Section 409a Regulations

Https Www Friedfrank Com Sitefiles Publications 4051c4d3cdccafea809ecfdb7a31e0ad Pdf

Section 409a Top 10 Rules For Compliant Non Qualified Deferred Compensation

Section 409a Handbook Second Edition Bloomberg Law Books

Https Www Fenwick Com Fenwickdocuments Execu Comp 04 16 07 Pdf

Https Www Ipbtax Com Media Publication 86 Code 20section 20409a 20hidden 20deferred 20compensation Pdf

Application Of Section 409a To Nonqualified Deferred Compensation Plans Us Internal Revenue Service Regulation Irs 2018 Edition The Law Library 9781729682548 Amazon Com Books

We are not attorneys so we will leave the legal minutiae of that definition for others to grapple with noting only that generally speaking a deferred compensation plan is an arrangement whereby an employee service provider in 409a parlance receives compensation in a later tax year.

Section 409a regulations. Service recipients are generally employers but those who hire independent contractors are also service recipients. What qualifies as a separation from service in certain m a transactions. Section 409a of the united states internal revenue code regulates nonqualified deferred compensation paid by a service recipient to a service provider by generally imposing a 20 excise tax when certain design or operational rules contained in the section are violated.

Vii payment upon income inclusion under section 409a. Section 409a applies to all companies offering nonqualified deferred compensation plans to employees. Viii cancellation of deferrals following an unforeseeable emergency or hardship distribution.

108 357 set out below subsection b of section 409a of the internal revenue code of 1986 shall take effect on january 1 2005. Section 409a a provides requirements on the deferral and payment of nonqualified deferred compensation. A plan does not satisfy the requirements of section 409a and this section and 1 409a 2 through 1 409a 3 and 1 409a 5 through 1 409a 6 unless the plan is established and maintained by a service recipient in accordance with the requirements of this section 1 409a 2 through 1 409a 3 and 1 409a 5 through 1 409a 6.

X certain distributions to avoid a nonallocation year under section 409 p. 1 the service provider s separation from service as defined in 1 409a 1 h and in accordance with paragraph i 2 of this section. Iv section 457 plans.

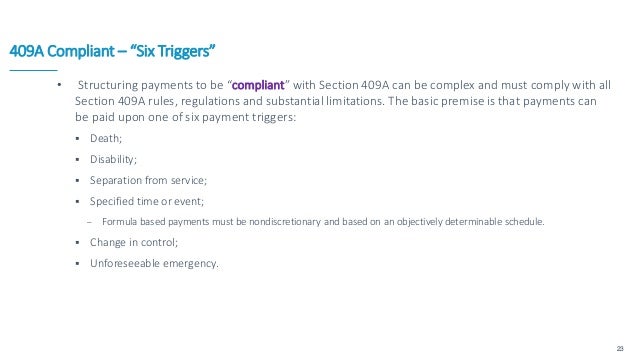

The requirements of section 409a a 2 a are met only if the plan provides that an amount of deferred compensation under the plan may be paid only upon an event or at a time set forth in this paragraph a. Notwithstanding section 885 d 1 of the american jobs creation act of 2004 pub. The proposed regulations state that the plan termination provision noted above is not ambiguous and that the section 409a final regulations currently require that all similar deferred compensation plans within.

The regulations provide a definition of a nonqualified deferred compensation plan subject to section 409a including rules related to the statutory effective date and rules governing initial and subsequent deferral elections the establishment of the time and form of payment. Final regulations set forth guidance on the application of section 409a to nonqualified deferred compensation plans. Vi payment of employment taxes.

Taxation Of Deferred Compensation Under Irc Section 409a Meridian Compensation Partners Llc Executive Compensation Consulting

Section 409a Regulations Irs Changes Affect Nonqualified Deferred Comp And Stock Plans The Mystockoptions Blog

Love And Section 409a In The Time Of Covid 19

409a Guidance On Nonqualified Deferred Compensation Plans For Beginne

Deferred Compensation Plan Best Practices And Irc Section 409a Nonqualified Nq Deferred Compensation For Plan Sponsor Use Only Updated October Ppt Download

Sections 409a And 457 Answers To 250 Frequently Asked Questions Lexisnexis Store

Nonqualified Deferred Compensation Plans And Section 409a Plansponsor

Irs Publishes New Proposed Regulations On Section 409a

Section 409a Valuations Dla Piper Accelerate

Https Www Sgrlaw Com Wp Content Uploads 2014 02 Humanresourcesauthority091207 Pdf

Possible Options For Participant Relief Under Section 409a Plans In The Time Of Coronavirus Groom Law Group

Irc Section 409a V Covid 19 The Nonqualified And Executive Compensation Clash And How Employers Can Navigate It

Http Www Buchalter Com Wp Content Uploads 2013 06 Client Alert 409a Pdf