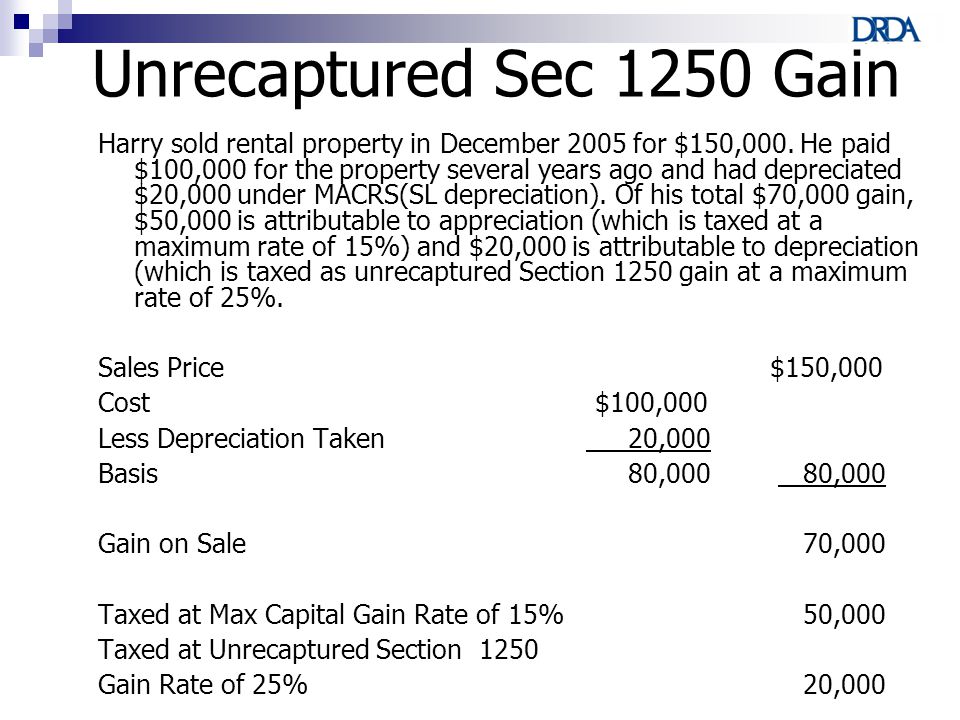

Unrecaptured Section 1250 Gain Example

1040 Us Calculating Unrecaptured Section 1250 Gain At 25 Capital Gains Tax Rate

Unrecaptured Section 1250 Gain Fill Online Printable Fillable Blank Pdffiller

Session 7 Sales Of Business Assets Ppt Video Online Download

Tax Consequences Of Buying And Selling A Business January 2006 Presented By Douglas A Dickey Cpa Ppt Download

Http Media Straffordpub Com Products Calculating Depreciation Recapture Under Irc 1245 And 1250 Minimizing Tax Through Transaction Planning 2017 08 15 Presentation Pdf

Chap 3 1b Property Disposition Cap Assets Etc Howard Godfrey Ph D Cpa Professor Of Accounting C Howard Godfrey Ppt Download

As an example if accumulated depreciation otherwise subject to unrecaptured section 1250 gain treatment is 10 000 but analysis can reduce the gain attributable to the building at the date of sale to 6 000 then the federal income tax to a high bracket taxpayer on the 4 000 reduction is reduced from 2 500 to 1 000.

Unrecaptured section 1250 gain example. 1250 recapture example purchase price 40 000 accumulated acrs depreciation 25 000 accumulated sl depreciation 18 000 sales price 32 000 17 000 32 000 15 000 gain 7 000 25 000 18 000 is 1250 recapture 10 000 is unrecaptured 1250 gain 12. Jack an individual sells nonresidential real property on aug. So in my example above the 20 000 of unrecaptured section 1250 gain would be regular tax rates usually 25 and the 50 000 would be taxed at long term capital gain rates usually 15.

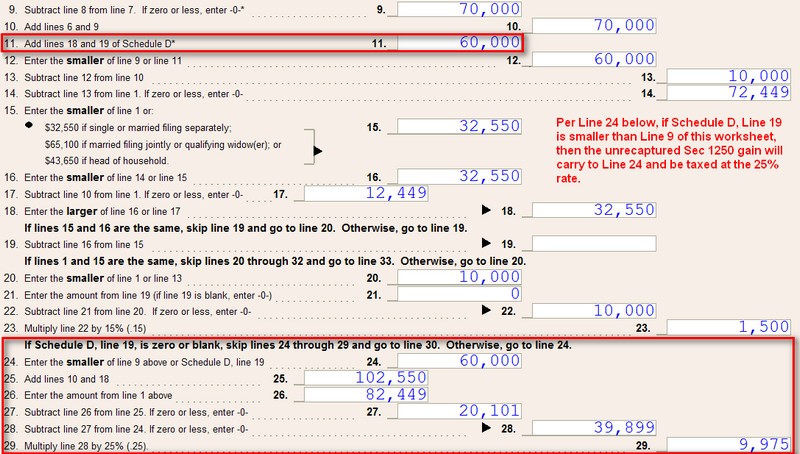

15 for 200 000 realizing a gain of 50 000. This worksheet can be found in forms view under the dwrk folder on the 28 rate capital gain and sec 1250 wrk tab. The unrecaptured gain is calculated as 70 000 depreciation allowed or allowable 79 079 additional depreciation 9 079.

The result is your total unrecaptured section 1250 gain that must be allocated to the installment payments received from the sale. The 20 000 is known as unrecaptured section 1250 gain by the irs. The unrecaptured section 1250 gain is taxed at your regular tax bracket up to a maximum of 25.

Your capital gains tax is based on your regular tax bracket while your unrecaptured section 1250 gain is a flat rate. Unrecaptured section 1250 gain only applies to depreciable real estate such as commercial real estate and residential rental properties. Follow the example in this topic to enter unrecaptured section 1250 gains.

It is only applicable to the sale of. To enter this information in the federal module. An unrecaptured section 1250 gain is an income tax provision designed to recapture the portion of a gain related to previously used depreciation allowances.

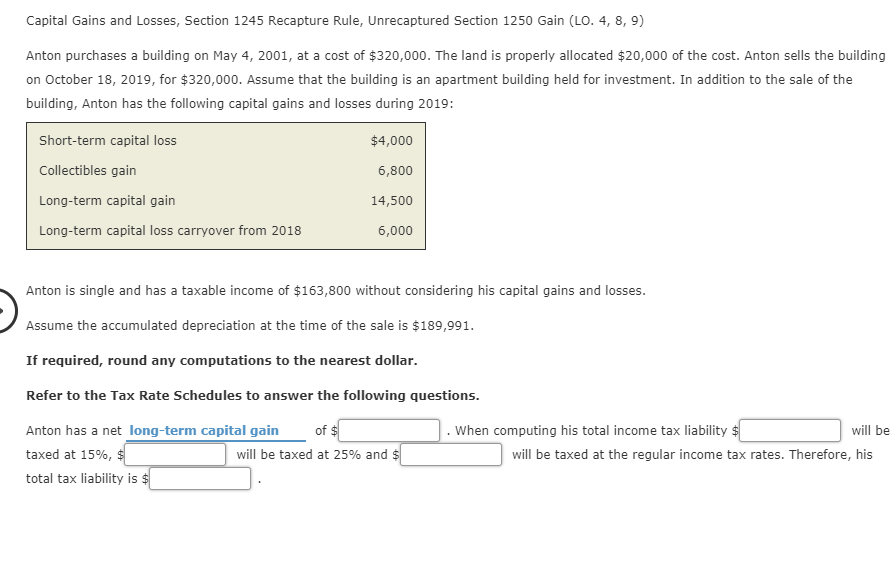

Your client has a total section 1231 gain of 50 000 and 20 000 of that gain is an unrecaptured section 1250 gain subject to the 25 percent maximum capital gains tax rate. The unrecaptured gain is calculated and reported on the unrecaptured section 1250 gain worksheet. This is jack s only transaction involving a capital asset for the year.

Recaptured And Unrecaptured Real Estate Rental Section 1250 Gain Taxcpe

Publication 523 Selling Your Home Chapter 2 Rules For Sales In 2001 Reporting The Gain

/ScheduleD-CapitalGainsandLosses-1-d651471c24974ac79739e2ef580b1c35.png)

Schedule D

Https Farmoffice Osu Edu Sites Aglaw Files Site Library Taxpdf Ch 203 20form 204797 281 29 Pdf

Chapter 11 Investments Howard Godfrey Ph D Ppt Video Online Download

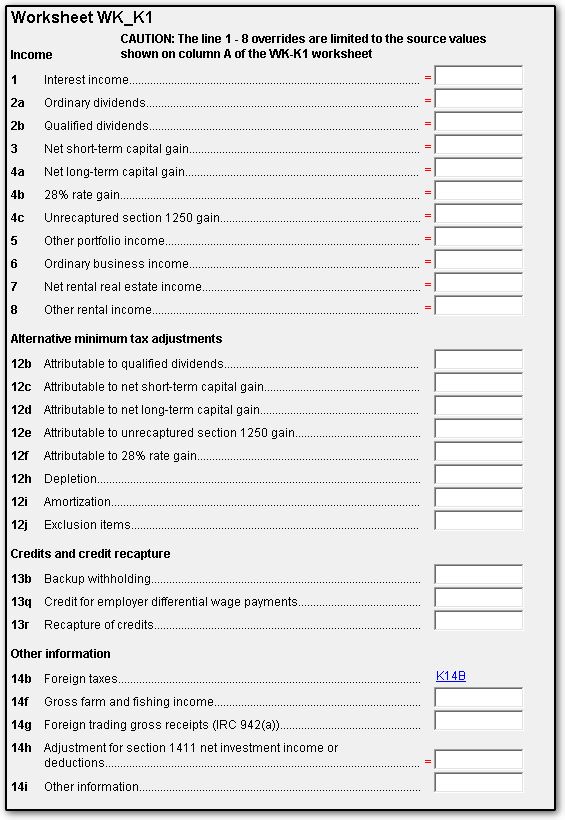

1041 Wkk1 Screen For Worksheet K1 K1

Ppt Sales And Exchanges Of Partnership Interests Powerpoint Presentation Id 4110851

Solved Based Only On The Example Provided Fil Out The Fo Chegg Com

2013 2014 2015 2016 2017 Ordinary Taxable Income S Chegg Com

Long Term Capital Gains Rate 2019 Ardusat Org

Based Only On The Example Provided Fil Out The Form Below With The Ordinary Income And Homeworklib

1231 1245 And 1250 Property Used In A Trade Or Business

Final Review Session Ba 128a Ppt Download