Section 754 Election Statement Example

Https Checkpointlearning Thomsonreuters Com Liveevent Download Location Prod Ecom H0191 Westlan Com Cpl Prod Marketing Webinarattachments 1369 12 29 16 20w238t Pdf Filename 12 29 16 20w238t Pdf

Chapter 13 Basis Adjustments To Partnership Property Ppt Download

Section 754 And Basis Adjustments Pdf Free Download

Https Www Enterprisecommunity Org Sites Default Files Media Library Financing And Development Asset Management 2019 Tax Return Prep Guide Pdf

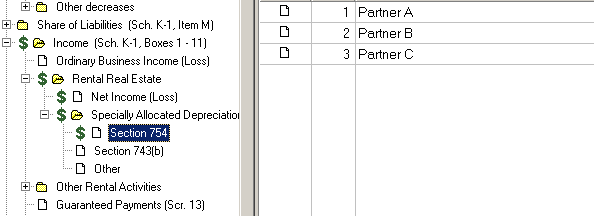

Entering Section 754 743 B Or Other Specially All Intuit Accountants Community

List Ui Design Principles And Examples Justinmind In 2020 Ui Design Ui Design Principles

Section 754 election 1065 only under section 754 a partnership may elect to adjust the basis of partnership property when property is distributed or when a partnership interest is transferred.

Section 754 election statement example. Distribution of partnership property or transfer of an interest by a partner. This will print an election statement. Section 754 allows a partnership to make an election to step up the basis of the assets within a partnership when one of two events occurs.

The partnership referred to in this paragraph is. A valid election under sec. The purpose of a section 754 election is to reconcile a new partner s outside and inside basis in the partnership.

The above scenario can be remedied by the fund making a section 754 election and adjusting the basis pursuant to section 743 b. Id taxpayer name hereby elects under code sec. Partnership name partnership address.

1 754 1 b to apply the provisions of code secs. Pursuant to irc section 1 754 1 b 1 the partnership hereby elects to adjust the basis of the partnership property for the tax year ended 12 31 08. The adjustment in the basis of the assets of the partnership is equal to the transferee partner s initial basis in the partnership less his proportionate share of the adjusted basis of the partnership assets.

The statement required by this subparagraph shall set forth the name and address of the partnership making the election be signed by any one of the partners and contain a declaration that the partnership elects under section 754 to apply the provisions of section 734 b and section 743 b. The manager shall upon the written request of any member cause the company to file an election under section 754 of the code and the treasury regulations promulgated thereunder to adjust the basis of the company s assets under section 734 b or 743 b of the code and a corresponding election under the applicable sections of state and local law. 754 could substantially benefit the owners of entities treated as partnerships for tax purposes i e general partnerships limited partnerships limited liability companies limited liability partnerships and other multimember entities for which a check the box election was made to treat the entity as a partnership for tax purposes or for which the default classification in the absence of an election is to treat the entity as a partnership because it allows a.

At the request of any member the company shall elect pursuant to section 754 of the code to adjust the basis of the company property as permitted and provided in sections 734 and 743 of the code and shall cause its subsidiaries to make similar elections if available such election shall be effective solely for federal and if applicable state and local income tax. The election is effective. The current regulation requires that the section 754 election statement i set forth the name and address of the partnership making the election ii be signed by any one of the partners and iii contain a declaration that the partnership elects under section 754 to apply the provisions of section 734 b and section 743 b.

Https Www Drakesoftware Com Sharedassets Manuals 2017 Partnerships Pdf

Show Me Your Hypothesis Hypothesis 6th Grade Science Teaching Writing

Https Www Thompsonhine Com Uploads 1136 Doc Domestic Taxable Mergers And Acquisitions Pdf

Https Www Houstoncpa Org Docs Librariesprovider2 Tax Expo 2020 205 345p Track 1 Overview Of Partnership Accounting And New Tax Return Reporting Updated Pdf Sfvrsn 143ac0b1 2

Partnerships And Llc S The Basics Of Making A 754 Election Marcum Llp Accountants And Advisors

Making A Valid Sec 754 Election Following A Transfer Of A Partnership Interest

Https Resources Taxschool Illinois Edu Taxbookarchive 2017 B5 Partnership Issues Pdf

Partnership Taxation What You Should Know About Section 754 Elections

The Rccs Twitter Story Story Twitter Comprehensive School

List Ui Design Principles And Examples Justinmind In 2020 Ui Design Ui Design Principles

The Immediate Impact Of 754 Elections When Selling Buying Or Liquidating Partnership Interest By John G Ebenger Cpa Berkowitz Pollack Brant Advisors And Accountants

Beadvicese Business And Financial Wordpress Theme 68672 Veb Dizajn Dizajn Dizajn Sajta

Https Farmoffice Osu Edu Sites Aglaw Files Site Library Taxpdf 2019 4 20llc 20issues 20lawrence 20bw Pdf