Irs Section 1250 Property

Https Www Irs Gov Pub Irs Utl 03 Alternative 20minimum 20tax 20pains Pdf

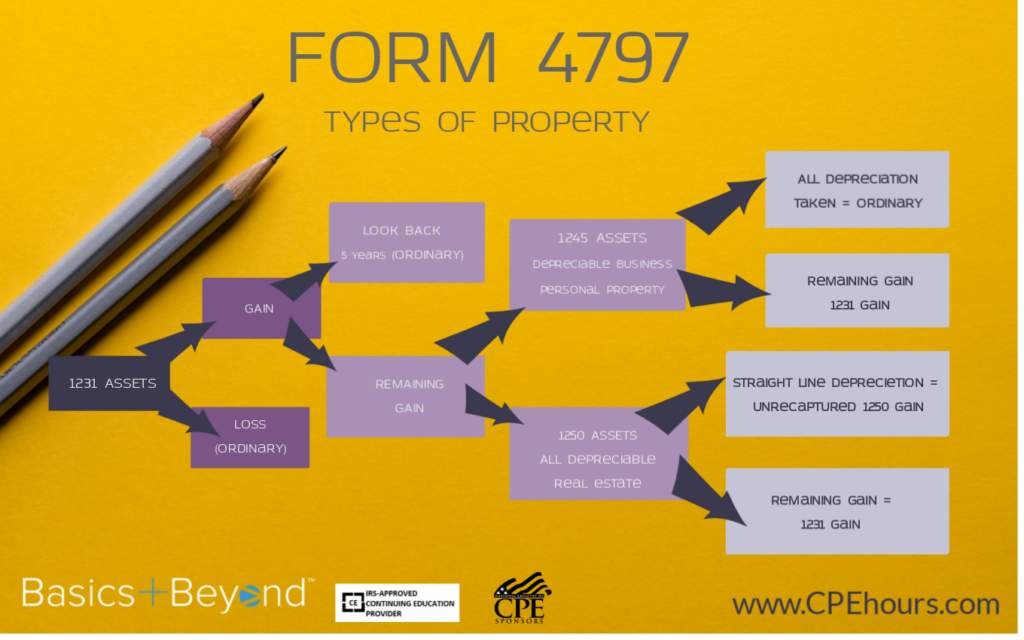

Sale Of Business Assets What You Need To Know About Form 4797 Basics Beyond

Sales Of Business Assets Taxconnections

Depreciation Recapture On Rental Property And Calculator Avoid The Painful Irs With A 1031 Exchange Inside The 1031 Exchange

Https Farmoffice Osu Edu Sites Aglaw Files Site Library Taxpdf Ch 203 20form 204797 281 29 Pdf

The Best Charts Of Inflation Adjusted Historical Real Estate Prices Available On The Internet Real Estate Prices House Prices Chart

Figuring straight line depreciation.

Irs section 1250 property. Retired or demolished property. Section 1250 of the united states internal revenue code is a rule establishing that the irs will tax a gain from the sale of depreciated real property as ordinary income if the accumulated. Section 1250 property includes all real property subject to an allowance for depreciation.

Publication 544 sales and other dispositions of assets depreciation recapture section 1250 property. Learn about 1231 1245 1250 property and its treatment for gains and losses. Section 1250 property defined.

Section 1250 property depreciable real property including leaseholds if they are subject to depreciation. 1231 1245 and 1250. Property held by lessee.

Property used in a trade or business the internal revenue code includes multiple classifications for property. Depreciation allowed or allowable. Depreciation taken by other taxpayers or on other property.

Of the cost of construction of the building and depreciated over the life of the building. The most common examples of 1250 property are buildings and. Unrecaptured section 1250 gain is the portion of a capital gain related to the amount a property has already been depreciated.

Section 1250 property the following is a list of the nine property classifications under gds and examples of the types of property included in each class. Deck shingles vapor barrier skylights trusses girders and gutters. Any portion of the sale price of real estate that was previously.

Http Media Straffordpub Com Products Calculating Depreciation Recapture Under Irc 1245 And 1250 Minimizing Tax Through Transaction Planning 2017 08 15 Presentation Pdf

:max_bytes(150000):strip_icc()/GettyImages-1174783581-020e7504020947dc979f864f2ebee096.jpg)

Section 1250 Definition

1231 1245 And 1250 Property Used In A Trade Or Business

Https Www Calt Iastate Edu System Files Premium Video Files Powerpoint 20 20sale 20of 20business 20assets Pdf

3 22 15 Foreign Partnership Withholding Internal Revenue Service

Fundraising Sponsorship Proposal Template Free Sponsorship Proposal Sponsorship Package Proposal Templates

Http Investor Apachecorp Com Static Files 92f9e587 Ae4a 4b89 9fcc 33a78f9a7d13

Lazy Portfolios Bogleheads Lazy Portfolios Early Retirement

Recaptured And Unrecaptured Real Estate Rental Section 1250 Gain Taxcpe

The Ladders Of Wealth Creation A Step By Step Roadmap To Building Wealth In 2020 Wealth Creation Wealth Building Wealth

Instructions For Form 1040 Nr 2019 Internal Revenue Service

Https Resources Taxschool Illinois Edu Taxbookarchive 2017 B1 Installment Sales Pdf

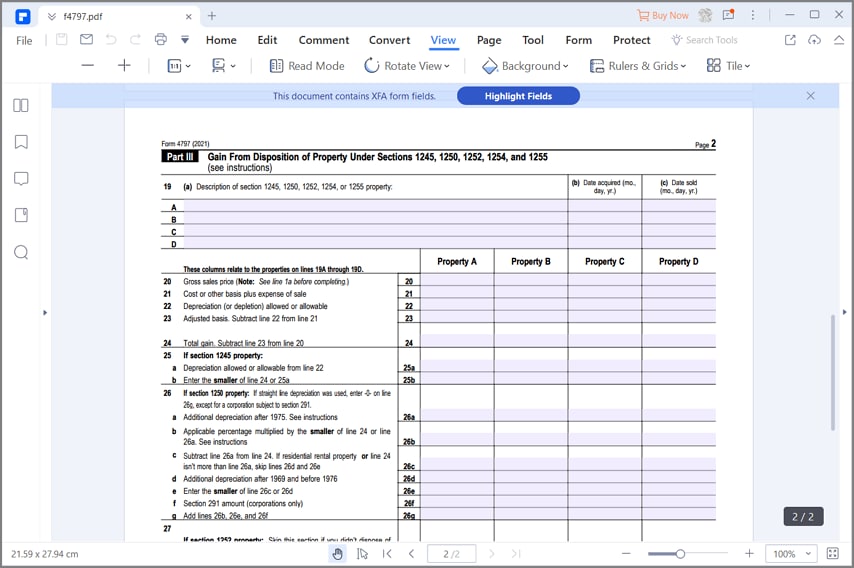

Irs Form 4797 Guide For How To Fill In Irs Form 4797