Section 351 Of The Internal Revenue Code

Startup Law A To Z Corporate Matters Start Up Corporate Counsel Right Of First Refusal

Section 351 Transaction U S Corporate Tax Youtube

Ch4 Tax Solutions Q A Law 794 Corporate Tax Slu Studocu

Instructions For Form 5471 02 2020 Internal Revenue Service

Section 351 Transaction With The Transfer Of Services U S Corporate Tax Youtube

Solved Business Environment And Concepts Solutionzip Business Structure Solutions Corporate Law

Internal revenue code section 351.

Section 351 of the internal revenue code. Transfer to corporation controlled by transferor. Code unannotated title 26. Section 351 a is intended to apply to certain transactions where gain or loss may have accrued in a constitutional sense but where in a popular and economic sense there has been a mere change in the form of ownership and the taxpayer has not really cashed in on the theoretical gain or closed out a losing venture.

The amendments made by this section amending this section and sections 355 358 and 368 of this title shall not apply to any distribution pursuant to a plan or series of related transactions which involves an acquisition described in section 355 e 2 a ii of the internal revenue code of 1986 or in the case of the amendments made by. Internal revenue code 351. For a description of the requirements of 351 see text accompanying notes 14 18 infra.

Tained in 351 of the internal revenue code the code. 351 u s. No gain or loss shall be recognized if property is transferred to a corporation by one or more persons solely in exchange for stock in such corporation and immediately after the exchange such person or persons are in control as defined in section 368 c of the corporation.

351 a general rule.

4 61 12 Foreign Investment In Real Property Tax Act Internal Revenue Service

Achieving Tax Free Rollover Treatment For Certain Shareholders In Acquisition Of Publicly Traded Target Company Tax United States

Https Investors Linde Com Media Linde Investors Documents Linde Ag Tax Form 8937 Pdf La En Rev E07743ed50b84f4ca9638c5e2066d6ef

M A Tax For 2019

How To Buy A Duplex The Ultimate Step By Step Guide Being A Landlord Real Estate Investing Buying A Rental Property

Boot And Relief Of Owner S Liabilities Henssler Financial

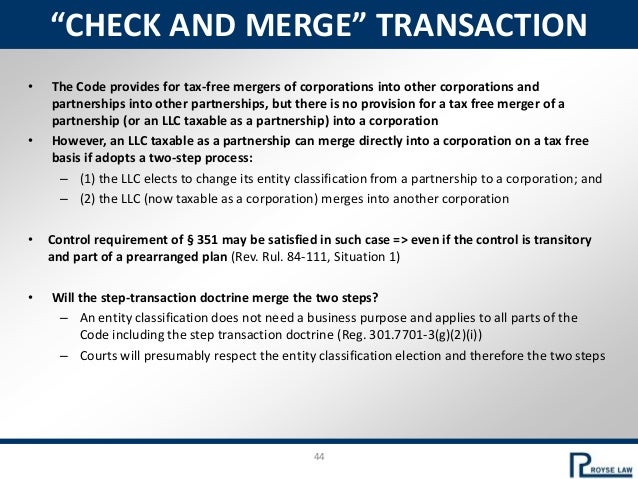

Sec 351 Control Requirement Opportunities And Pitfalls

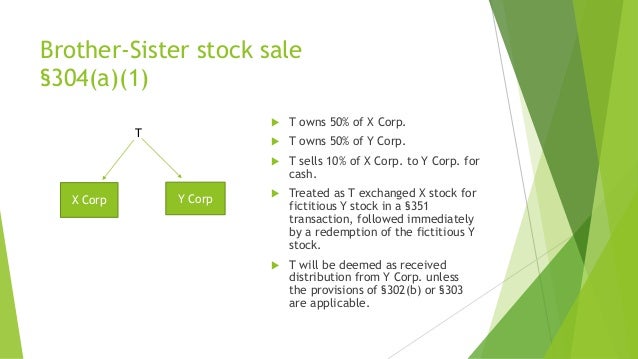

Code Sec 304 Related Party Stock Sales

Http Www Mvlandbank Com Documents Transferfee Regulations 000 Pdf

2019 2020 Kansas Legal Directory Pages 351 400 Flip Pdf Download Fliphtml5

Requirements For Nonrecognition Of Gain Or Loss On Transfer Of Property To A Corporation Irc 351 Taxconnections

Architektur Aktuell 354 09 2009 Stahl Alu Architect Ebay House

2020 Georgia Legal Directory Pages 351 400 Flip Pdf Download Fliphtml5