Section 409a Irc

Irc 409a Overview 409a Valuations Explained Equityeffect

Irc Section 409a

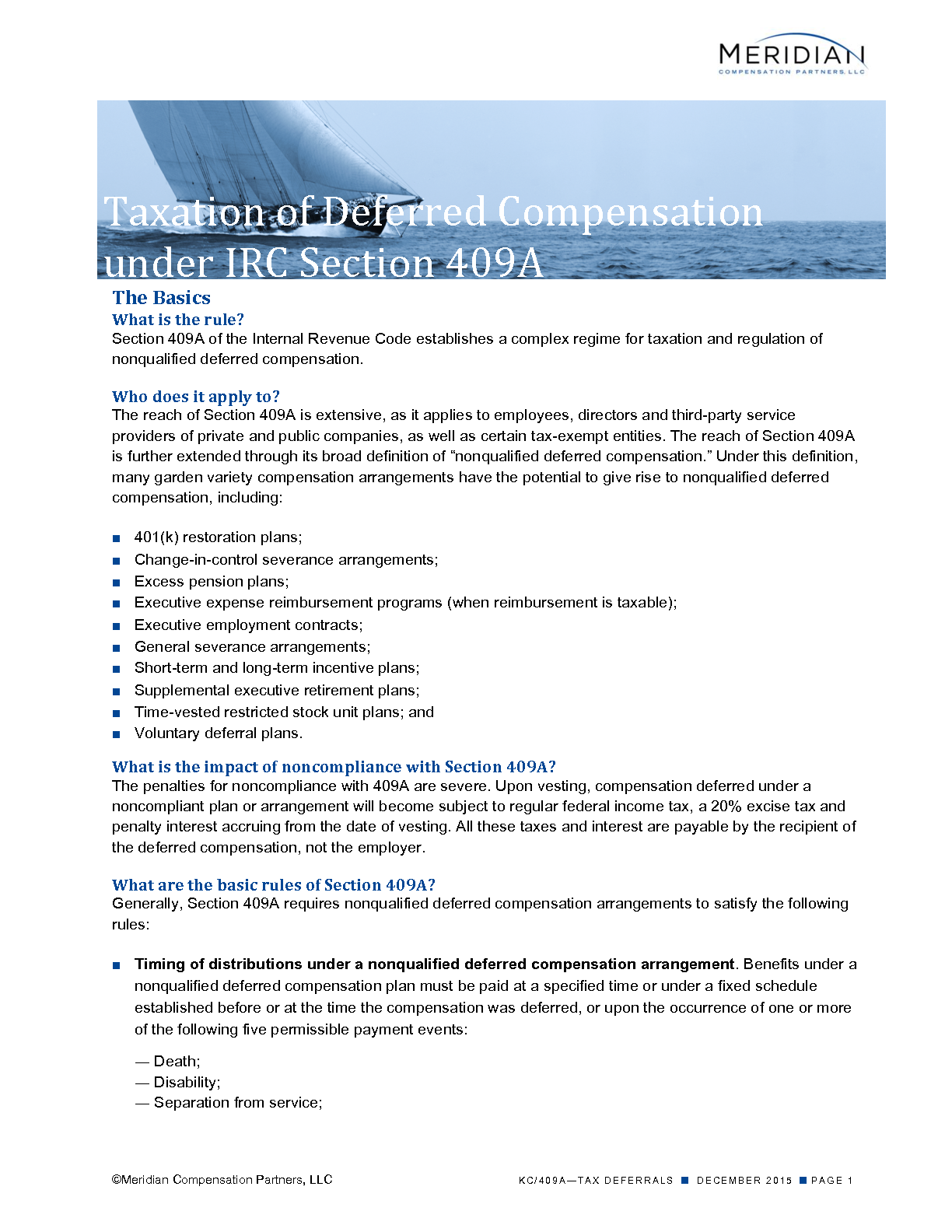

Taxation Of Deferred Compensation Under Irc Section 409a Meridian Compensation Partners Llc Executive Compensation Consulting

Irs 409a Valuations Morning Investments

Section 409a Top 10 Rules For Compliant Non Qualified Deferred Compensation

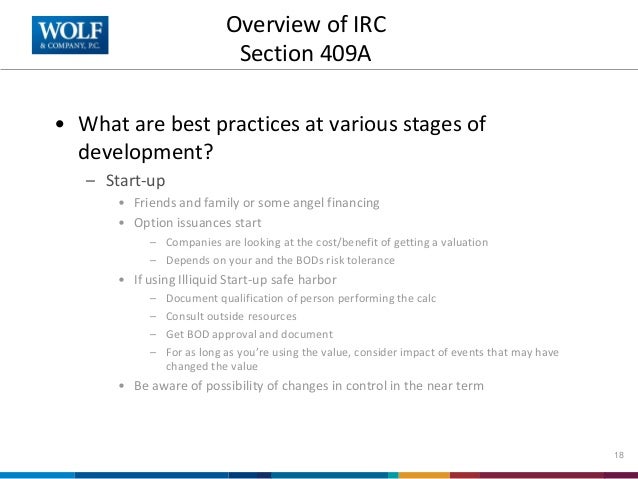

Guidance On Deferred Compensation Irc 409a And Irc Ppt Download

Notwithstanding section 885 d 1 of the american jobs creation act of 2004 pub.

Section 409a irc. Internal revenue code section 409a was designed to address perceived abuses by executives who used their authority to accelerate distributions in deferred compensation plans while knowing that the companies they represented were approaching financial ruin. The regulations provide a definition of a nonqualified deferred compensation plan subject to section 409a including rules related to the statutory effective date and rules governing initial and subsequent deferral elections the establishment of the time and form of payment. Ix plan terminations and liquidations.

Viii cancellation of deferrals following an unforeseeable emergency or hardship distribution. 109 135 provided the following. Read the code on findlaw.

Vi payment of employment taxes. Final regulations set forth guidance on the application of section 409a to nonqualified deferred compensation plans. 409a affects nonqualified retirement plans and other deferred compensation arrangements.

Section 409a of the united states internal revenue code regulates nonqualified deferred compensation paid by a service recipient to a service provider by generally imposing a 20 excise tax when certain design or operational rules contained in the section are violated. A plan does not satisfy the requirements of section 409a and this section and 1 409a 2 through 1 409a 3 and 1 409a 5 through 1 409a 6 unless the plan is established and maintained by a service recipient in accordance with the requirements of this section 1 409a 2 through 1 409a 3 and 1 409a 5 through 1 409a 6. An internal revenue code section 409a primer by tony ling and galen mason1 the american jobs creation act of 2004 was signed into law on october 22 2004.

According to will fogleman associate at groom law group in washington d c the new section was created mostly in response to the enron scandal. It created a new section 409a of the internal revenue code 409a and the code respectively. Iv section 457 plans.

X certain distributions to avoid a nonallocation year under section 409 p. Service recipients are generally employers but those who hire independent contractors are also service recipients. The american jobs creation act of 2004 was signed into law on october 22 2004.

Know Your Valuation For Equity Compensation And Avoid The Perils Of

What Is A 409a Valuation Carta

Irc Section 409a V Covid 19 The Nonqualified And Executive Compensation Clash And How Employers Can Navigate It

Irc Section 409a V Covid 19 Fulcrum Partners Llc

Defining Separation From Service Under Irc Section 409a

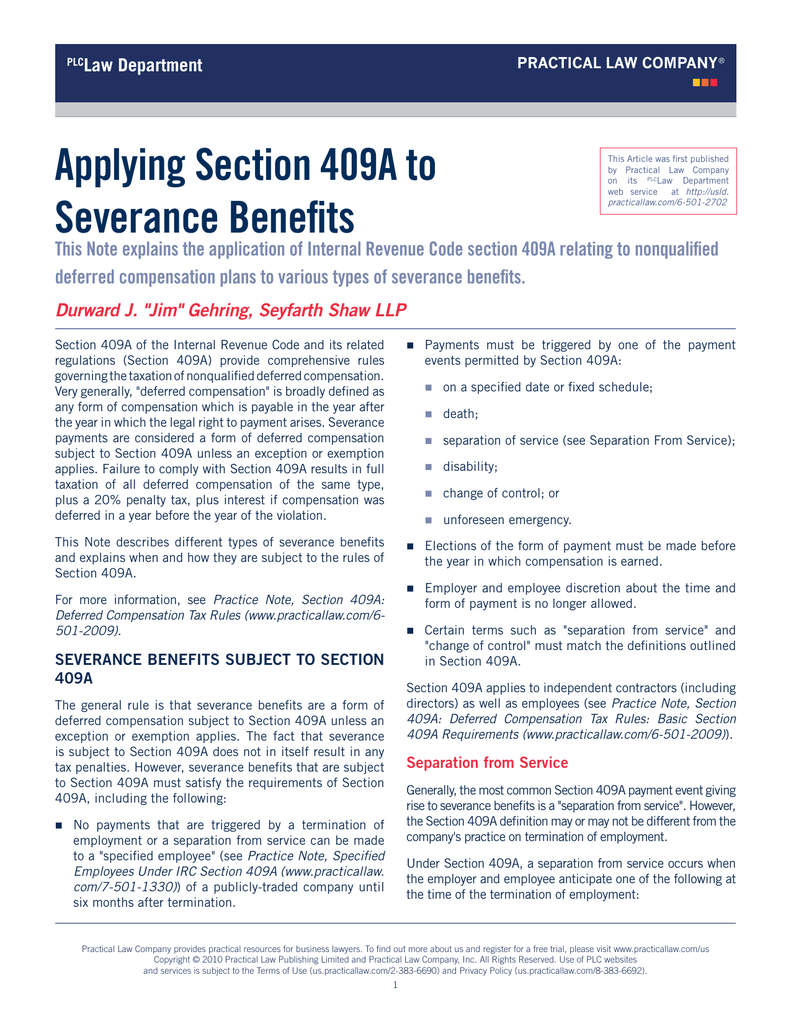

Applying Section 409a To Severance Benefits

Irc Section 409a Simple409a Com

Proposed Changes Clarifications And Additions To Deferred Compensation Agreements Under Irc Section 409a Sikich Llp

Section 409a Handbook Second Edition Bloomberg Law Books

Carta Discusses The Flaws In The 409a Valuations Process By Carta Owner S Manual Blog By Carta Medium

How To Fix Broken Legislation In The 409a Process Carta

Section 409a Valuations Dla Piper Accelerate

Play By The Rules