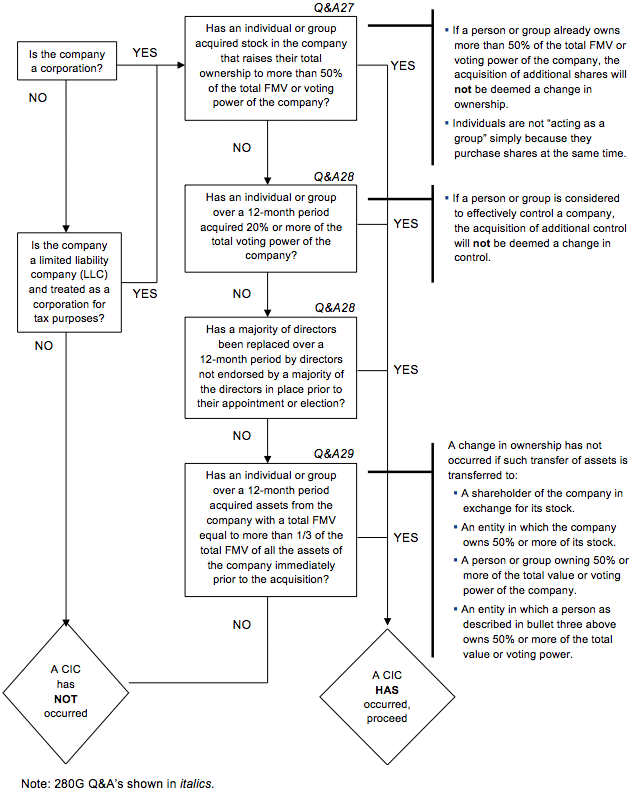

However the payment still could be a parachute payment under q a 37 of this section if the contract violated a generally enforced securities law or regulation. Section 1 280g 1 q a 27 a provides that a change in the ownership of a corporation occurs on the date that any one person or more than one person. If this presumption is not rebutted the payment will be treated as contingent on the change in ownership or control.

If no change in ownership or control had occurred the payment would not be treated as contingent on a change in ownership or control. Base period means the period consisting of the most recent 5 taxable years ending before the date on which the change in ownership or control described in. If the present value of change in control payments to a disqualified individual is outside the safe harbor that is the present value equals or exceeds three times the base amount then the excess parachute payments are calculated on amounts paid in excess of the disqualified individual s base amount rather than the amount in excess of the safe harbor sec.

Section 280g denies a corporate tax deduction for and section 4999 imposes a non deductible 20 excise tax on the recipients of payments exceeding a statutory thresh old that are made to senior executives in connection with a change in control and as a result can have a signi cant adverse impact on change in control payments penalizing both the employer and the executive. 280g change in control means a change in the ownership or effective control of the company or in the ownership of a substantial portion of the assets of the company as determined in accordance with section 280g b 2 of the code and the regulations issued thereunder. Golden parachute payments are payments of compensation made to individuals whose companies experience a change in control.

Section 1 280g 1 q as 27 and 29 provides guidance concerning whether a corporation is considered to have undergone a change in ownership or control in a merger.

Pin On Vegan

Pin On Diet Workout

Pin By Denada Maku On Pages How To Stop Procrastinating Procrastination Overcoming Procrastination

Pasini Law Golden Parachutes And Section 280g An Overview And Practice Tips

Printed On Top Quality Heavyweight 280g Satin Finish Paper Frame Is Not Included Sizes A4 21x29 7cm 8 27 X 11 Cartaz Publicitario Cartaz Publicitarios

The Happiest Women Like The Happiest Nations Have No History Happy Nation Happy Quotes Make Me Smile Quotes

Http Media Straffordpub Com Products Executive Employment Agreements And Change In Control Arrangements 2015 10 13 Presentation Pdf

Pin On Health And Fitness

Neila Rey S Vegetarian Diet Neilareyideagenial Vegetarian Bodybuilding Vegetarian Diet Bodybuilding Recipes

Face Mask Mockup Original In 2020 Face Mask Mask Face

Https Dpntax5jbd3l Cloudfront Net Images Content 1 6 V2 168586 Parachute Payments A Few Things You Should Know February 201 Pdf

In Our Shangri La Terms For Code Section 280g Golden Parachute Taxes In Employment Agreements Holland Hart The Benefits Dial Jdsupra

Herbalife Beverage Mix Canister Wild Berry 280g Canister By Herbalife Http Www Amazon Com Dp B005j5zp88 Ref Cm Sw R Pi Dp Fp Herbalife Wild Berry Beverages