Irs Section 125 Rules

New Irs Guidance Provides Employers With Section 125 Plan Flexibility During 2020

Section 125 Covid 19 Relief Irs On 2020 Mid Year Elections Fsa Claims Core Documents

Cash In Lieu Option Must Follow Section 125 Irs Rules Core Documents

Irs Section 125core Documents

Http Doa Alaska Gov Drb Pdf Employer Cafeteriaplans Slidesnoteshandout Pdf

How Aca Affects Flex Credits Abd Insurance Financial Services

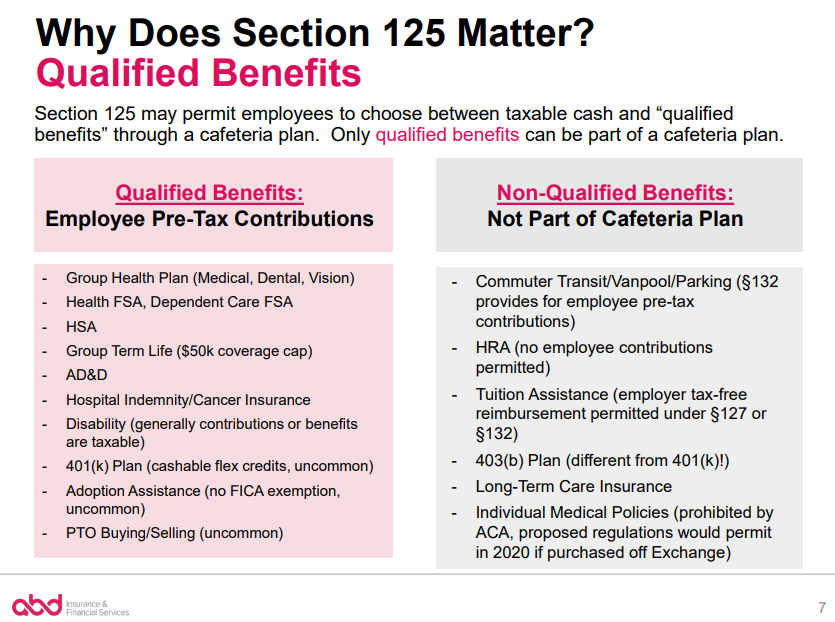

Section 125 f defines a qualified benefit as any benefit which with the application of 125 a is not includable in the gross income of the employee by reason of an express provision of chapter i of the internal revenue code other than 106 b 117 127 or l32.

Irs section 125 rules. Except as provided in subsection b no amount shall be included in the gross income of a participant in a irs section 125 cafeteria plan solely because under the plan the participant may choose among the benefits of the plan. If taken as a. A general rule except as provided in subsection b no amount shall be included in the gross income of a participant in a cafeteria plan solely because under the plan the participant may choose among the benefits of the plan.

A cafeteria plan may permit an employee to revoke an election during a period of coverage and to make a new election only as provided in paragraphs b through g of this section. B exception for highly compensated participants. A cafeteria plan also known as a section 125 plan is a written plan that offers employees a choice between receiving their compensation in cash or as part of an employee benefit.

See notice 2013 71 2013 47 irb. Irs section 125 code. These changes extend the claims period for health flexible spending arrangements fsas and dependent care assistance programs and allow taxpayers to make mid year changes.

B exception for highly compensated participants and key employees. Section 125 i provides that a health fsa is not treated as a qualified benefit unless the cafeteria plan provides that an employee may not elect for any taxable year to have salary reduction contributions in excess of 2 500 made to such arrangement. Section 125 does not require a cafeteria plan to permit any of these changes.

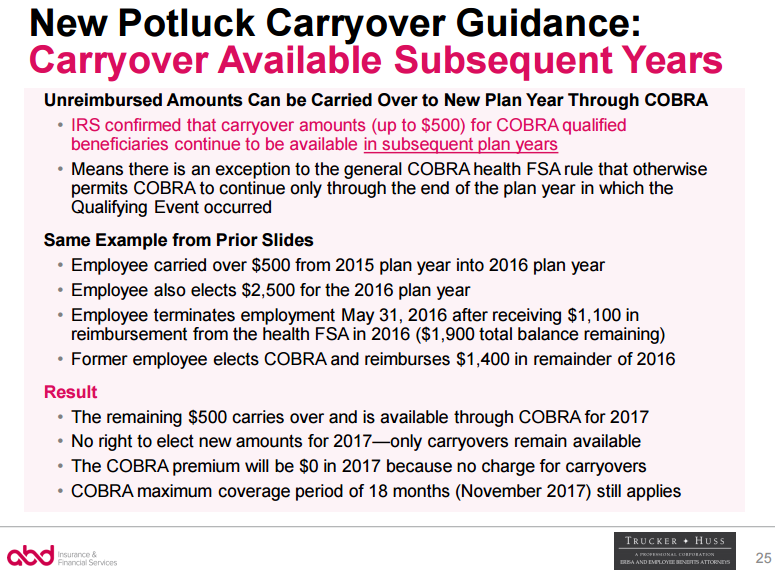

Ir 2020 95 may 12 2020 washington the internal revenue service today released guidance to allow temporary changes to section 125 cafeteria plans. Under the carryover rule a 125 cafeteria plan may permit the carryover of unused amounts remaining in a health fsa as of the end of a plan year to pay or reimburse a participant for medical care expenses incurred during the following plan year subject to the carryover limit currently 550. These benefits may be.

What Is A Section 125 Pop Premium Only Plan Gusto

Https Theabdteam Com Sites Default Files Content Presentation File Abd 20office 20hours 20 Section 20125 20cafeteria 20plans 20final Pdf

Understanding Section 125 Cafeteria Plans

Internal Revenue Bulletin 2020 22 Internal Revenue Service

Irs Issues New Rules Impacting Cafeteria Plans Mcafee Taft

Client Alert Irs Relaxes Section 125 Mid Year Change Rules Increases Health Fsa Carryovers Fraser Trebilcock Jdsupra

Health Fsa Reimbursements After Termination Of Employment Abd Insurance Financial Services

Https Www Truenetworkadvisors Com S March Compliance Webinar 125 Cafeteria Plans Pdf

What Is A Section 125 Plan And Who Needs One Onedigital

Flexible Spending Account Rule Changes Section 125

Irs Releases 2020 Tax Rate Tables Standard Deduction Amounts And More Tax Brackets Standard Deduction Payroll Taxes

Irs Provides 125 Plan And Flexible Spending Account Relief In Response To Covid 19 Frost Brown Todd Full Service Law Firm

Taxation Of Irs Section 125 And Health Insurance Finance Zacks