Section 754 Election Death Of Partner

Https Checkpointlearning Thomsonreuters Com Liveevent Download Location Prod Ecom H0191 Westlan Com Cpl Prod Marketing Webinarattachments 1369 12 29 16 20w238t Pdf Filename 12 29 16 20w238t Pdf

Making A Valid Sec 754 Election Following A Transfer Of A Partnership Interest

Chapter 13 Basis Adjustments To Partnership Property Ppt Download

Section 754 And Basis Adjustments Pdf Free Download

Https Www Oataxpro Com Assets Files Presentations Be 21 Partnership Termination On Sale Etc Pdf

Ppt Partnership Termination And Transfer Of A Partner S Interest Amanda Wilson February 21 2013 Powerpoint Presentation Id 3321120

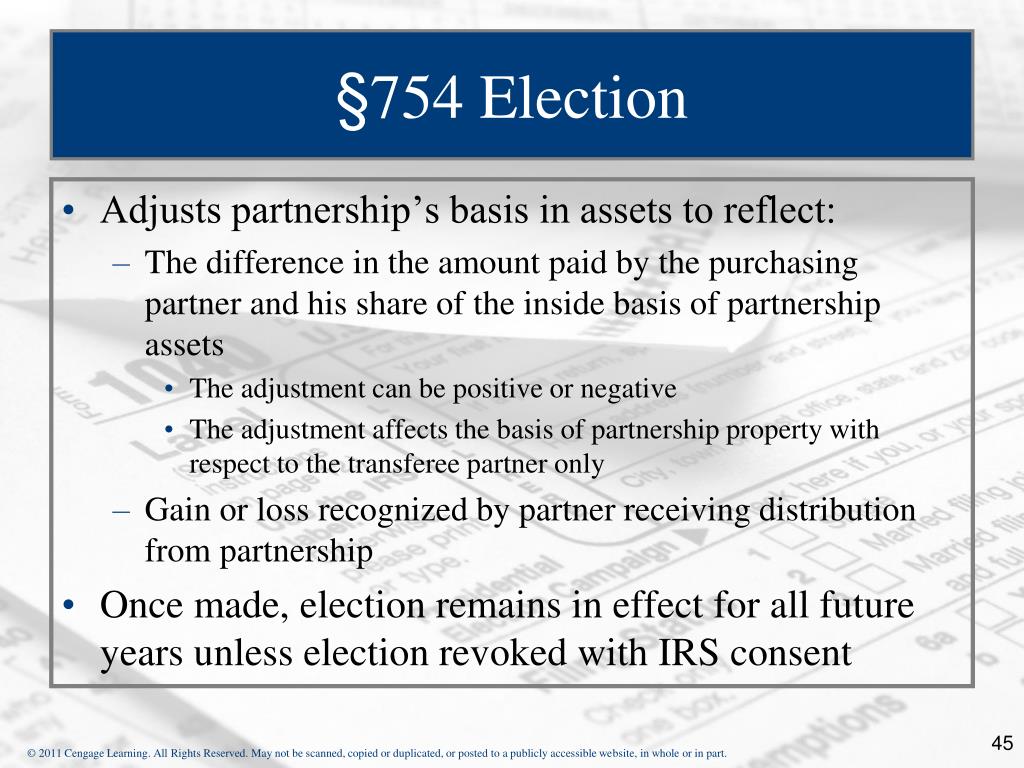

Section 754 allows a partnership to make an election to step up the basis of the assets within a partnership when one of two events occurs.

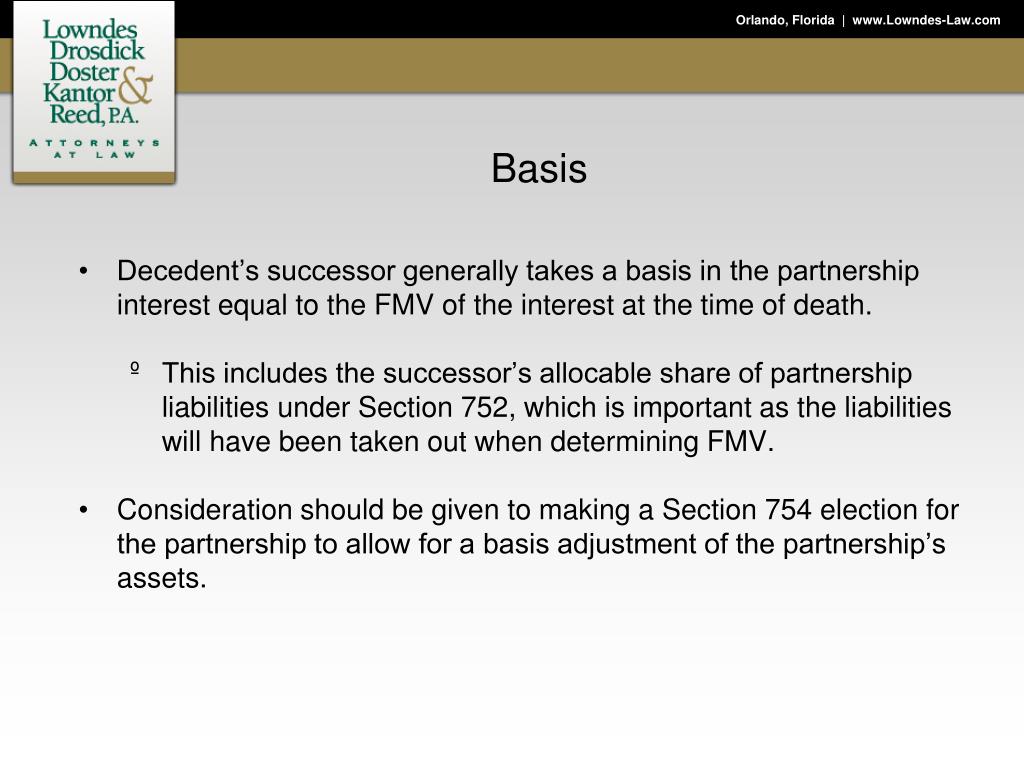

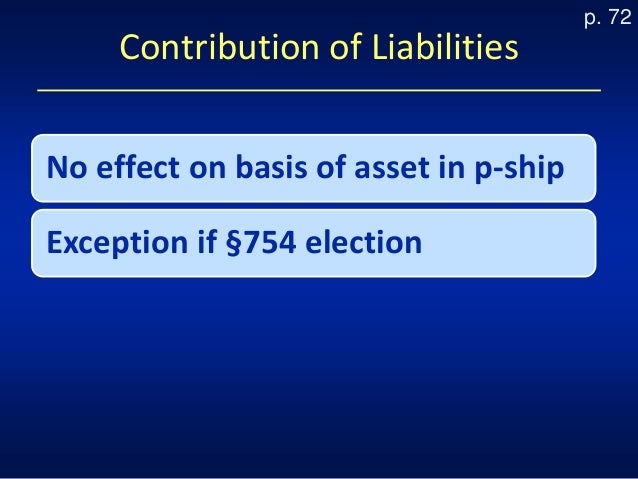

Section 754 election death of partner. There are two sections in subchapter k that allow for basis adjustment if a section 754 election is in place when the inside and outside basis differ. 754 provides an election to adjust the inside bases of partnership assets pursuant to sec. However to claim this adjustment the partnership itself must have an irc sec.

If the partnership has in effect or if it timely makes an election under sec. 754 of the code the estate will receive a special basis adjustment to its share of the partnership s basis for its assets derived from the estate s basis for its partnership interest at the date of the deceased partner s death. Section 743 transfer of an interest in a partnership by sale or exchange or on death of a partner.

A transferee that acquires on the death of a partner an interest in a partnership with an election under section 754 in effect for the taxable year of the transfer must notify the partnership in writing within one year of the death of the deceased partner. 754 election can also be made when a member s interest is sold or upon certain distributions of partnership assets. If the partnership desires to make an election under sec.

A few years after my mother s death the partners sold one of the properties. 754 election in effect or must make the election for the year that includes the deceased partner s date of death. After consulting with a cpa we decided to make a section 754 election to step up our basis in the partnership assets.

743 b upon the transfer of a partnership interest caused by a partner s death. If the partnership has a section 754 election in effect or if it makes a section 754 election the partnership may increase the basis of its capital and section 1231 assets by 1 000 in the year. 754 election can only be made by the partnership.

743 b an election must be made with a timely filed partnership return. This allowed us to reduce current income allocated to us and reduce taxable gain on the disposition of the partnership s assets.

Chapter 11 Partnerships Distributions Transfer Of Interests Ppt Video Online Download

Ppt Chapter 11 Powerpoint Presentation Free Download Id 270938

Could The 754 Election Benefit Your Partnership Ds B

Developments Affecting M A Deal Structure Ppt Download

Partnership Taxation What You Should Know About Section 754 Elections

Tax Implications Of Liquidation Of Partnerships And Family Limited Partnerships Eugene F Pollingue Jr Ppt Download

Limited Liability Companies Llc Electing Partnership Vs S Corpora

Orlando Florida 407 Partnership Termination And Transfer Of A Partner S Interest Amanda Wilson Ppt Download

Partnerships And Llc S The Basics Of Making A 754 Election Marcum Llp Accountants And Advisors

4 31 2 Tefra Examinations Field Office Procedures Internal Revenue Service

Https Www Houstoncpa Org Docs Librariesprovider2 Tax Expo 2020 205 345p Track 1 Overview Of Partnership Accounting And New Tax Return Reporting Updated Pdf Sfvrsn 143ac0b1 2

How The Death Of A Partner Could Affect A Partnership S Year End

Estate Planning For The 99 Of Us For Estates Under 11 4 Million Ppt Download