Irc Section 338 H 10

(10).JPG?cbcachex=262393)

Gt S Quick Guide To Section 338 H 10 Elections Insights Greenberg Traurig Llp

Cft 2004 02 Corporate Franchise Tax Information Release The Franchise Tax Effects Of The Irc Section 338 H 10 Election Issued June 2004

Buying Selling A Business Tax Considerations

Section 338 Election Overview Asset Sale Tax Implications

Section 338 H 10 S Corporation Checklist Rev 9 05 Pdf Free Download

Https Www Ftb Ca Gov Tax Pros Procedures S Corp Handbook S Corp Chapter 16 Pdf

A 338 h 10 election allows a buyer of stock of an s.

Irc section 338 h 10. H definitions and special rules. One on the shareholders upon their sale of the target stock and the other on the deemed asset sale by the target corporation old target. Section 338 h 10 of the internal revenue code can provide significant tax benefits to a buyer of 80 or more of a target corporation.

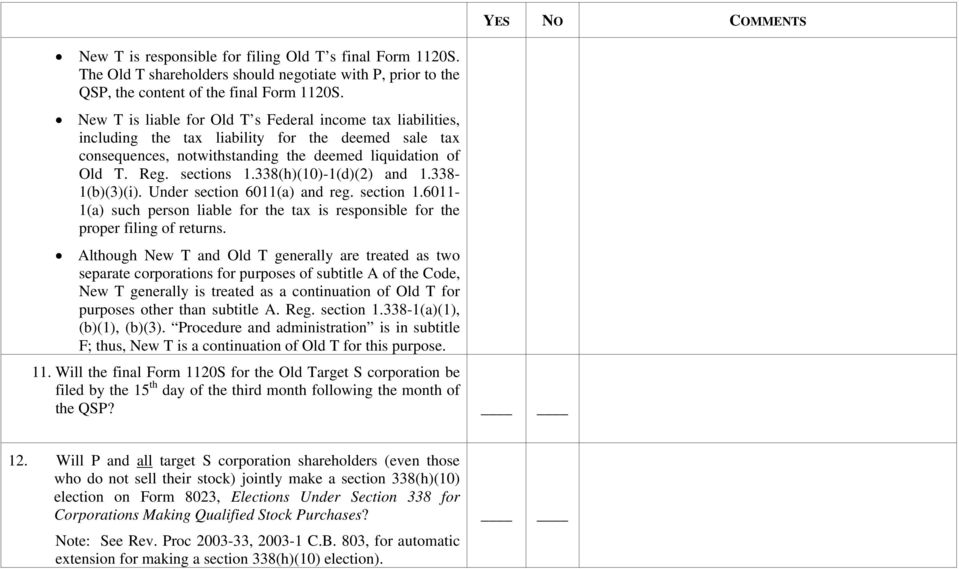

S corporation shareholders who do not sell their stock must also consent to the election. In a regular section 338 election two levels of tax are imposed. When a corporate buyer buyer purchases the stock of a target corporation target from a selling consolidated group sec.

The deemed asset sale for tax purposes increases the tax basis of the target s assets which can significantly reduce the buyer s future taxable income. In simple terms a 338 h 10 is a tax election for a qualified stock purchase qsp which recharacterizes a stock purchase as an asset purchase for federal tax purposes. A 338 h 10 election allows a buyer of stock of an s corporation or a corporation within a consolidated group to treat the transaction as an acquisition of 100 of the assets of the target for tax purposes.

In addition there is typically only a single level of tax in the transaction. A section 338 h 10 election is made jointly by p and the selling consolidated group or the selling affiliate or the s corporation shareholders on form 8023 in accordance with the instructions to the form. An irc section 338 h 10 election is available when one corporation is purchasing the stock of either an s corporation or a c corporation that is a member of an affiliated group of corporations.

Section 338 h 10 a section 338 h 10 election is much more common than a section 338 g election because the 338 g election results in two levels of tax whereas a 338 h 10 election results in only one. It remains a stock purchase for all other legal purposes such as contracts and licensing more on that later. 338 h 10 offers the opportunity for the buyer to obtain a step up in basis for the assets owned by target.

A section 338 h 10 election is jointly made by the purchasing corporation and the common parent of the selling consolidated group or the selling affiliate or s corporation shareholder s. The amendment made by subparagraph a amending this section shall apply to qualified stock purchases as defined in section 338 d 3 of the 1986 code after march 31 1988 except that in the case of an election under section 338 h 10 of the 1986 code such amendment shall apply to qualified stock purchases as so defined after june 10 1987. Section 338 h 10 of the internal revenue code can provide significant tax benefits to a buyer of 80 or more of a target corporation.

Understanding The Section 338 H 10 Election Youtube

Tax Issues In Private Equity Venture Capital

Mergers Acquisitions Federal And State Ppt Download

Irc Section 338 H 10 May 8 2019

State Tax Matters

Acquisitions Of Subsidiaries Of Freestanding Companies Ppt Download

338h10 Elections V10 31 16

Valuation Plays Key Role In Section 338 Elections Valuation Research

New York State Tax Gain From Irc 338 H 10 Deloitte Us Tax

M A Tax For 2019

Tax Issues In Private Equity Venture Capital Aba Section Of Business Law August 12 2007 Julie Divola Jonathan Axelrad Pillsbury Winthrop Shaw Pittman Ppt Download

Https Www Revenue Pa Gov Generaltaxinformation Taxlawpoliciesbulletinsnotices Letterrulings Crp Documents Crp 14 001 Pdf

Tax Issues To Consider In Common Acquisition Scenarios Ppt Download