Section 162 Bonus Plan Drawbacks

Section 162 Executive Bonus Plan And It S Benefits In 2020 Life Insurance Policy Permanent Life Insurance How To Plan

Irc Section 162 Linked Benefit Executive Bonus Plans For Business Owners And Key Employees Bsmg

Reward Key Employees With An Executive Bonus Plan

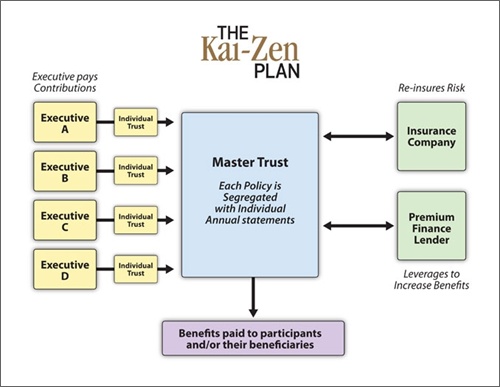

Kai Zen

Plan 56367sm Roomy French Country Home Plan European House Plans French Country House Country House Plans

162 Bonus Plans The Basics Ebs

Disadvantages of executive bonuses.

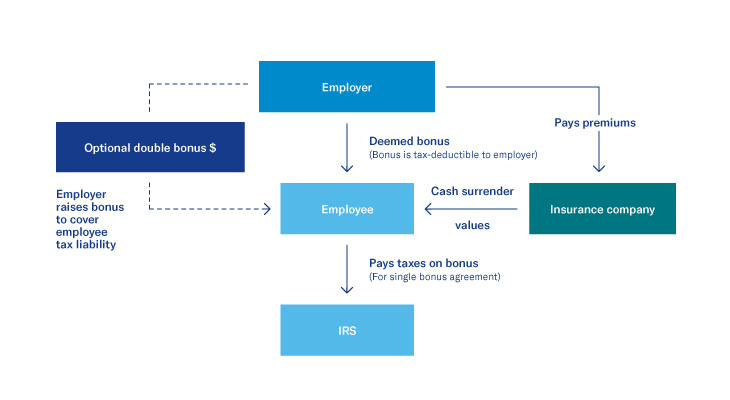

Section 162 bonus plan drawbacks. The company is unable to fully recover its costs from the policy s death benefit since the key executive names the policy beneficiary. 162 bonus plans can create a competitive edge to attract or retain key employees by using employer funded life insurance policies. They allow for business owners or executives to receive additional compensation over and above their traditional compensation in a tax favored manner.

A 162 bonus arrangement is an arrangement where the executive owns a life insurance policy and the company pays the premium. As the economy improves employee talent is at a premium. Among other things because of its simplicity and its potential flexibility throughout the life of the benefit plan the section 162 executive bonus arrangement is deservedly getting new levels of attention.

What is a section 162 executive bonus plan. Once an executive is retirement eligible the plan mandates that the company will need to continue premiums until certain funding guidelines are satsified. The premium is treated as compensation under section 162.

This piece offers insight into section 162 executive bonus plan design considerations marketing opportunities benefits to the business and executive and more. Deferred compensation plans are quite popular and have been around for decades. Well designed executive benefit plans are important tools in both retaining and attracting top talent.

Employers create 162 bonus plans to provide supplemental benefits to select key employees. And one of the simplest forms of these types of plans is a section 162 bonus plan. There are also some inherent disadvantages in using an executive bonus plans including.

The plan can be discriminatory inasmuch as the employer can determine which employees participate in the plan. The bonus is fully deductible to the company. The company can restrict access to the cash value using a controlled bonus arrangement.

Craftsman House Plan The Alder Etsy Shedplans Craftsman House Plan Craftsman House House Plans

Plan 73374hs Exclusive Five Bedroom Craftsman With Sports Court Included In 2020 Building Plans House House Plans Narrow Lot House Plans

Irs Issues Proposed Regulations Clarifying And Expanding Scope Of Code Section 162 M

Management Vs Leadership On Linkedin By Tom Schulte Via Slideshare Leadership Short Essay Leadership Skills

Plan 16502ar Passive Solar House Plan With Bonus Loft Passive Solar House Plans Solar House Plans Passive Solar Homes

Whispering Valley 2235 3 Bedrooms And 2 Baths The House Designers Tuscan House Plans Cottage Style House Plans House Plans

The Bemont Custom Bricks Palmer House Dining Room Paint Colors

Section 162 M After The Tax Cuts And Jobs Act What To Do Now Insights Skadden Arps Slate Meagher Flom Llp

The Latest On Tax Reform And Equity Compensation Equity Methods

9530xl Fillmore Chambers Design Group Mansion Floor Plan Floor Plans Courtyard House Plans

Cottage Style House Plan 3 Beds 2 5 Baths 1281 Sq Ft Plan 410 162 House Plans Cottage Style House Plans Cottage Floor Plans

F43b34b5540fa2dec45f0040ac56d65f8259445b Jpg 800 600

Wow Mit Diesem Trainingsplan In Nur 30 Tagen Zur Idealen Bikini Figur F R Den Sommer Fitness Abnehmen Deutsc In 2020 Crunches Workout Bottom Workout Lower Stomach