Section 1245 Property Rental Real Estate

1231 1245 And 1250 Property Used In A Trade Or Business Investing Infographic Investment Quotes Investing

Http Media Straffordpub Com Products Calculating Depreciation Recapture Under Irc 1245 And 1250 Minimizing Tax Through Transaction Planning 2017 08 15 Presentation Pdf

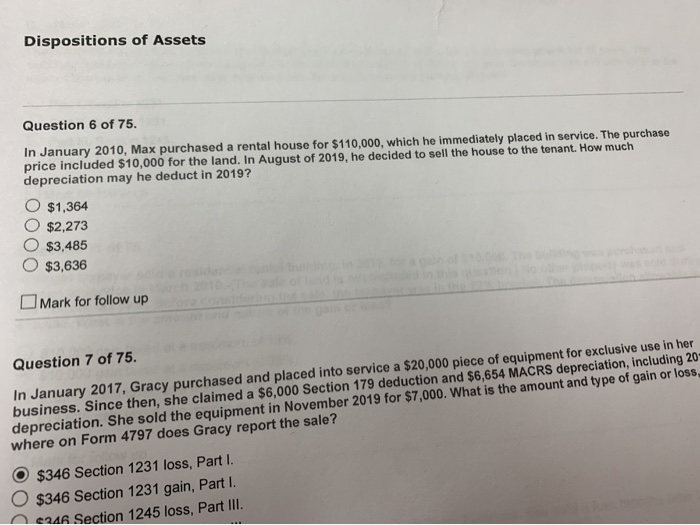

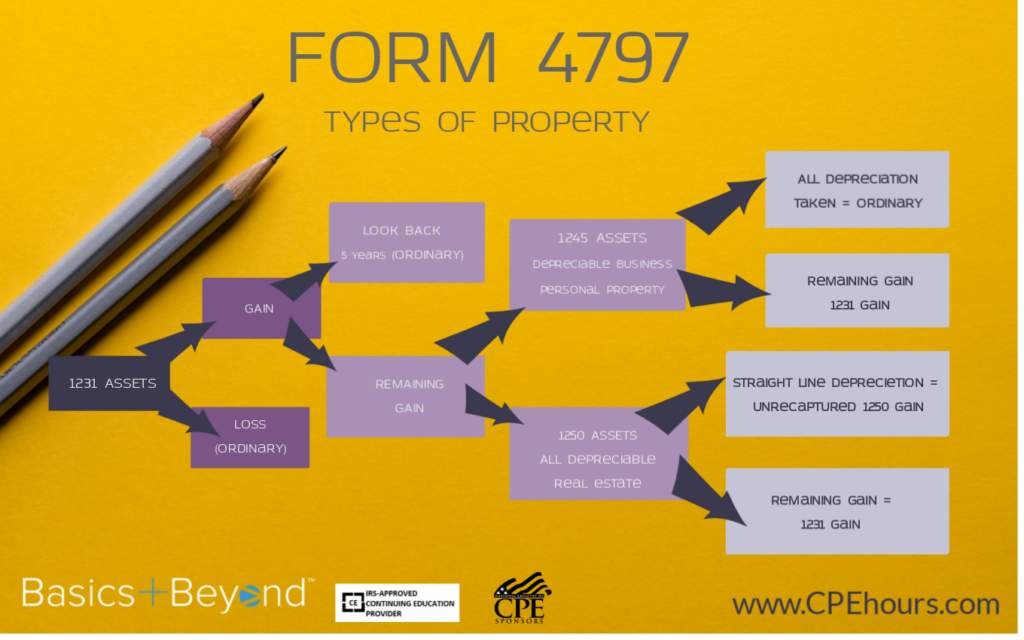

Sale Of Business Assets What You Need To Know About Form 4797 Basics Beyond

What Is Section 1245 Elb Consulting

Section 1245 Vs Section 1250 Youtube

:max_bytes(150000):strip_icc()/architecture-building-urban-facade-property-professional-1364228-pxhere.com-cfab579cc3b64694913efdb2ea4d85c0.jpg)

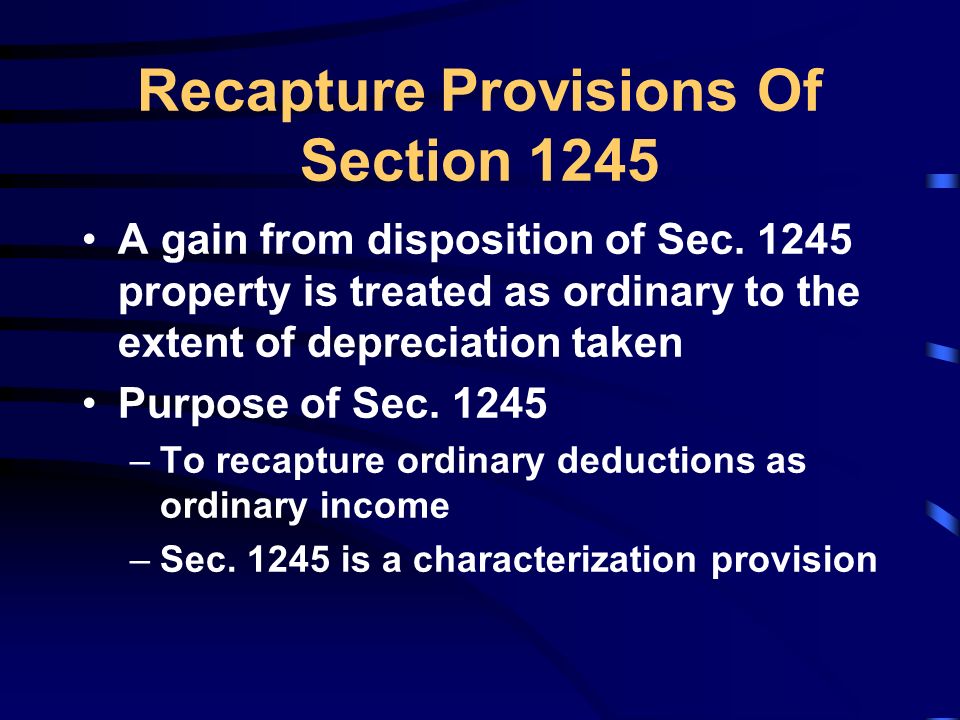

Introduction To Section 1245

1245 tangible property assets are depreciated over shorter depreciable lives mandated by the internal revenue service irs.

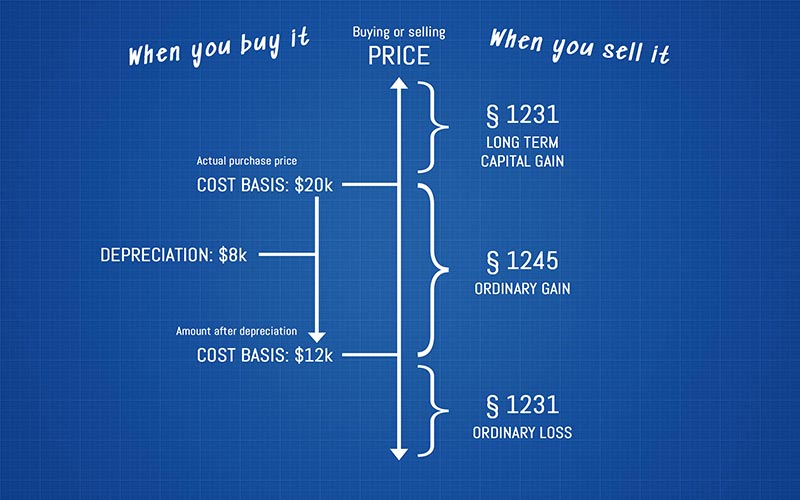

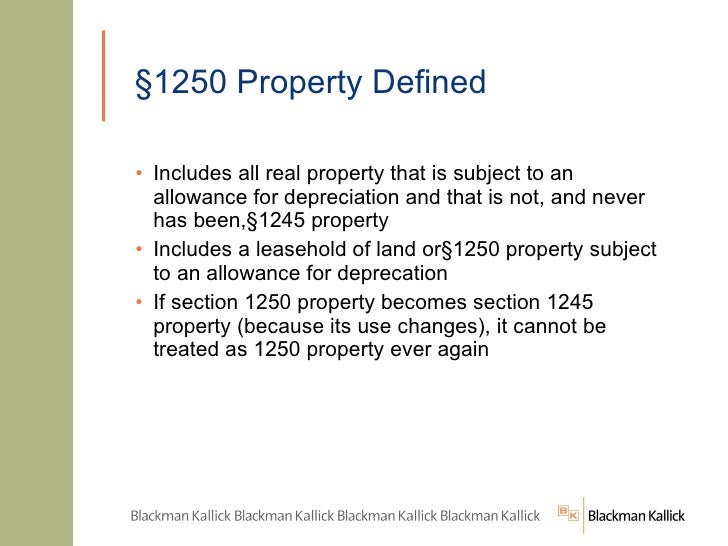

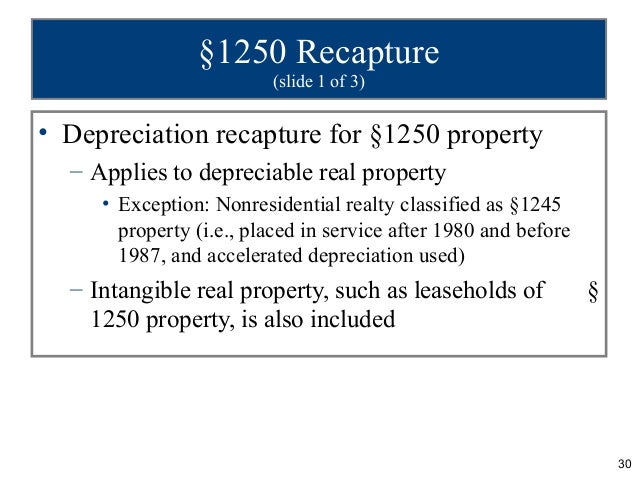

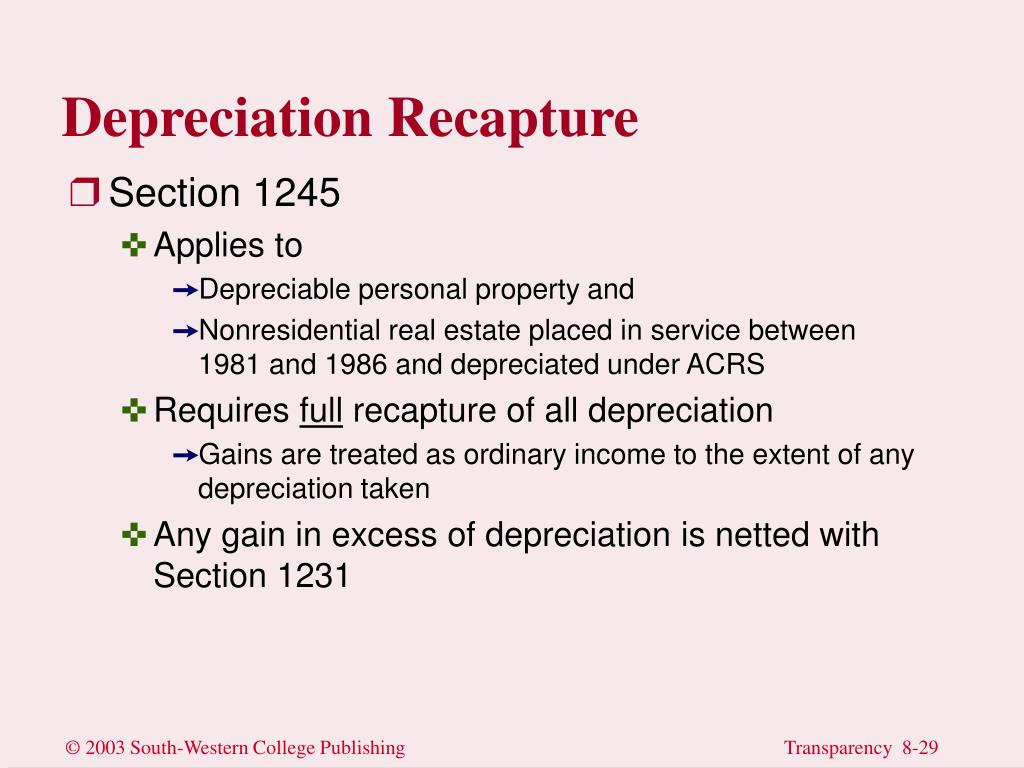

Section 1245 property rental real estate. Section 1245 property cannot include buildings or structural components unless the structure is designed specifically to handle the stresses and demands of a specific use. If you sell section 1245 property you must recapture your gain as ordinary income to the extent of your earlier depreciation deductions on the asset that was sold. Section 1250 property consists of real property that is not section 1245 property as defined above generally buildings and their structural components.

Section 1250 addresses the taxing of gains from the sale of depreciable real property such as commercial buildings warehouses barns rental properties and their structural components at an. Section 1245 property should be subject to depreciation or amortization which can be depreciated over a five seven or 15 year period. Although most real property is section 1250 property there are certain types of real property that qualify as section 1245 property.

Section 1245 property as real property the property must be depreciable or amortizable in nature. This can help reduce the business owner s tax basis by. Section 1245 property.

It can be personal or real tangible or intangible.

Navigating The Depreciation Maze

1231 1245 And 1250 Property Used In A Trade Or Business

Chapter 11 Property Dispositions Howard Godfrey Ph D Ppt Video Online Download

Https Www Calt Iastate Edu System Files Premium Video Files Powerpoint 20 20sale 20of 20business 20assets Pdf

What Is 1245 Property And How Is It Taxed Millionacres

Chapter 13 Property Transactions Section 1231 And Recapture Ppt Download

Ppt Ch 17

Section 1245 Depreciation Recapture Income Tax Course Cpa Exam Regulation Tax Cuts And Jobs Act Youtube

7 1 Property Dispositions Chapter Tax Impact On Cash Flow Taxes Paid On A Recognized Gain Reduce Net Cash Flow Tax Savings Generated By A Recognized Ppt Download

Ppt Chapter 8 Powerpoint Presentation Free Download Id 1731275

Final Review Session Ba 128a Ppt Download

Su9 2 Business Property 1245 And 1250 Flashcards Quizlet

The Power Of 1031 Like Kind Exchanges Ppt Download