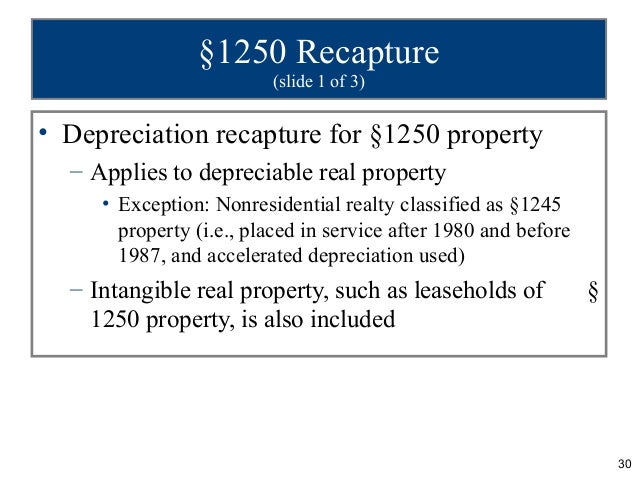

Section 1250 Assets

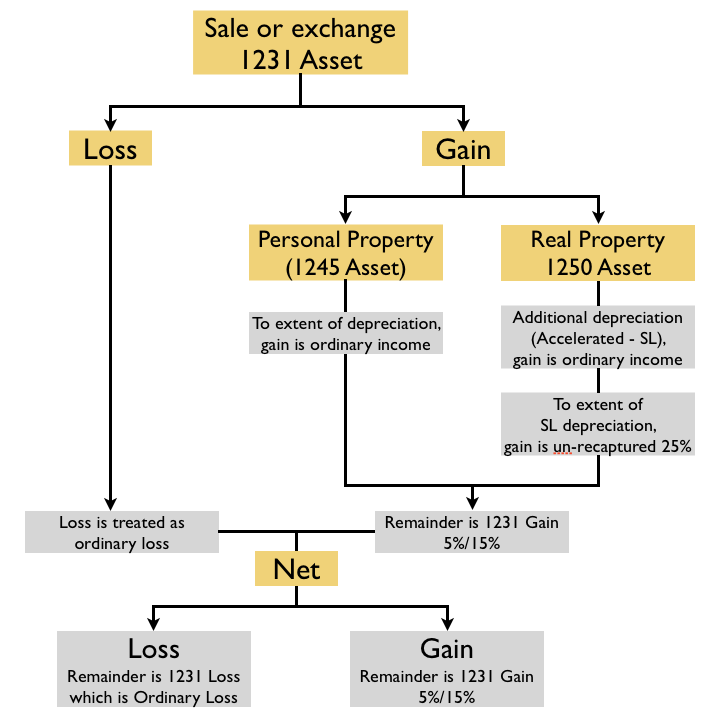

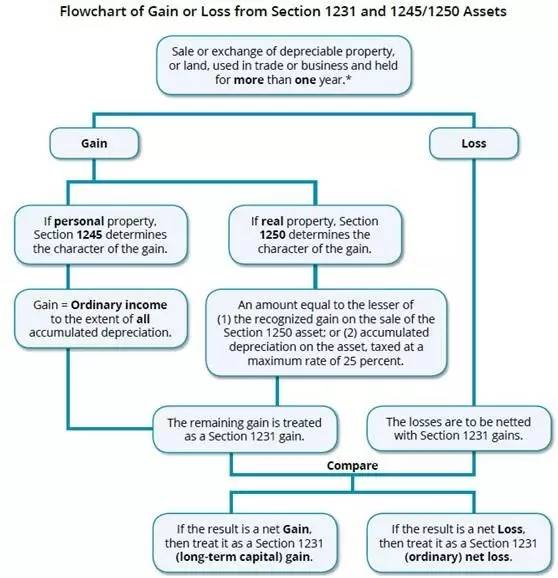

Flowchart Of Sale Or Exchange Of Property Section 1231 1245 And 1250 Assets Reg Notes Cpa Exam Club

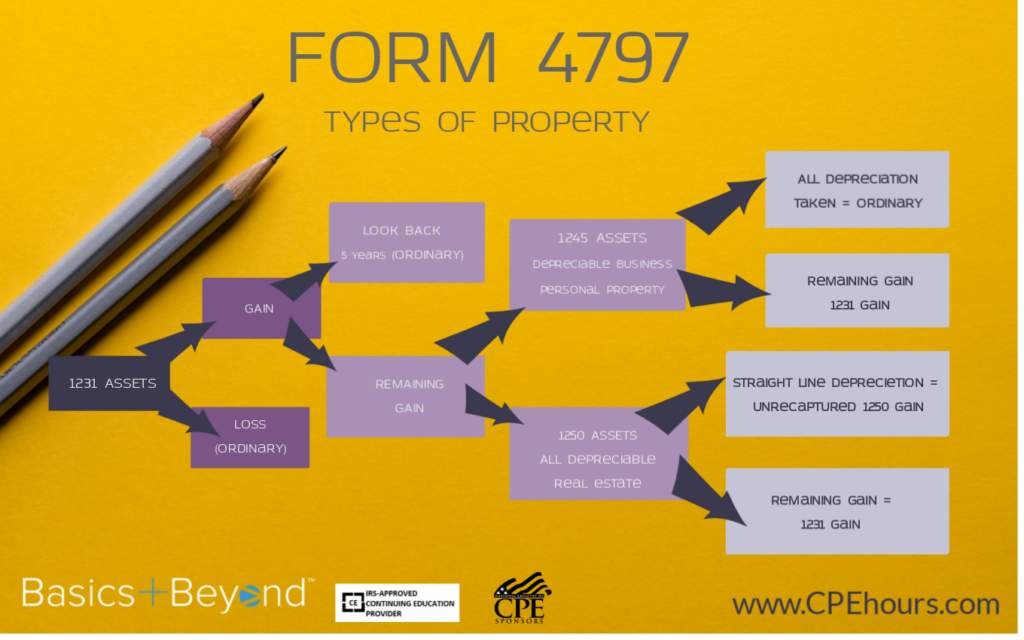

Sale Of Business Assets What You Need To Know About Form 4797 Basics Beyond

1231 1245 And 1250 Property Used In A Trade Or Business Investing Infographic Investment Quotes Investing

Http Media Straffordpub Com Products Calculating Depreciation Recapture Under Irc 1245 And 1250 Minimizing Tax Through Transaction Planning 2017 08 15 Presentation Pdf

Session 7 Sales Of Business Assets Ppt Video Online Download

Section 1231 assets include all depreciable capital assets held by a taxpayer for longer than one year.

Section 1250 assets. Depreciation allowed or allowable. Depreciation taken by other taxpayers or on other property. Figuring straight line depreciation.

Retired or demolished property. Are rental properties subject to unrecaptured section 1250 gains. It cannot be property held for personal use.

Section 1250 of the u s. If section 1250 property is held longer than one year the additional depreciation is the excess of actual depreciation over the depreciation figured using the straight line method. It must be business property or a capital asset held in connection with a trade or business or a transaction entered into for profit such as investment property.

Internal revenue code establishes that the irs will tax a gain from the sale of depreciated real property as ordinary income if the accumulated depreciation exceeds the. Learn about 1231 1245 1250 property and its treatment for gains and losses. If the property is held for one year or less all the depreciation taken is additional depreciation.

A section 1250 property is any real property that is used for business purposes. While the asset may meet the definition of section 1231 and thus be a section 1231 asset if section 1245 or section 1250 applies to an asset those provisions must be contended with as well. Section 1250 property defined.

The condemned property must have been held longer than 1 year. 3 property consisting of more than one elementin. 1 amount treated as ordinary income if in the case of a disposition of section 1250 property the property is treated.

1231 1245 And 1250 Property Used In A Trade Or Business

Recaptured And Unrecaptured Real Estate Rental Section 1250 Gain Taxcpe

Https Farmoffice Osu Edu Sites Aglaw Files Site Library Taxpdf Ch 203 20form 204797 281 29 Pdf

Ppt Ch 17

:max_bytes(150000):strip_icc()/GettyImages-1174783581-020e7504020947dc979f864f2ebee096.jpg)

Section 1250 Definition

Section 1250 Depreciation Recapture Corporate Income Tax Cpa Reg Ch 14 P 6 Youtube

Https Resources Taxschool Illinois Edu Taxbookarchive 2013 C1 20form 204797 Pdf

Depreciation Recapture On Rental Property And Calculator Avoid The Painful Irs With A 1031 Exchange Inside The 1031 Exchange

Https Www Irs Gov Pub Irs Utl 03 Alternative 20minimum 20tax 20pains Pdf

:max_bytes(150000):strip_icc()/architecture-building-urban-facade-property-professional-1364228-pxhere.com-cfab579cc3b64694913efdb2ea4d85c0.jpg)

Unrecaptured Section 1250 Gain Definition

Section 1245 Depreciation Recapture Income Tax Course Cpa Exam Regulation Tax Cuts And Jobs Act Youtube

Chapter 8

Depreciation Refresher 2017