Section 1411 Trade Or Business

Section 1411 Net Investment Income Tax Income Tax Investing Income

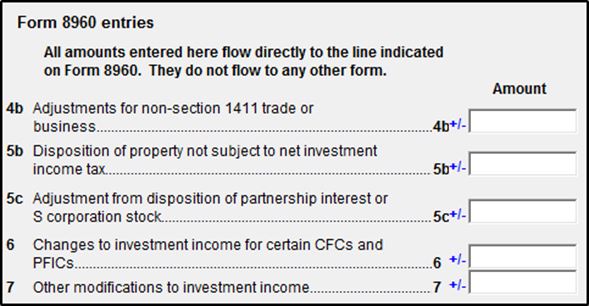

Taxprepsmart How To Figure The Amount For Form 8960 Line 4b

Nbsp Nbsp Bitcoin Nbsp Nbsp Nbsp Nbsp Cryptocurrency Nbsp Nbsp Nbsp Nbsp Crypto Nbsp Nbsp Nbsp Nbsp Blockchain Nbsp Nbsp Nbsp Nb Goruntuler Ile

8960 Net Investment Income Tax 8960 K1 Schedulec Schedulee Schedulef

New Sec 1411 Brings Difficulty Defining Real Estate Trade Or Business

Understanding The Net Investment Income Tax

Section 1411 trade or business.

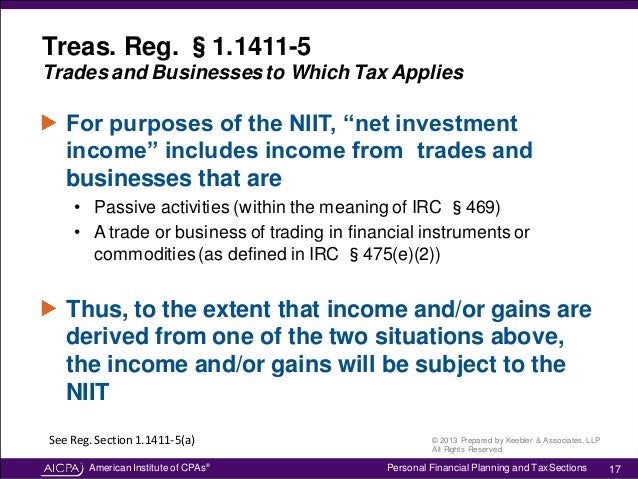

Section 1411 trade or business. The niit applies at a rate of 3 8 to certain net investment income of individuals estates and trusts that have income above the statutory threshold amounts. Generally a trade or business that s either a passive activity for the taxpayer or is a trade or business of trading in financial instruments or commodities. Except as provided in subsection e 1 application to individuals.

1411 do not provide a definition of trade or business for taxpayers engaged in rental real estate activities and thus potentially subject to the tax on net investment income on income from these activities. Section 1411 is an important recent addition to the internal revenue code which will directly impact high income high net worth taxpayers. Taxpayers will be surprised by the breadth of the new.

162 which is intended to. A rule similar to the rule of section 469 e 1 b shall apply for purposes of this subsection. In the case of an individual there is hereby imposed in addition to any other tax imposed by this subtitle for each taxable year a tax equal to 3 8 percent of the lesser of a net investment income for such taxable year or b the excess if any of i the modified adjusted gross income for such taxable year over ii the threshold amount.

A trade or business of trading in financial instruments or commodities as defined in section 475 e 2. 1411 brings difficulty defining real estate trade or business. Finally gain or loss from the sale of the property used in the equipment leasing trade or business is subject to 1 1411 4 a 1 iii because the trade or business is a passive activity with respect to b as described in paragraph b 1 ii of this section.

1 1411 1 d provides that the term trade or business when used by code sec. The proposed regulations under sec. Trade or business rental real estate despite receiving multiple comments regarding the determination of a trade or business within the context of rental real estate the treasury and the irs declined to provide guidance on the meaning of trade or business solely within the context of section 1411.

1411 c 3 income on investment of working capital subject to tax a rule similar to the rule of section 469 e 1 b shall apply for purposes of this subsection. See section 1411 c 2 and regulations section 1 1411 5 a. 1411 and the final regs means a trade or business within the meaning of code sec.

Why Section 965 Transition Tax Inclusions Are Not Subject To The Sec 1411 Net Investment Income Tax Taxconnections

Pin On Business Mindset

Infographic Job Description Business Analyst Business Continuity E Trade

Ex Dividend Reminder Aflac Selective Insurance Group And Duke Realty Dividend Group Insurance Reminder

Bitcoin Growing 25 Faster Than The Internet In Its Early Years What Is Bitcoin Mining Bitcoin Mining Bitcoin Price

Planning For The Parallel Universe Of The Net Investment Income Tax

General Catalog 1911 1912 Segelke Kohlhaus Mfg Co Free Download Borrow And Streaming Victorian Interiors Victorian Homes Victorian Decor

Https Www Drakesoftware Com Sharedassets Manuals 2018 Fiduciaries Pdf

Become A Forex Trader Cryptocurrency Trading

Futuristic Technology Concept Science Drone Stock Footage Ad Concept Technology Science Futuristic In 2020 Futuristic Technology Science Technology

Forex Real Profit Ea Review Best Forex Ea S Expert Advisors Fx Robots Advisor Forex Real

Freight Management System Market Trends And Growth Factors Details For Business Development In 2020 Transportation Solutions Enterprise System Growth Marketing