Irc Section 274 A 4

Current Mode Test Schematic My Fb Current Test

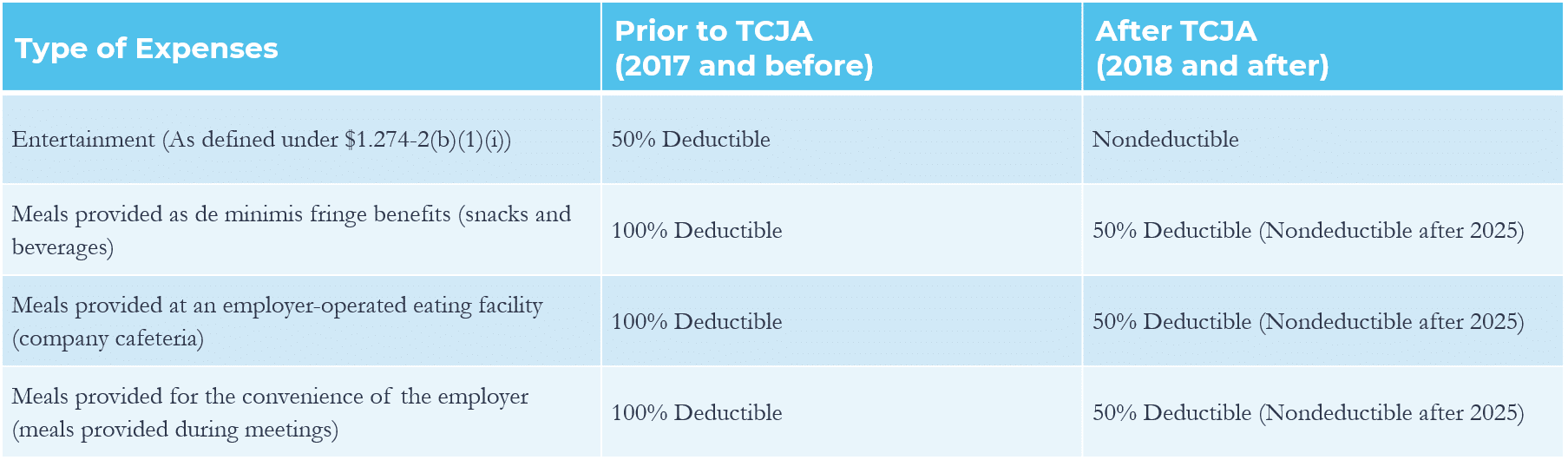

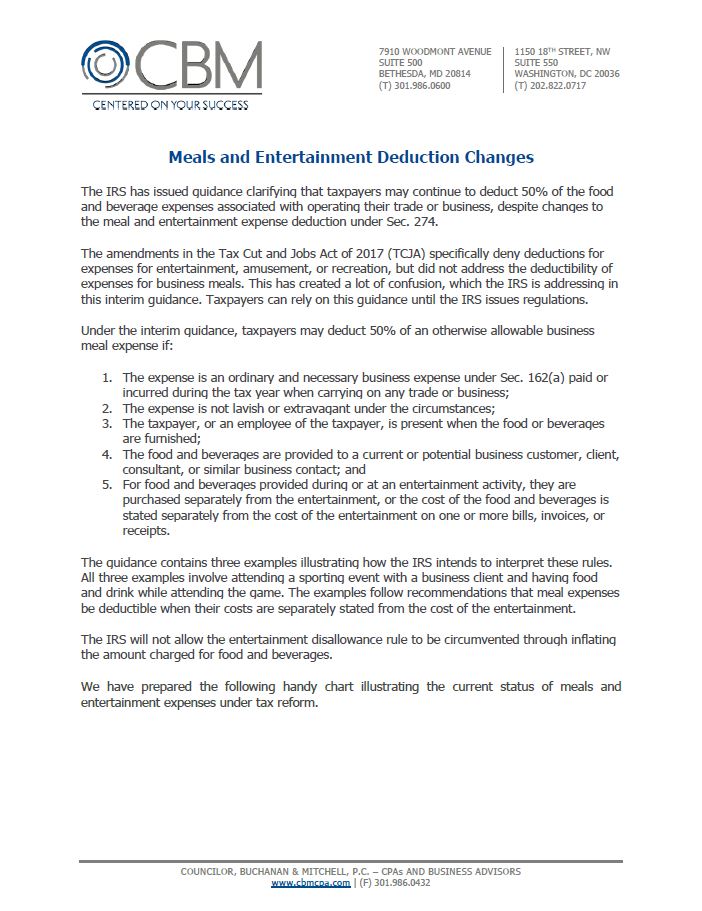

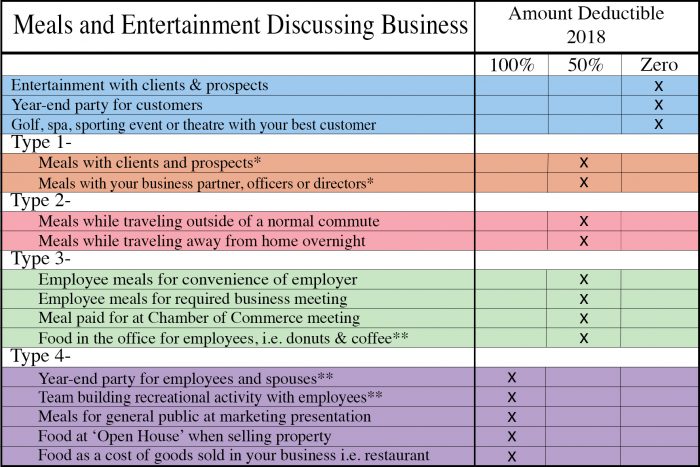

Navigating The New Meals And Entertainment Deductions Under Tcja Grf Cpas Advisors

Article 274 European Banking Authority

Tropical Climate House Plan With Raised Light Weight Construction And Skillion Roofs Tropical House Design Australian House Plans House Design

Disallowed Deductions For Qualified Parking Strategic Finance

Pin On Maps Schedules

In such case the amount of the expenses directly connected with the unrelated trade or business is subject to the disallowance under section 274 a 4 and thus is disallowed as a deduction in calculating the ubti attributable to such unrelated trade or business under the general rule of section 512 a 1.

Irc section 274 a 4. Section 274 was added to the code by section 4 of the revenue act of 1962 public law 87 834 76 stat. This document contains proposed regulations under section 274 of the code that amend the income tax regulations 26 cfr part 1. The irs has issued guidance detailing the deduction disallowance provisions of section 274 a 4 explaining how to determine the nondeductible portion of employee parking expenses.

With some exceptions an employee who adequately accounts for the m ie is not again required to substantiate the expenses. No deduction is allowed under the code as spelled out in section 274 a 4 for the expense of any qualified transportation fringes qtf provided by employers for the purposes of this article the employers are nonprofit organizations to their employees. Sections 274 and 512 were amended by the tax cuts and jobs act pub.

274 a 4 of the internal revenue code code and for tax exempt organizations to determine the corresponding increase in the amount of unrelated business taxable income ubti under 512 a 7 attributable to the nondeductible parking expenses. Section 1 274 5t f 5 of the temporary income tax regulations. Details of the internal revenue code sections 274 a 4 and 512 a 7 the message is clear.

274 d 4 for expenses with respect to any listed property as defined in sec. If the payor and employee use the annually. 1 limitation no deduction shall be allowed under section 162 or section 212 for any expense for gifts made directly or indirectly to any individual to the extent that such expense when added to prior expenses of the taxpayer for gifts made to such individual during the same taxable year exceeds 25.

1954 relating to disallowance of certain entertainment etc expenses shall not apply to expenses paid or incurred by the taxpayer for goods services and facilities to the extent that the expenses are includible in the gross income of a recipient of the entertainment amusement or recreation who is not an employee of the taxpayer as compensation for services rendered or as a prize or award under. Subsection a of section 274 of the internal revenue code of 1986 formerly i r c. 1954 relating to disallowance of certain entertainment etc expenses shall not apply to expenses paid or incurred by the taxpayer for goods services and facilities to the extent that the expenses are includible in the gross income of a recipient of the entertainment amusement or recreation who is not an employee of the taxpayer as compensation for services rendered or as a prize or award under.

960 and has been amended numerous times over the years. For purposes of this section the term gift means any item excludable from gross. Subsection a of section 274 of the internal revenue code of 1986 formerly i r c.

Jazz Real Book Ii Page 274 Once In A While Michael Edwards Jazz Standard Sheet Music Sheet Music Jazz Standard Music Notes

Tax Update On Meals And Entertainment Deduction Charges Councilor Buchanan Mitchell Cbm

Tax Planning Meals Entertainment Traderstatus Com

Farrow Ball Color Ammonite No 274 Living Room Bookcase Hall Colour Hallway Decorating

Pantone 274 C Pantone Color Pms Hex En 2020 Paletas De Colores Paleta De Color Pantone Colores Pantone

Pin On My Homosexual Heart

Revox C 274 Bandrecorder Bandrecorders Audio

The Yoga Freedom Project Helped Raise Funds For The Support Of Aftercare For Trafficking Victims In Both Nyc And Cambodia Yoga Center Dharma Yoga Projects

Proposed Regulations Regarding Tcja Disallowance For Employee Commuting And Parking Costs A Mixed Bag Tax Withholding Reporting Blog

Https Www Afwa Org Wp Content Uploads 2019 10 Afwa19 Tax Reform Kuntz Pdf

Steinway D 274 Wikipedia The Free Encyclopedia Piano Steinway Piano Steinway

Template Geometric Planter Terrarium Project 0274 Printable Etsy Geometric Planter Terrarium Geometric

Irc Volume Control Kit Vintage Industrial Metal Parts Cabinet Industrial Crafting Storage Jewelry Art Supplies Storage Craft Storage Jewellery Storage