Section 482 Irs

013 Free Bank Statement Template Printable Download Obc Regarding Blank Bank Statement Template Download In 2020 Statement Template Bank Statement Money Template

Section 482 Methods To Determine Taxable Income In Connection With Cost Sharing Arrangement Us Internal Revenue Service Regulation Irs 2018 Edition The Law Library 9781729729540 Amazon Com Books

Sec 482 Allocation Of Income And Deductions Among Taxpayers

A Closer Look At The Repeal Of Section 958 B 4 Withum

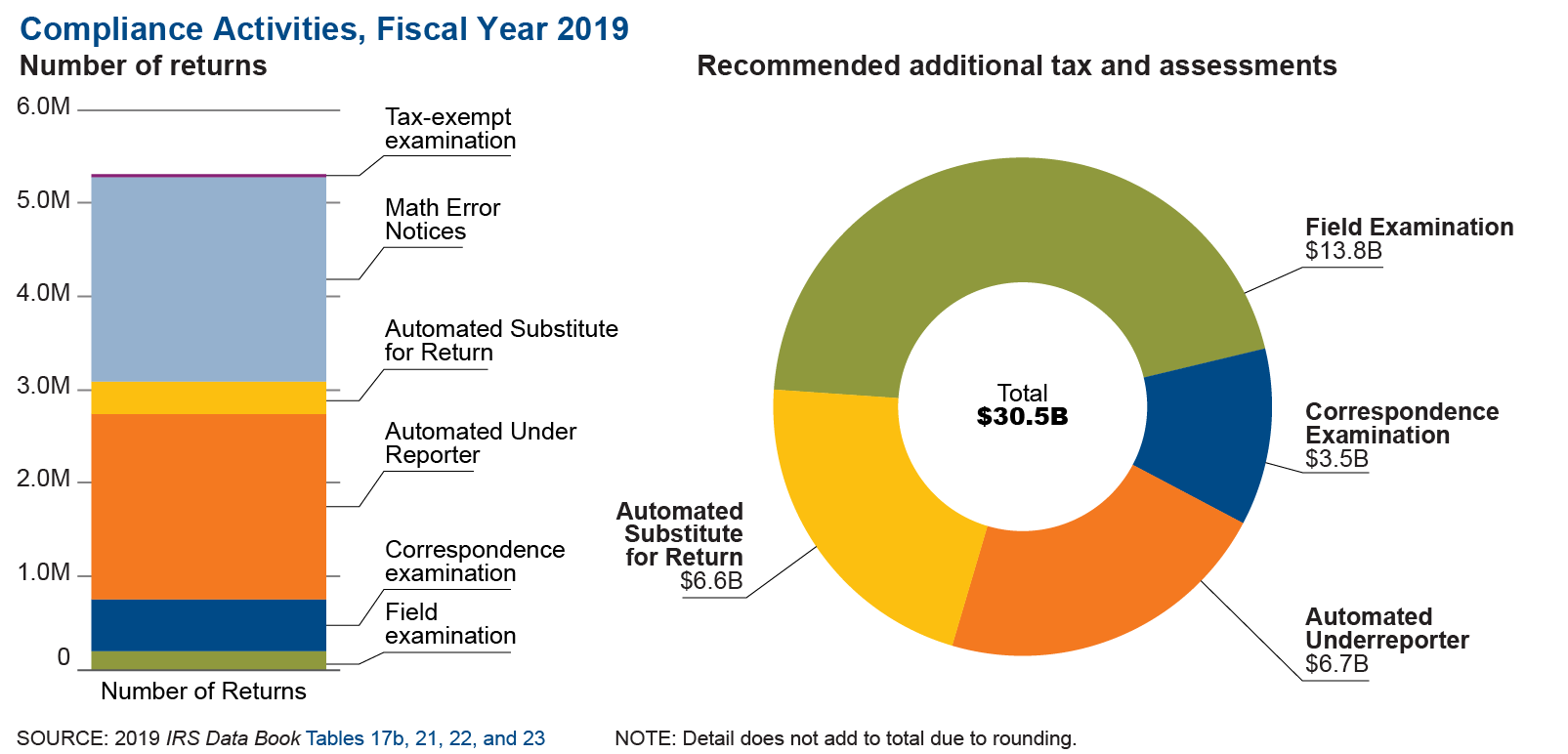

Compliance Presence Internal Revenue Service

Transfer Pricing Tax Irc Irs Taxpayers Mnc Section 482 Contemporaneous Documentation

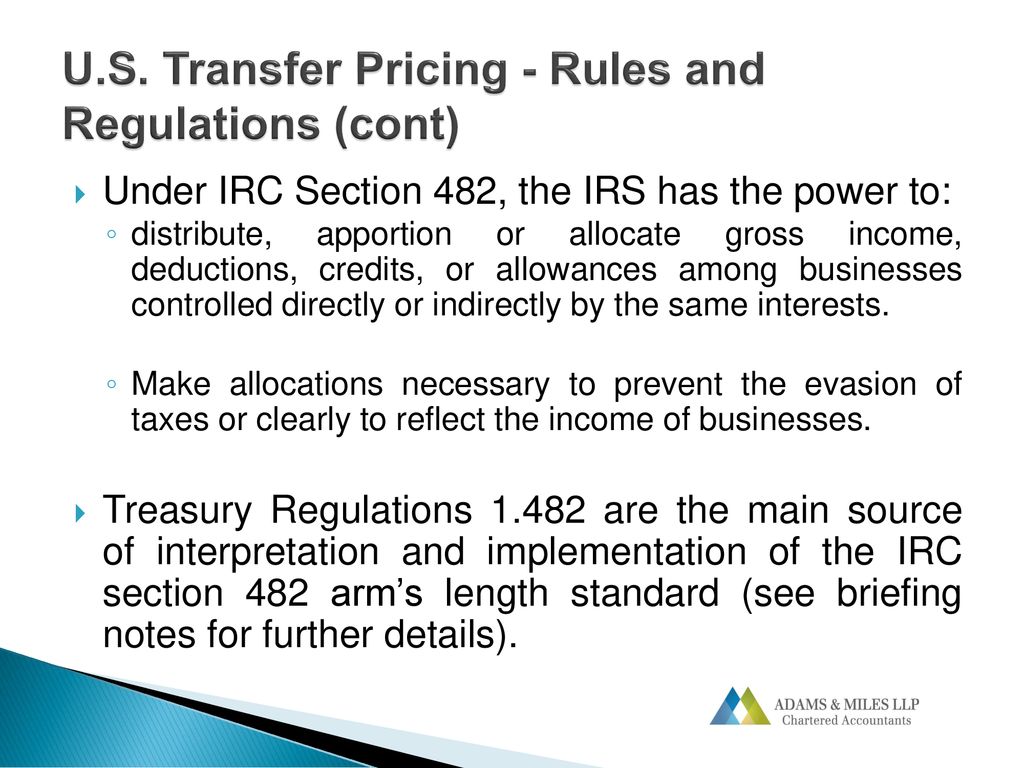

The purpose of section 482 is to place a controlled taxpayer on parity with an uncontrolled taxpayer in an attempt to achieve a proper reflection of true taxable income.

Section 482 irs. 1 1992 submit to committee on ways and means of house of representatives and committee on finance of senate a report on the study together with such recommendations as he deemed advisable. 5 1990 104 stat. 482 of the internal revenue code code the income tax regulations the regulations thereunder and relevant income tax treaties to which the united states is a party in a principled and cooperative manner on a prospective basis.

The study shall include a review of the contemporaneous documentation and penalty rules under section 6662 of the internal revenue code of 1986 a review of the regulatory and administrative guidance implementing the principles of section 482 of such code to transactions involving intangible property and services and to cost sharing arrangements and an examination of whether increased disclosure of cross border transactions should be required. The purpose of section 482 is to ensure that taxpayers clearly reflect income attributable to controlled transactions and to prevent the avoidance of taxes with respect to such transactions. Irc 482 places a controlled taxpayer on a tax parity with an uncontrolled taxpayer in determining true taxable income.

1388 458 directed secretary of the treasury or his delegate to conduct a study of the application and administration of section 482 of the internal revenue code of 1986 and not later than mar. 101 508 title xi 11316 nov. Section 482 places a controlled taxpayer on a tax parity with an uncontrolled taxpayer by determining the true taxable income of the controlled taxpayer.

Section 482 places a controlled taxpayer on a tax parity with an uncontrolled taxpayer by determining the true taxable income of the controlled taxpayer.

Internal Revenue Bulletin 2019 32 Internal Revenue Service

8 17 5 Special Computation Formats Forms And Worksheets Internal Revenue Service

Ninth Circuit Reverses Tax Court In Loss For Intel And Win For Irs Accounting Today

Customs Valuation A Concern For Unsuspecting Tax Practitioners

Https Www2 Deloitte Com Content Dam Deloitte Us Documents Tax Us Tax Inside Deloitte Global Business And States 20challenges To Taxable Income Pdf

The Future Of Dating Apps Funny Memes Funny P Funny Pictures

Dealing With The Secondary U S Tax Consequences Of Transfer Pricing Adjustments

Transfer Pricing Rules

Irs Faces Big Decisions 482 Transfer Pricing Rules

Https Www Jstor Org Stable 40707127

Http Www Irs Gov Pub Irs Irbs Irb20 04 Pdf

Insight Accounting Standard Asc 606 And Transfer Pricing The Devil Is In The Details

U S Transfer Pricing Overview Ppt Download