Section 6114 Or 7701 B

Form 8833 Treaty Based Return Position Disclosure Under Section 6114 Or 7701 B Youtube

Form 8833 Treaty Based Return Position Disclosure Under Section 6114 Or 7701 B 2013 Free Download

Irs Form 8833 Download Fillable Pdf Or Fill Online Treaty Based Return Position Disclosure Under Section 6114 Or 7701 B Templateroller

Instructions For Form 5471 02 2020 Internal Revenue Service

Form 8833 Example Fill Online Printable Fillable Blank Pdffiller

3 11 213 Form 1066 U S Real Estate Mortgage Investment Conduit Remic Income Tax Return Internal Revenue Service

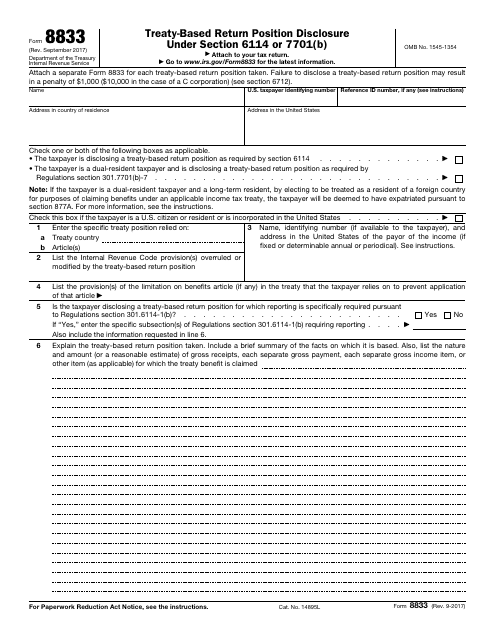

Us taxpayers use this form to be compliant with internal revenue code section 6114 while dual resident taxpayers need it to make the treaty based return position disclosure required by regulations section 301 7701 b 7.

Section 6114 or 7701 b. Dual resident are also required to make the treaty based return position disclosure required by regulations section 301 7701 b 7 coordination with income tax. Taxpayers use form 8833 to make the treaty based return position disclosure required by section 6114. Fillable treaty based return position disclosure under section 6114 or 7701 b form 8833 fill online printable fillable blank treaty based return position disclosure under section 6114 or 7701 b form 8833 form use fill to complete blank online irs pdf forms for free.

A separate form is required annually for. Effective date of 1990 amendment. Disclosure required by section 6114 and the regulations thereunder regulations section 301 6114 1.

Form 8833 tax treaty provisions and expat tax returns. The 8833 form is generally used by us taxpayers to make tax treaty based return position disclosures to the irs required by irc section 6114 with a separate form for each treaty based return position taken. When reporting is required under this section for a return relating to a taxable year for which the due date without extensions is after december 15 1997 the taxpayer must furnish in accordance with paragraph a of this section as an attachment to the return a fully completed form 8833 treaty based return position disclosure under section 6114 or 7701 b or appropriate successor form.

Once completed you can sign your fillable form or send for signing. Form 8833 treaty based return position disclosure under section 6114 or 7701 b is used by taxpayers to make a treaty based return position disclosure as required by section 6114 or such dual resident taxpayers whose treaty based return position disclosure is required under reg. When congress enacted section 7701 b it recognized that an individual who would be treated as a resident alien under section 7701 b 1 a might be treated as a nonresident alien under the so called tie breaker rules of the income tax treaties to which the u s is a party 12 the remainder of this article explores how these tie breaker treaty rules can or not be impacted by section 6114.

A prior section 6114 was renumbered 6116 of this title. This file was special though as it gave me the opportunity to drill down on irc section 6114 treaty based return positions. The form must also be used by dual resident taxpayers defined later to make the treaty based return position disclosure required by regulations section 301 7701 b 7.

Technically the form is referred to as form 8833 treaty based return position disclosure under section 6114 or 7701 b. Taxpayer wants to rely on an international tax treaty that the united states has entered into regarding tax law sometimes they have to file an additional form with their tax return when filing with the irs.

3 11 12 Exempt Organization Returns Internal Revenue Service

Form 8833 How To Claim Income Tax Treaty Benefits Nomad Capitalist

3 12 217 Error Resolution Instructions For Form 1120 S Internal Revenue Service

Pin On World War Earl

3 12 220 Error Resolution System For Excise Tax Returns Internal Revenue Service

3 11 6 Data Processing Dp Tax Adjustments Internal Revenue Service

3 11 15 Return Of Partnership Income Internal Revenue Service

2000 Form Irs 8833 Fill Online Printable Fillable Blank Pdffiller

Instructions For Form 1040 Nr 2019 Internal Revenue Service

B 17 Mid Air Collision Thread Wwii B17 Winning Run Last Mission With Images Wwii Aircraft Reconnaissance Aircraft Wwii Plane

Form 8833 Fillable Treaty Based Return Position Disclosure Under Section 6114 Or 7701 B

3 21 3 Individual Income Tax Returns Internal Revenue Service

Irs 8833 2013 Fill Out Tax Template Online Us Legal Forms