Irs Code Section 382

Section 382 Net Operating Loss Carryforward Rules And Regulations

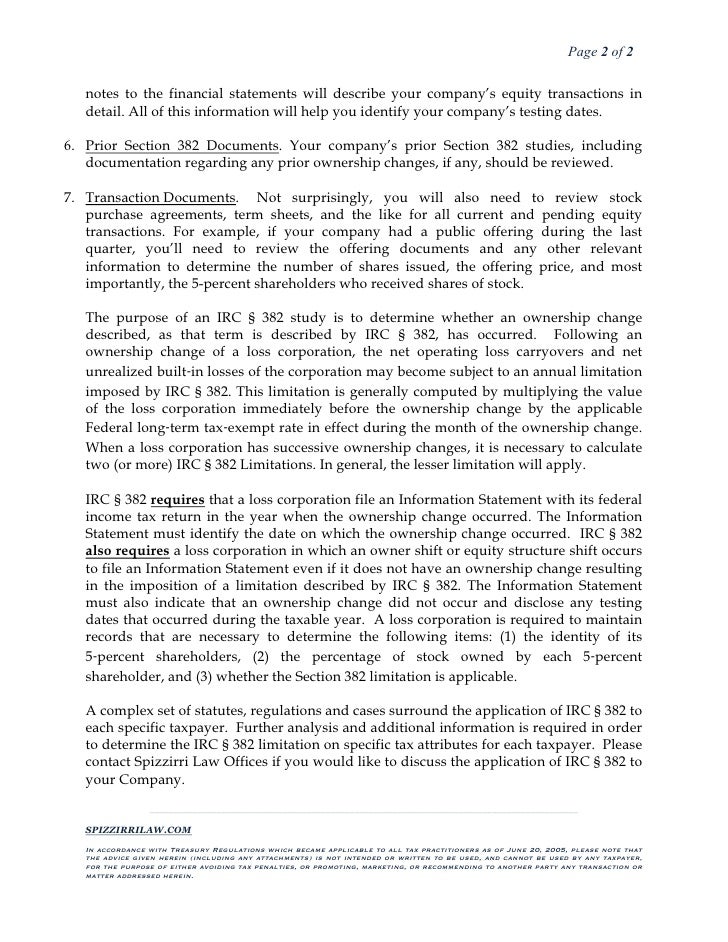

382 Studies

Https Www Alvarezandmarsal Com Sites Default Files 90507 Tax Pli Section 382 White Paper 03 Pdf

Irc 382 Section Explanation And Guide For Nol Carryforward

Internal Revenue Code 382 Accounting Rules On Operating Losses

Irc 382 Apportioned State Tax Purposes Deloitte Us Tax

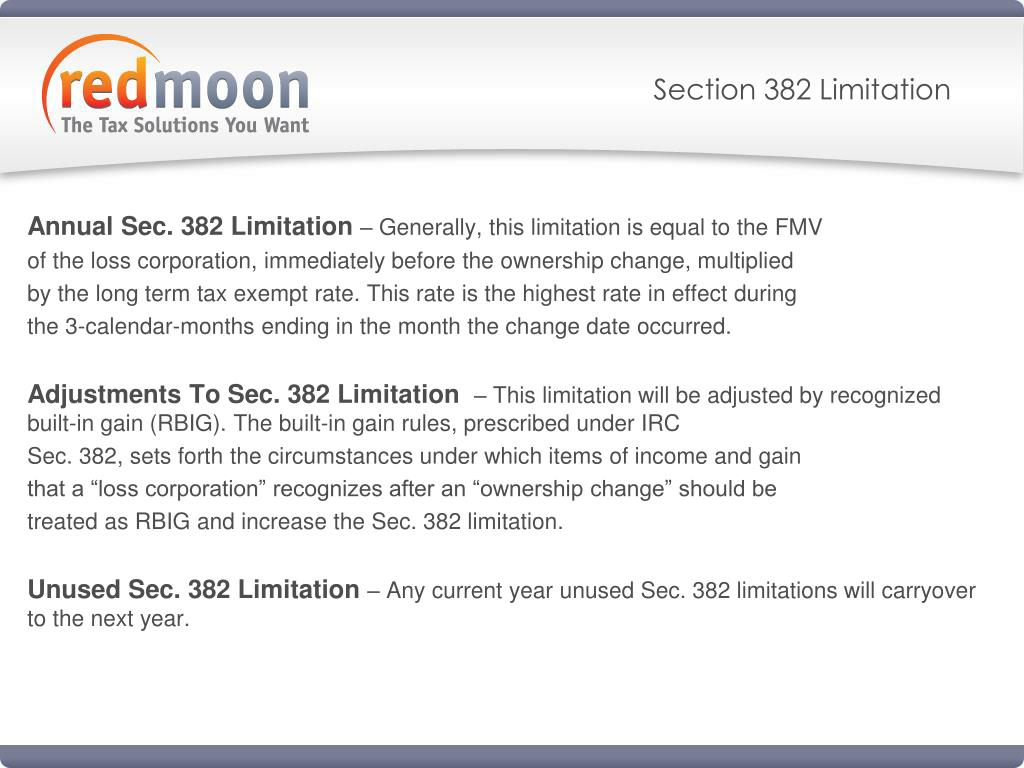

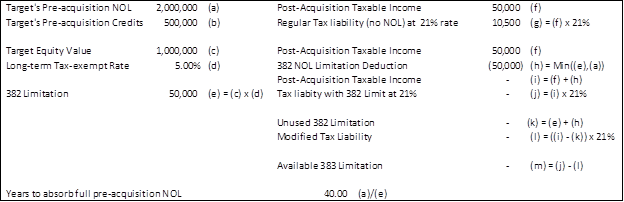

The section 382 limitation is determined by multiplying the value of the loss corporation s equity before the ownership change by a specified rate that is determined each month by treasury and the irs.

Irs code section 382. 94 455 shall not apply to any increase in percentage points occurring after december 31 1988 and. Under section 382 of the irc a c corporation is required to have a limit to offset historic losses. Although corporations are allowed to utilize pre change nols there is a limit to how much they can use to offset tax liability.

As a summary c corporations are those under us law that are taxed separately from their owners. In general the irc 382 or the internal revenue code 382 limits the ability of a corporation to use nol or net operating loss carryovers once the corporation has undergone an ownership change. I section 382 a of the internal revenue code of 1954 as in effect before the amendment made by subsection a and the amendments made by section 806 of the tax reform act of 1976 section 806 of pub.

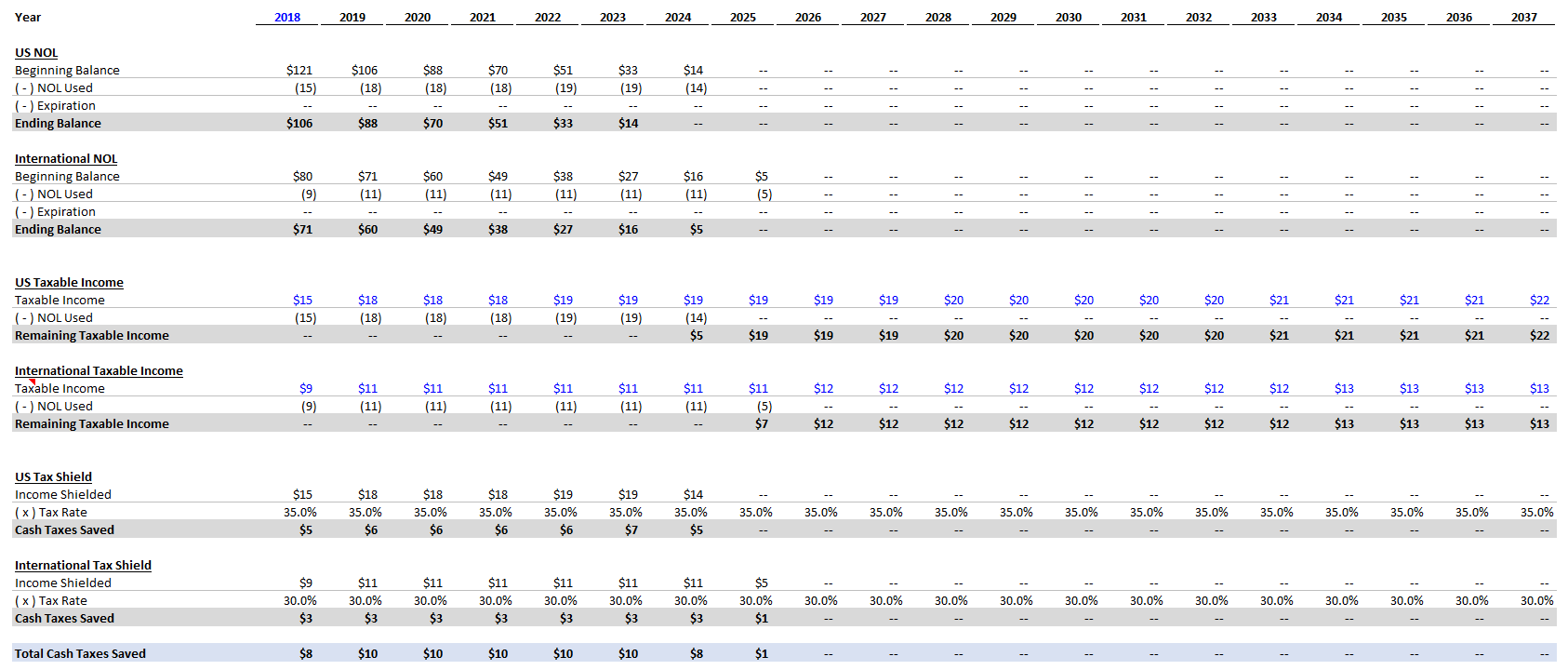

Assume an acquirer purchases all the stock of lossco for 100. Assume also that the long term tax exempt rate is 2.

Section 382 Forward Looking Statements

Tax Principles Part 2 Valuing Nols Multiple Expansion

Ppt Built In Gain Solution Sec 382 Limitation Powerpoint Presentation Id 907349

Credits And Nols Under Section 382

Nol Accounting Carryforwards Section 382 Nol Tax Savings Net Operating Loss

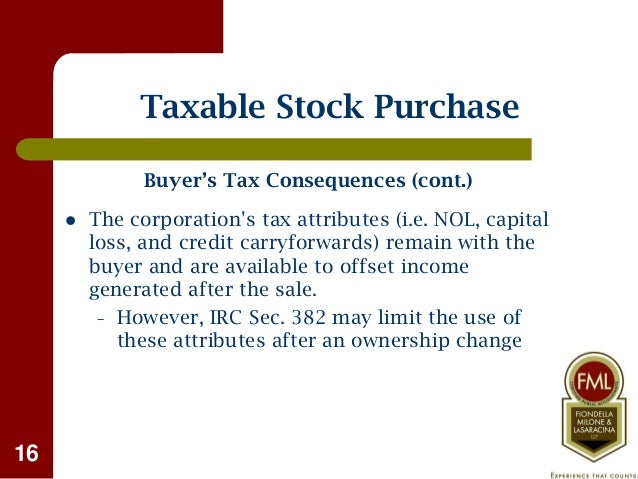

Buying Selling A Business Tax Considerations

Valuation Considerations Of Section 382 Limitations Vrc

Http Www Mtc Gov Getattachment Uniformity Uniformity Committee 2019 Agenda 8 2019 Nol White Paper August 2019 Pdf Aspx Lang En Us

Https Www Jstor Org Stable 42745397

Tax Cartoons Taxes Humor Tax Season Humor Accounting Jokes

For The Record Newsletter From Andersen Q3 2019 Newsletter Sweetening The Deal The Value Of Research Tax Credits In A Merger Or Acquisition

Section 382 And Limited Net Operating Losses

Related Parties And Nols