Irc Section 212 Deductions

Alizio Law Pllc Long Island Tax Attorneys Tax Attorney Tax Lawyer Attorneys

Tax Deductions For Financial Advisor Fees Without Irc 212 Wtop

Intent To Rent

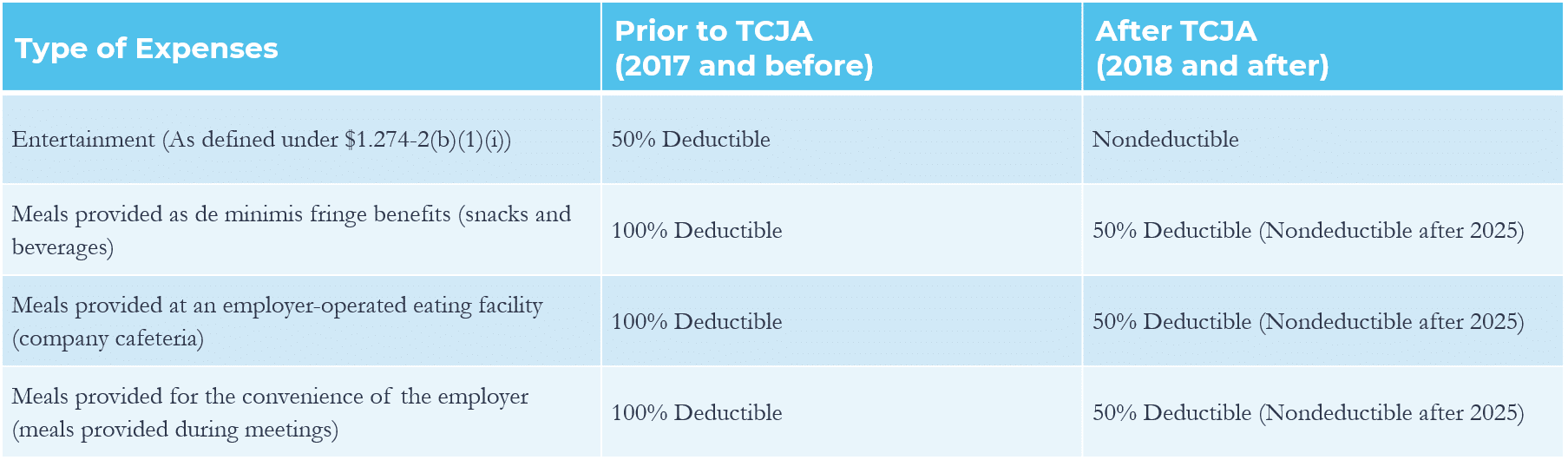

Navigating The New Meals And Entertainment Deductions Under Tcja Grf Cpas Advisors

Get Unfiled Tax Return Help On Long Island There Is A Statute Of Limitations On Obtaining Income Tax Refunds If You Are Due Tax Return Tax Attorney

Https Www Dtcc Com Media Files Pdf 2020 6 26 13429 20 Pdf

Operating as an individual in self employment eliminates the ability to take advantage itemized deductions.

Irc section 212 deductions. Federal income tax purposes for expenses incurred in investment activities. For the production or collection of income. The deduction of an item otherwise allowable under section 212 will not be disallowed simply because the taxpayer was entitled under subtitle a of the code to treat such item as a capital expenditure rather than to deduct it as an expense.

212 2. In connection with the determination collection or refund of any tax. Internet bills phone bills power bills gas and mileage.

There shall be allowed as a deduction all the ordinary and necessary expenses paid or incurred during the taxable year. For the production or collection of income. Expenses for production of income.

Section 212 of the tax code has been suspended from january 1 2018 to at least 2025. 212 provides a deduction for u s. What that covers are your itemized deductions.

For the management conservation or maintenance of property held for the production of income. In the case of an individual there shall be allowed as a deduction all the ordinary and necessary expenses paid or incurred during the taxable year. Costs that are not deductible under this section are those that customarily would be incurred by a hypothetical individual holding the same property such as ownership costs e g homeowners association fees insurance and maintenance.

There shall be allowed as a deduction the expenses paid during the taxable year not compensated for by insurance or otherwise for medical careof the taxpayer his spouse or a dependent as defined in section 152 determined without regard to subsections b 1 b 2 and d 1 b thereof to the extent that such expenses exceed 10 percent of adjusted gross income. Section 212 deductibility eliminated but some benefits remain before tcja internal revenue code section 212 allowed individuals to deduct expenses incurred in the production of income including. Taxpayers are allowed to deduct all the ordinary and necessary expenses paid or incurred during the taxable year 1 for the production or collection of income.

Contact Information Peter Alizio Tax Attorney Tax Attorney Tax Lawyer Income Tax Preparation

Alizio Law Pllc Tax Attorney 1551 Franklin Avenue 205 Mineola Ny 11501 212 520 2906 Tax Help Tax Attorney Tax Lawyer

Deductions For Vs From Agi Coursera

Group Exemption Northern California Spinal Cord Network

Tax Deductions For Individuals A Summary Everycrsreport Com

Logo Nassau County Bar Association Tax Attorney Tax Lawyer Tax Help

Are Estate Planning Legal Fees Tax Deductible Dallas Elder Lawyer

Gale Academic Onefile Document Individual Income Tax Rates And Tax Shares 1998

Nyc 8 General Corporation Tax Claim For Credit Or Refund

Sec Filing Liberty Broadband Corporation

Https Www Justice Gov Archive Tax Sperl D3motforpreliminjmemo Pdf

Tax Issues In Litigation Treatment Of Judgment And Settlement Payments And Deductibility Of Legal Expenses Everycrsreport Com

Real Estate Taxes Are Subject To A 10 000 Limit Or Are They Sol Schwartz