Section 475 F Election

Updated Massive Market Losses Elect 475 For Enormous Tax Savings

Traders Elect Section 475 For Massive Tax Savings

Consider 475 Election By Tax Deadline To Save Thousands

Section 475 Mark To Market Election Accounting Consulting Trader S Accounting

Sec 475 Mark To Market Election

Time Is Ticking To Make A Mark To Market Section 475 F Election

Tts traders as sole proprietor individuals now have to july 15 2020 to elect section 475 f for 2020 as the 475 mtm election is an attachment to a specified form either f1040 or.

Section 475 f election. The trader can make an election under irc 475 f 1 to use the mark to market method of accounting for any securities held on the last day of the taxable year. 475 f which allows taxpayers to make what is known as the mark to market election. The provision offering these underused advantages is sec.

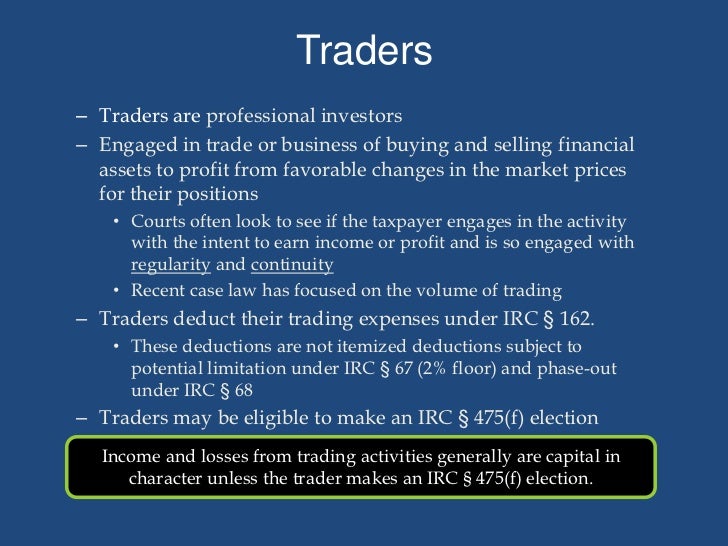

A fund must be a trader and not an investor in order to be able to make a section 475 f election. The section 475 election procedure is different for new taxpayers like a new entity. Additionally all realized gains losses will be treated as ordinary income loss and not as capital gain loss.

If a trader makes that election the gains or losses are treated as ordinary and not capital thus no 3 000 per year limit is imposed on deducting the losses. Section 475 f provides that a trader in securities or commodities can make elections to mark to market their securities and or commodities and treat increases or decreases in value as ordinary.

Mark To Market Election Whether To Make Or Revoke A Section 475 F Election On Or Before March 16 2020 Kleinberg Kaplan

Basic Tax Considerations Affecting Hedge Funds

Mark To Market Election For Hedge Funds

Mark To Market Accounting For Traders Youtube

The Lure Of A Sec 475 Election

Alert Mark To Market Tax Election Deadline For Partnerships Sadis Goldberg Llp

Reminder Deadline To Make A Section 475 F Election For Most Calendar Year Partnership Funds Is Tomorrow Monday March 16 Lexology

Simplest Form Lowest Term Ten Common Mistakes Everyone Makes In Simplest Form Lowest Term Writing Fractions Common Core Math Fractions Simplest Form Fractions

Tool Socrative Student Response System Educationation Excercises And Games Via Smartphones Laptops And Tablet Socrative Teacher Signs Teacher

I Want Out Revoking Your Section 475 E Or F Election Marcum Llp Accountants And Advisors

Egypt Uprising Power Of The People Jpg 305 475 Egyptuprisingpowerofthepeoplejpg Protest Posters In 2020 Revolution Art Protest Posters Protest Art

This Handy Metric Conversion Guide For Knitting And Crochet Will Help You To Convert Yarn Weight Cooking Conversions Metric Conversions Metric Conversion Chart

Printable Oven Temperature Conversion Chart Temperature Conversion Chart Oven Temperature Conversion Baking Conversion Chart