Section 125 Irc

Section 125 Plan Administration American Fidelity

Section 125 Plan Lively

Irs Section 125core Documents

Ssa Poms Si 00820 102 Cafeteria Benefit Plans 07 23 2012

Do You Need A Section 125 Plan Document Get One Today Core Documents

Is Your Section 125 Plan Compliant American Fidelity

Section 125 cafeteria plans health flexible spending arrangements not subject to 2 500 limit on salary reduction contributions for plan years beginning before 2013 and comments requested on potential modification of use or lose rule.

Section 125 irc. A section 125 plan is part of the irs code that enables and allows employees to take taxable benefits such as a cash salary and convert them into nontaxable benefits. 125 b exception for highly compensated participants. 100 203 as added by pub.

These benefits may be. 125 a general rule except as provided in subsection b no amount shall be included in the gross income of a participant in a cafeteria plan solely because under the plan the participant may choose among the benefits of the plan. Irs provides tax relief through increased flexibility for taxpayers in section 125 cafeteria plans internal revenue service skip to main content.

For provision that for purposes of section 125 of the internal revenue code of 1986 a plan shall not be treated as failing to be a cafeteria plan solely because under the plan a participant elected before january 1 1988 to receive reimbursement under the plan for dependent care assistance for periods after december 31 1987 and such assistance included reimbursement for expenses at a camp where the dependent stays overnight see section 10101 b 2 of pub. Section 125 of the internal revenue code refers to cafeteria plan benefits.

Irs Increases Flexibility For Section 125 Cafeteria Plan Squar Milner

5 Things Districts Need To Know About Section 125 Cafeteria Plans

Http Doa Alaska Gov Drb Pdf Employer Cafeteriaplans Slidesnoteshandout Pdf

New Irs Guidance Provides Employers With Section 125 Plan Flexibility During 2020

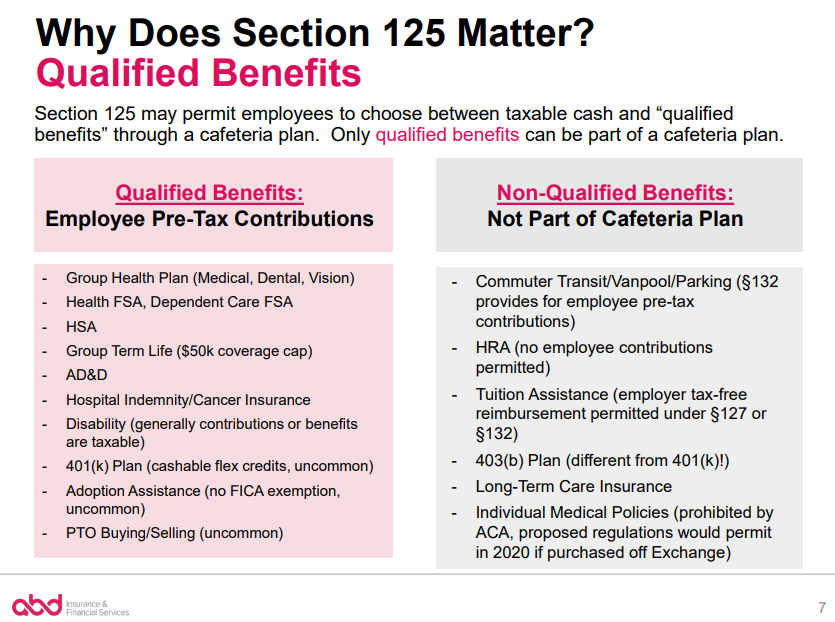

How Aca Affects Flex Credits Abd Insurance Financial Services

Http Twinriversarea Org Wp Content Uploads 2016 09 Section 125 Pdf

Cafeteria Plan Section 125 Features Costs Providers

Cash In Lieu Option Must Follow Section 125 Irs Rules Core Documents

Linear Handrail Bracket Handrail Brackets Handrail Stainless Steel Handrail

Cafeteria Plan Options For 2020 Section 125 Pop Hsa Fsa Dcap Core Documents

Standard Deck Railing Height Decks Residential Building Permits Stair Railing Requirements Codes Deck Railings Deck Stairs Deck Railing Height

Celebrating 40 Years Of Section 125 Cafeteria Plans Core Documents

Box 12w Hsa Employer Contributions Asap Help Center