Section 1250 Property Depreciation Recapture

Http Media Straffordpub Com Products Calculating Depreciation Recapture Under Irc 1245 And 1250 Minimizing Tax Through Transaction Planning 2017 08 15 Presentation Pdf

Section 1245 And 1250 Recapture Provisions Youtube

Taxation Of Business Entities Ppt Download

Recaptured And Unrecaptured Real Estate Rental Section 1250 Gain Taxcpe

Depreciation Recapture On Rental Property And Calculator Avoid The Painful Irs With A 1031 Exchange Inside The 1031 Exchange

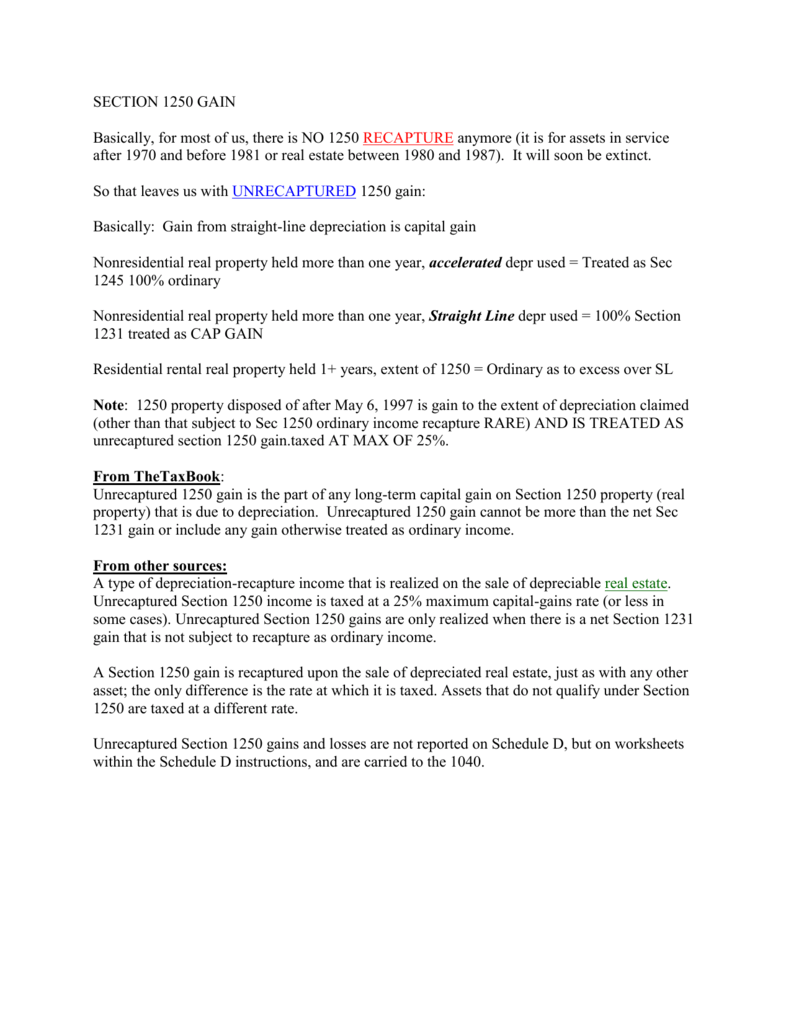

Section 1250 Gain Basically For Most Of Us There Is No 1250

Capital gains and losses from both categories are added to determine the.

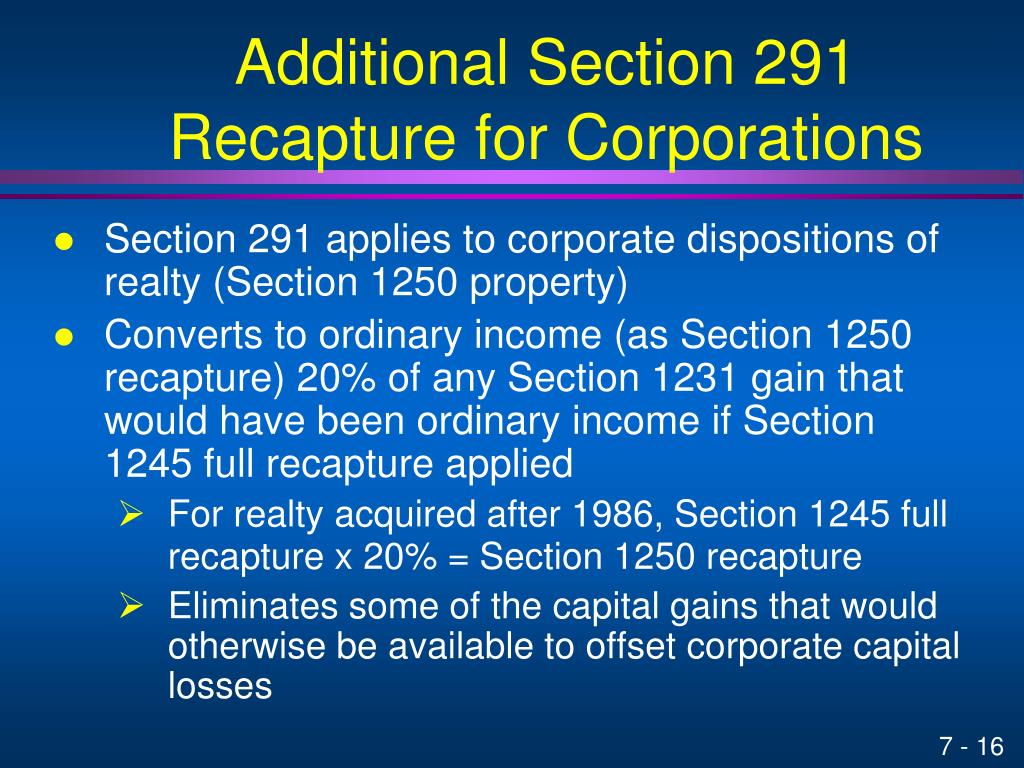

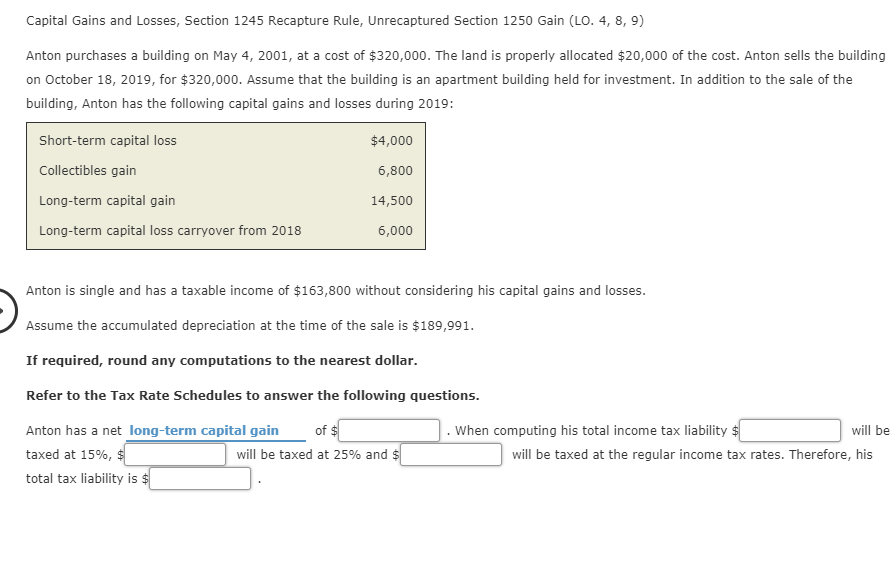

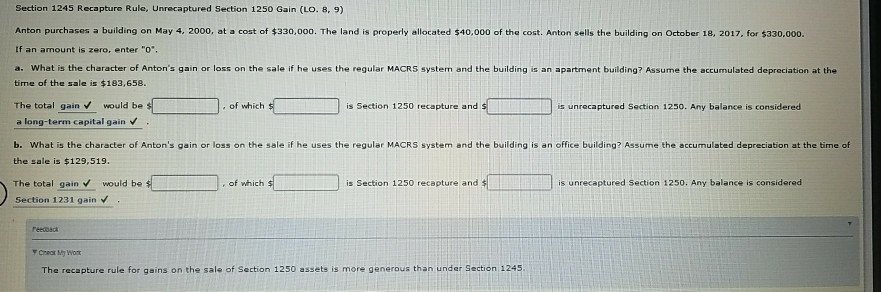

Section 1250 property depreciation recapture. A section 1231 gain is a capital gain realized from the sale of either a section 1245 property or a section 1250 property. Internal revenue code establishes that the irs will tax a gain from the sale of depreciated real property as ordinary income if the accumulated depreciation exceeds the. Part or all of the gain on the sale or other disposition of section 1250 property may be treated as ordinary income.

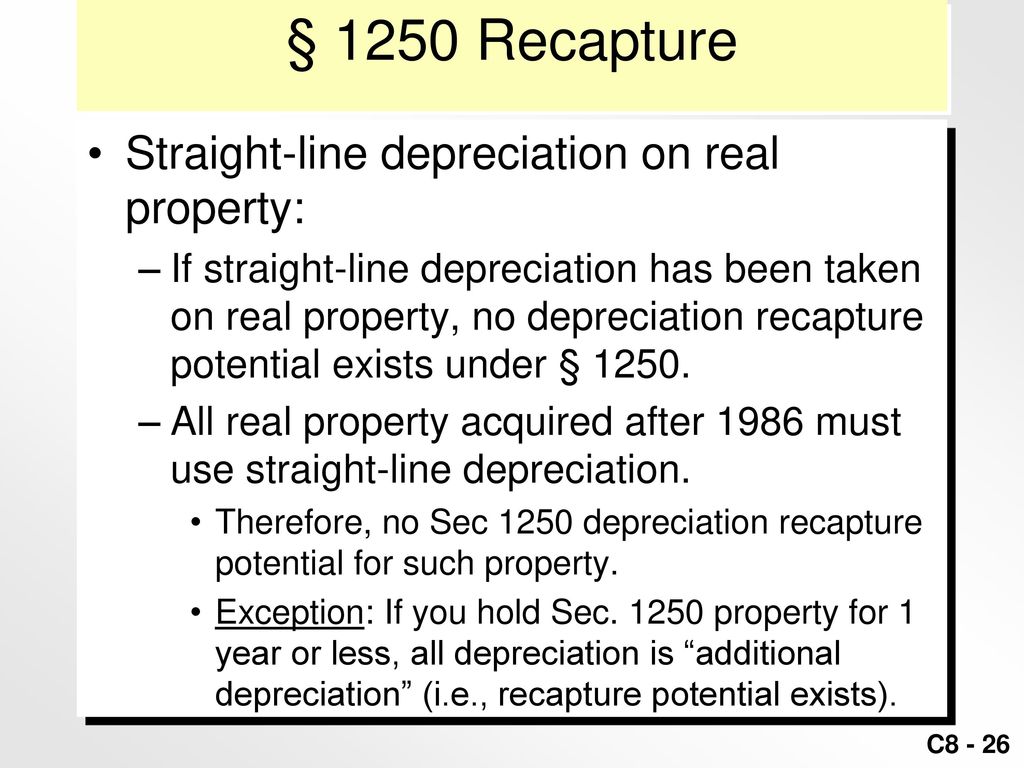

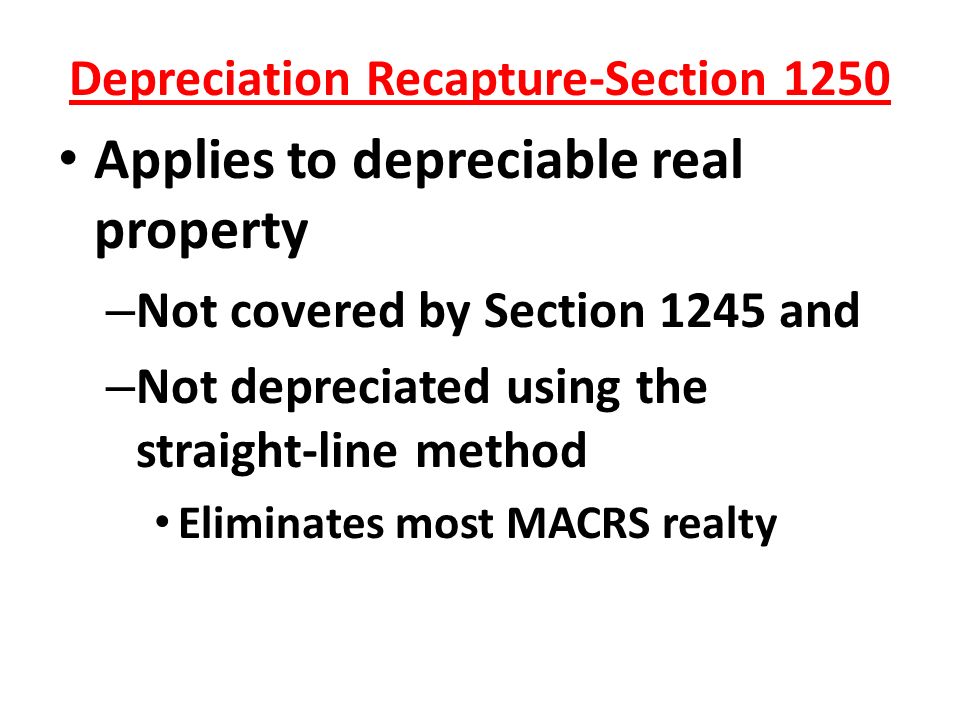

For section 1250 property held more than one year the amount of gain generally treated as ordinary income is the lower of the following. Section 1250 relates only to real property such as buildings and land.

Solved Capital Gains And Losses Section 1245 Recapture R Chegg Com

Section 1231 And Depreciation Recapture Use This I Chegg Com

Section 1250 Depreciation Recapture Corporate Income Tax Cpa Reg Ch 14 P 6 Youtube

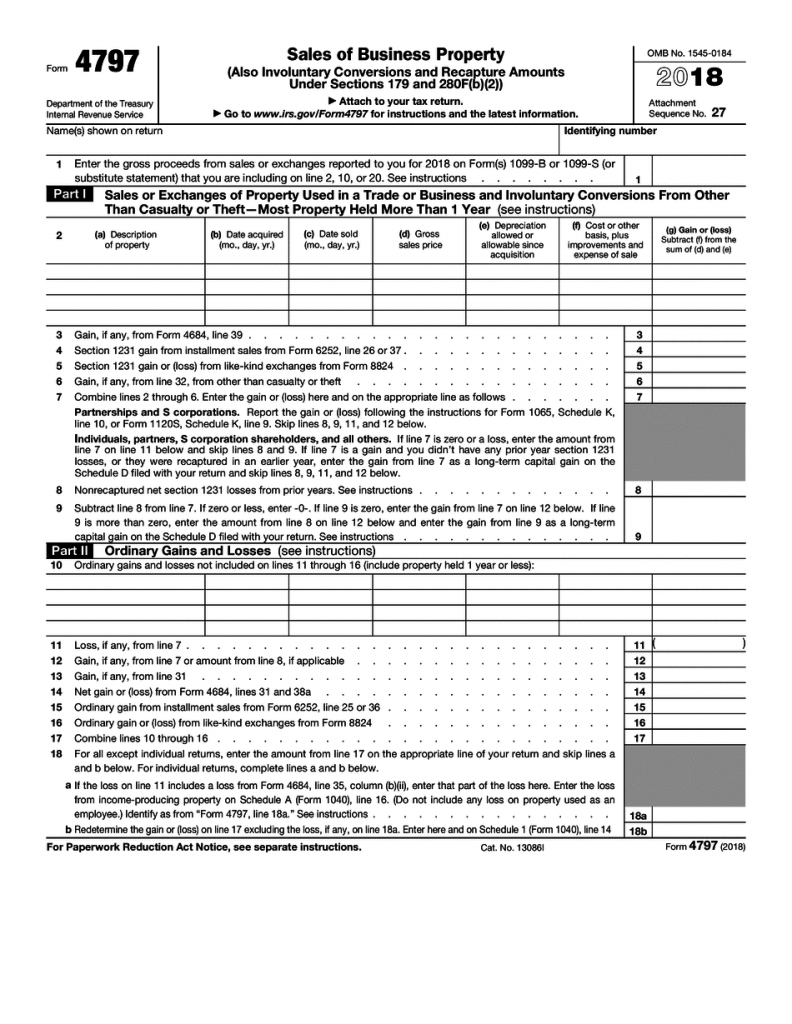

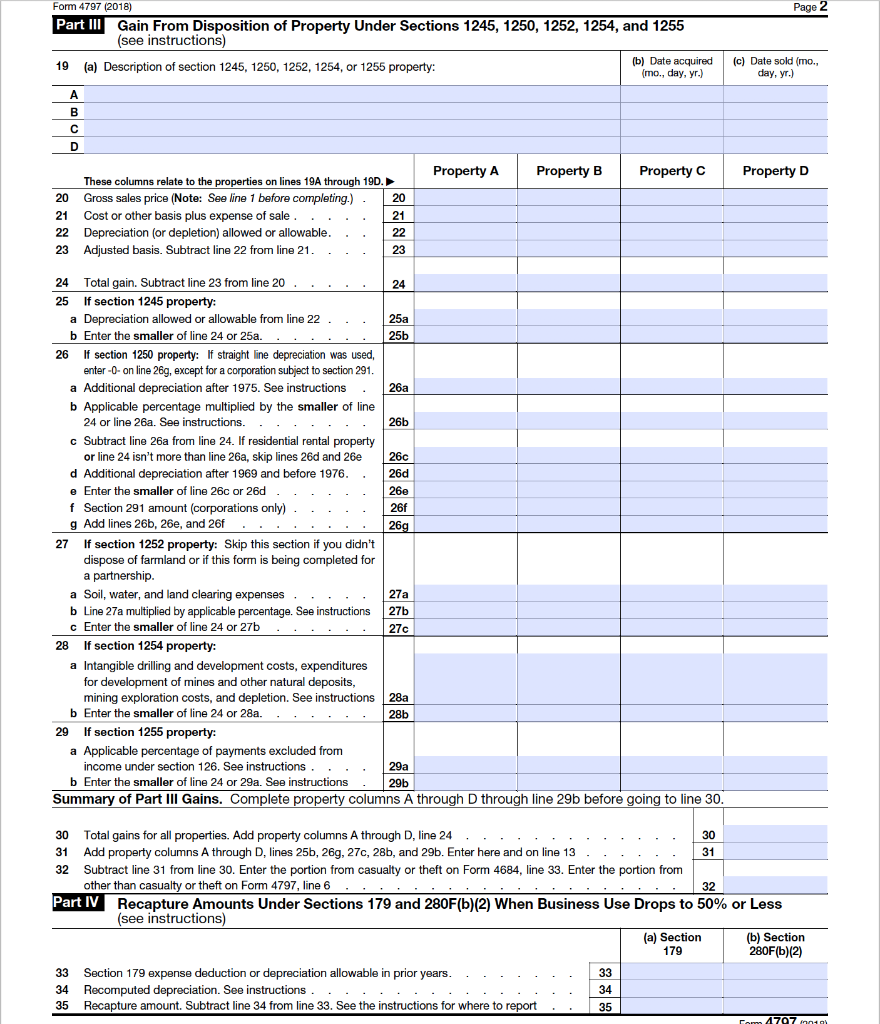

Https Farmoffice Osu Edu Sites Aglaw Files Site Library Taxpdf Ch 203 20form 204797 281 29 Pdf

Session 7 Sales Of Business Assets Ppt Video Online Download

1231 1245 And 1250 Property Used In A Trade Or Business

Chapter 11 Property Dispositions Howard Godfrey Ph D Ppt Video Online Download

Solved Exercise 17 20 Lo 1 Aqua Corporation Purchases Chegg Com

:max_bytes(150000):strip_icc()/GettyImages-1174783581-020e7504020947dc979f864f2ebee096.jpg)

Section 1250 Definition

7 1 Property Dispositions Chapter Tax Impact On Cash Flow Taxes Paid On A Recognized Gain Reduce Net Cash Flow Tax Savings Generated By A Recognized Ppt Download

Solved Section 1245 Recapture Rule Unrecaptured Section Chegg Com

Ppt Property Dispositions Powerpoint Presentation Free Download Id 5829702

Basic Tax Planning Tips For Depreciation Recapture Homeunion