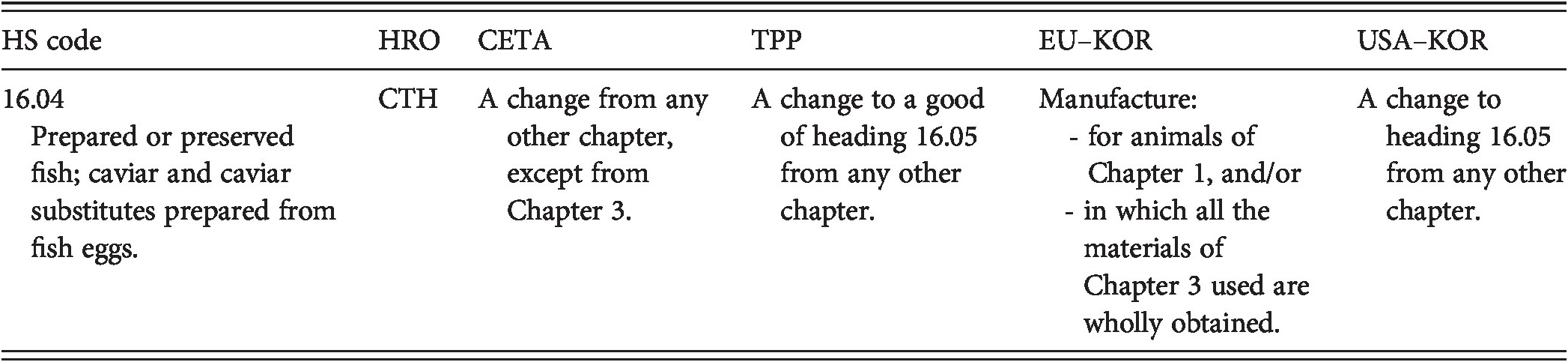

Section 1245 Property Defined

:max_bytes(150000):strip_icc()/architecture-building-urban-facade-property-professional-1364228-pxhere.com-cfab579cc3b64694913efdb2ea4d85c0.jpg)

Introduction To Section 1245

Engineering Formula Sheet Engineering Notes Engineering Mechanics Statics Engineering

Dealing With Non Tariff Measures Legal And Institutional Contexts Part Iii Behind The Border Policies

Engineering Formula Sheet Engineering Notes Engineering Mechanics Statics Engineering

Structural Engineering Spreadsheet Construction Program Spreadsheet Structural Engineering Construction Estimating Software Civil Engineering Design

Professor George Vassiliou Wellcome Mrc Cambridge Stem Cell Institute

C property described in section 1245 a 3 b.

Section 1245 property defined. Facility for bulk storage of fungible commodities. Section 1245 property defined. The internal revenue code includes multiple classifications for property.

In other words 1250 property encompasses all depreciable property that is not 1245 property. 1 tangible personal property as defined in paragraph of 1 48 1 relating to the definition of section 38 property for purposes of the investment credit and 2 intangible personal property. Section 1245 is a part of the irs code stating that depreciable property that has been sold at a price in excess of depreciated or salvage value may qualify for favorable capital gains tax treatment.

Section 1245 real property is. 87 56 may be either 1245 or 1250 property and are depreciated over a 15 year recovery period. Section 1245 property as real property.

According to the internal revenue service irs section 1245 property is defined as intangible or tangible personal property that could be or is subject to depreciation or amortization excluding. Depreciation taken on other property or taken by other taxpayers. Buildings and structural components.

The second sentence of paragraph 3 shall not apply to a disposition of section 1245 property to an organization described in section 511 a 2 or 511 b 2 if immediately after such disposition such organization uses such property in an unrelated trade or business as defined in section 513. Special rules for certain qualified section 179 real property. The term personal property means.

Section 1250 property depreciable real property including leaseholds if they are subject to. B personal property defined. Land improvements i e depreciable improvements made directly to or added to land as defined in asset class 00 3 of rev.

What Is 1245 Property And How Is It Taxed Millionacres

Taxation Of Business Entities Ppt Download

Doodle Ideas For The Currently Section Of Your Bullet Journal Make A Currently Bullet Journal Bullet Journal Writing Bullet Journal Books Bullet Journal Mood

Number Crunch Expanded Notation 4 Digit Notations

1231 1245 And 1250 Property Used In A Trade Or Business

Loom Weights In Bronze Age Central Europe Four The Textile Revolution In Bronze Age Europe

Gallery Of Sou Fujimoto Led Team Selected To Design Ecole Polytechnique Learning Centre In Paris 14 Sou Fujimoto Learning Centers Architecture Photography

Seattle Central Library Oma Lmn Seattle Central Library Seattle Library Central Library

Moshe Safdie Architects Have A Deep Social Responsibility Contemporary Architecture Design Architecture Architecture Design

Contemporary Landscape Architecture Landscape Designs For Your Home Landscape Design Modern Landscaping Landscape Architect

Youtube Project Dashboard Architecture Program Revit Architecture

432 Park Avenue Floor Plans And December Construction Update 432 Park Avenue Park Avenue Floor Plans

Mobius House Section 3 House Architecture Architecture Drawing