Section 280g S Corporation

Golden Parachute Payments Under Section 280g Valuation Research

Noncompete Agreements For Section 280g Compliance For Banks Mercer Capital

Plez 2018 19 On Behance With Images Sandwich Shops Cafe Branding Organic Drinks

Section 280g Golden Parachutes Meridian Compensation Partners Llc Executive Compensation Consulting

Pasini Law Golden Parachutes And Section 280g An Overview And Practice Tips

Cloudnola Flipping Out A Sleek Clock With Retro Designs And Modern Materials Cafe Menu Design Menu Design Menu Design Inspiration

What is a disqualified individual.

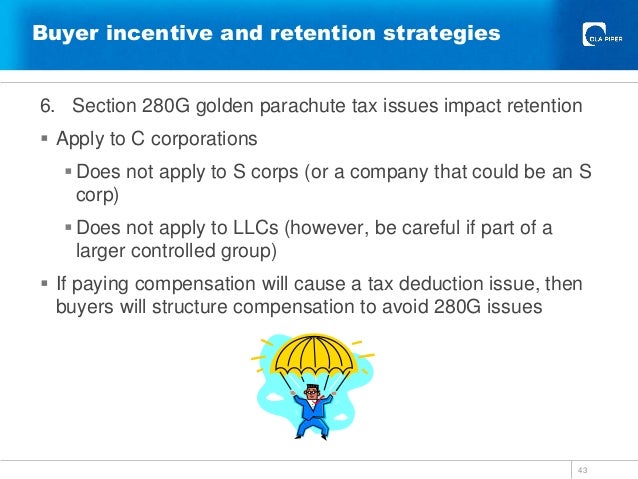

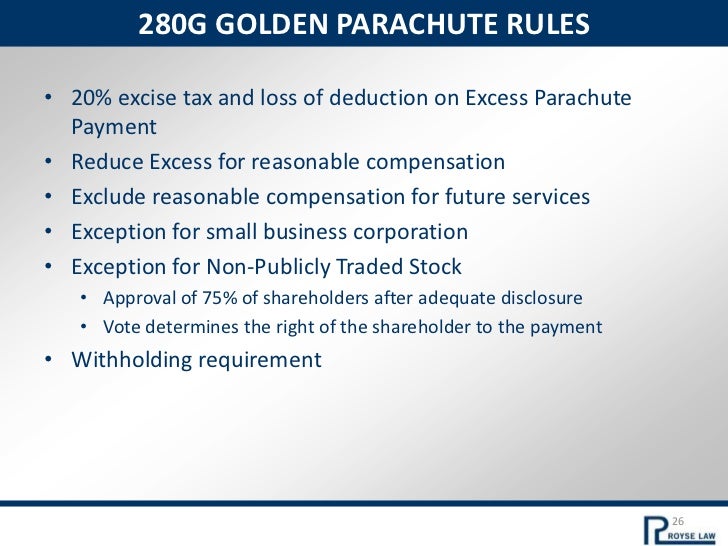

Section 280g s corporation. The secretary may by regulations prescribe that the requirements of subclause i of clause ii are not met where a substantial portion of the assets of any entity consists directly or indirectly of stock in such corporation and interests in such other entity are readily tradeable on an established securities market or otherwise. 280g does not typically apply to companies that are organized as an llc or an s corporation and also does not apply to any c corporation that is eligible to be treated as an s corporation. 280g disallows a deduction to a corporation for an excess parachute payment made to an individual and sec.

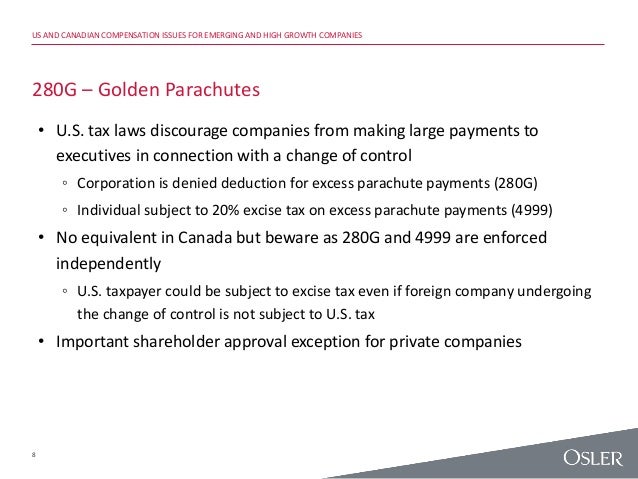

280g relating to golden parachute payments and its sec. 280g impacts both the corporate entity and its executives shareholders and other highly compensated individuals associated with the corporation and imposes harsh tax consequences if not properly addressed. Section 280g was created to protect the interests of shareholders by stopping corporations from making unreasonably large payments to disqualified individuals when control of a corporation changes hands.

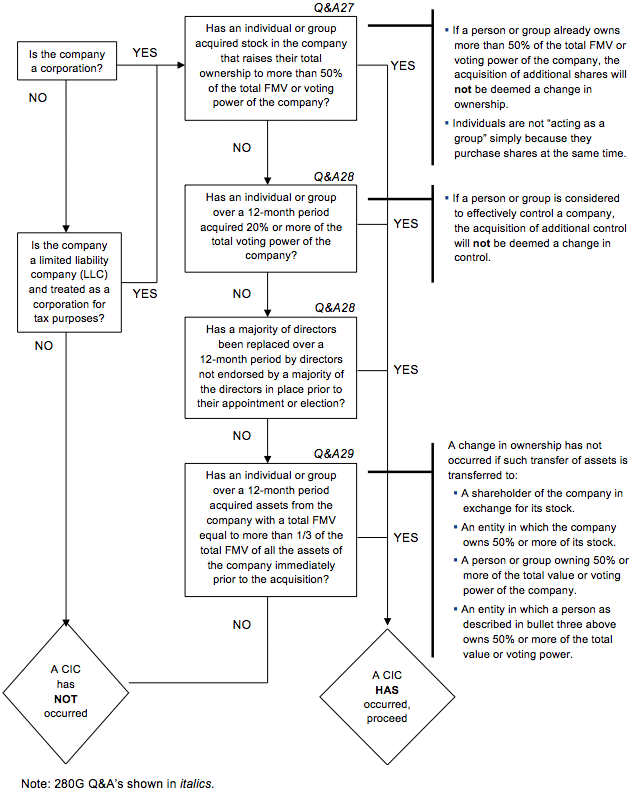

Enter one such term internal revenue code irc section 280g 280g or the golden parachute payment rules a federal tax provision that comes into play when there is a change in control of a corporation. Corporation s makes severance payments to several of its highly compensated individuals that are parachute payments under section 280g and q a 2 of this section. Foreign corporations however are not included in the definition and therefore cannot rely on this exception.

It does not apply to s corps partnerships or llcs that are taxed as partnerships. Final regulationsunder irc section 280g extend the small business corporation definition to include a corporation that would qualify for s corporation status but for the restriction regarding nonresident alien shareholders. Section 280g applies only to corporations both public and private.

Generally the terms are defined as follows. An important one is golden parachutes because there s potential for disqualified individuals to owe excise taxes and companies to lose their tax deduction. Congress added section 280g to the internal revenue code in response to critics of the arrangement to discourage companies from paying golden parachutes.

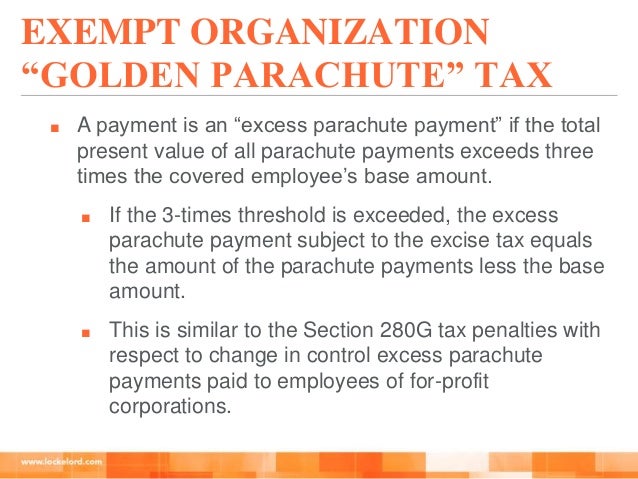

The corporation s stock equals or exceeds one third of the total gross fair market value of the assets of corporation p and thus represents a substantial portion of the assets of corporation p. 280g is triggered when any covered individual receives payments in the nature of compensation in connection with a change of control in excess of 3 times his or her base amount which is defined as his or her average annual compensation over the previous five years pro rated for any. Disqualified individuals include corporate officers shareholders and other highly.

Mark Sevouni Packing Design Chocolatier Dried Fruits

Us And Canadian Compensation Issues For Emerging And High Growth Comp

Key Issues In M A For In House Counsel

Mercer Capital S Noncompete Agreements For Section 280g Compliance

Tax And Corporate Law On Sales And Purchases Of Businesses

Revisiting The Application Of Sec 280g On Partnerships And Llcs

We Were Tasked With Designing The Club And Restaurant S Visual Identities For The Club We Chose To Honour The Night Birds That Flo Book Design Menu Design Club

Xiongyu Shishe Vi On Behance In 2020 Cover Design Packaging Design Graphics Layout

Jack Daniel S Tennessee Whiskey Infused Vanilla Cake Jack Daniels Jack Whiskey

Freda S Peanut Butter Branding Freda S Peanut Butter Are Packed Full Of Good Stuff A Peanut Butter Brands Healthy Peanut Butter Snacks Butter Recipes Homemade

Pin On Gym

Tailored Jacket Fabric 8128 Plain Grey Tailored Jacket Jackets Gentleman Style

Golden Parachutes Under Irc Sections 280g And 4999 Rules Strategies And Tactics Casetext