Irc Section 414 S

What Do Safe Harbor Adjustments Mean For Compensation Definitions Csh

B2b Ecommerce Business Resources This Or That Questions Strategies Strategic

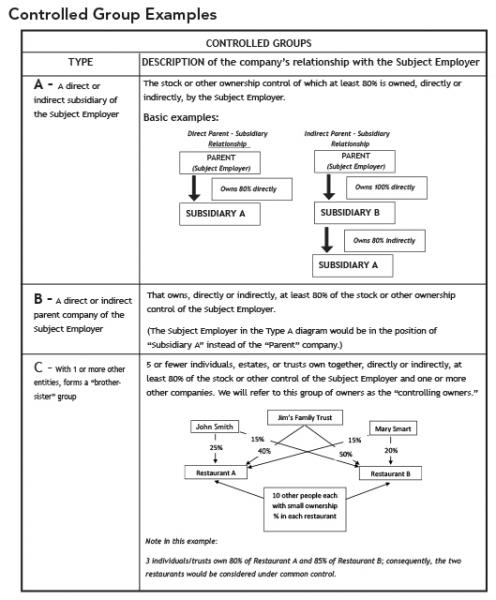

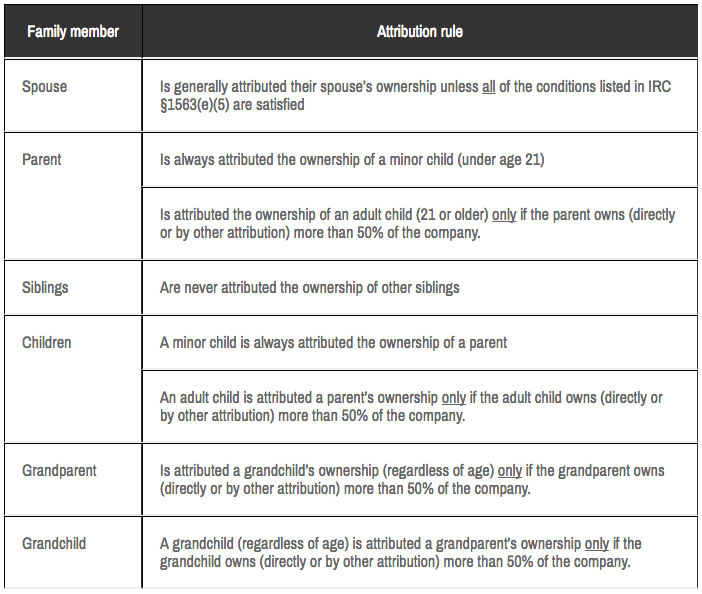

Is Your Organization Part Of A Controlled Group Common Controlled Group Basics Parker Smith Feek Business Insurance Employee Benefits Surety Northwest Beyond

Definitions Of Compensation For Plan Purposes Retirement Learning Center

Buy Cash Registers Sydney Pos Systems At Best Rate In Australia Cash Register Thermal Printer Label Printer

Is Your Company Part Of A Controlled Group You Need To Know Or Risk 401 K Plan Disqualification

2 employer may elect not to treat certain deferrals as compensation.

Irc section 414 s. Except as otherwise provided in paragraph j 2 ii of this section 1 414 s 1 through apply to years beginning on or after january 1 1994. This snapshot discusses how to identify hces in a plan s initial plan year or in a short plan year. Private letter rulings irc section 414.

Section 414 s applies to years beginning on or after january 1 1987. 414 e 1 in general. For purposes of subparagraph a all plans maintained by employers who are treated as a single employer under subsection b or o of section 414 shall be treated as 1 plan except that a plan described in clause i of section 410 b 6 c shall not be treated as a plan of the employer until the expiration of the transition period with respect to such plan as determined under clause ii of such section.

A definition of compensation within the meaning of irc section 415 c with certain permissible modifications also satisfies irc section 414 s. 2 regulatory effective date i in general. Some definitions of compensation automatically satisfy irc section 414 s.

For example a definition of compensation that includes all compensation within the meaning of irc section 415 c 3 and excludes all other compensation automatically satisfies irc section 414 s. For purposes of this part the term church plan means a plan established and maintained to the extent required in paragraph 2 b for its employees or their beneficiaries by a church or by a convention or association of churches which is exempt from tax under section 501. The definition of an hce is set forth in irc section 414 q.

Irc section 414 plr. Except as provided in this subsection the term compensation has the meaning given such term by section 415 c 3. Ii plans of tax exempt organizations.

Whether contributions made by employer a to plan x on behalf of its peace officers who are licensed by the board are considered contributions by an agency or instrumentality of state m or political subdivision thereof for purposes of code section 414 d and participation in plan x by such peace officers of employer a will not adversely affect the status of plan x as a governmental plan within the meaning. Internal revenue code section 414 s definitions and special rules. Code section 414 s and associated regulations provide a definition of compensation that must be used by qualified plans and 403 b plans that feature employer contributions in certain discrimination tests.

Infographic How Many Languages Are Spoken In The Us Redline Foreign Language Learning Language Learning Languages

Plan 710025btz Classic Cottage With Cedar Shake Shingles Cedar Shake Shingles House Floor Plans Shake Shingle

Defining Compensation For 401 K Plan Contributions And Testing Ascensus

Inmate Reception Center Irc Holding Cells Bail Jail County Jail

Irs Announces Adjustments To Retirement Plan Contributions And Benefits Limits For 2020

Compensation Ratio Test Nondiscrimination Testing Dwc

Https Www Bakermckenzie Com Media Files Insight Publications 2018 09 Al Understandingdefinitioncompensation Sep2018 Pdf La En

Pin By Irc Ashland University Library On Irc Materials Kits

Part I New Comparability Plan William Dicristofaro

Checklist Of Federal Tax Law Rules Applicable To Public Retirement Systems Employee Benefits Legal Resource Site

Keep Gutters Separate From Footing Drains Foundation Drainage Drainage Solutions Drainage

Dissecting The New Business Interest Expense Limitation Blue Co Llc

5 Lesser Known Retirement And Benefit Plans