Internal Revenue Code Section 267

Section 267 B 1 Related Family Members

Part Iii Passport Revocation Department Of State Says Its Hands Are Tied Go Resolve With The Taxman Irs Tax Expatriation

Attribution Rules

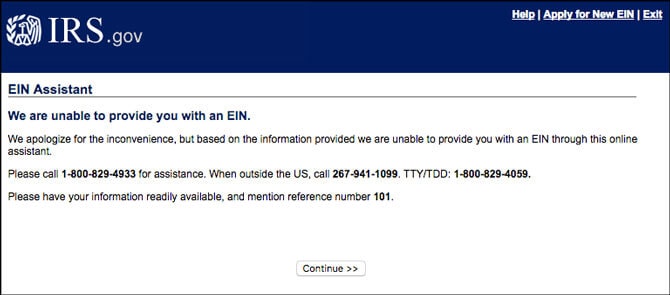

Ein Reference Number 101 109 110 115 What Do They Mean Llc University

Sec 163 Interest

Irs Reference Codes On Where S My Refund Refundtalk Com

Title 26 internal revenue code subtitle a income taxes chapter 1 normal taxes and surtaxes subchapter b computation of taxable income.

Internal revenue code section 267. Rules for treating a tax preference as an exclusion from income for purposes of applying subsection b 1 if such tax preference has the effect of reducing the generally applicable statutory rate by 25 percent or more i r c. The amendments made by subsections a and b 1 amending this section shall apply to amounts allowable as deductions under chapter 1 of the internal revenue code of 1986 formerly i r c. 1954 for taxable years beginning after december 31 1983.

Internal revenue code 267. Section 267 losses expenses and interest with respect to transactions between related taxpayers 26 u s c. For more detailed codes research information including annotations and citations please visit westlaw.

267 casetext search citator. 1 deduction for losses disallowed. Losses expenses and interest with respect to transactions between related taxpayerstext contains those laws in effect on september 27 2020.

For purposes of the preceding sentence the allowability of a deduction shall be determined without regard to any disallowance or postponement of deductions under section 267 of such code. Internal revenue code section 267 b losses expenses and interest with respect to transactions between related taxpayers a in general. Losses expenses and interest with respect to transactions between related taxpayers on westlaw findlaw codes are provided courtesy of thomson reuters westlaw the industry leading online legal research system.

From title 26 internal revenue codesubtitle a income taxeschapter 1 normal taxes and surtaxessubchapter b computation of taxable incomepart ix items not deductible. Section 267 losses expenses and interest with respect to transactions between related taxpayers a in general 1 deduction for losses disallowed no deduction shall be allowed in respect of any loss from the sale or exchange of property directly or indirectly between persons specified in any of the paragraphs of subsection b. No deduction shall be allowed in respect of any loss from the sale or exchange of property directly or indirectly between persons specified in any of the paragraphs of subsection b.

Statutes codes and regulations. 267 a 1 deduction for losses disallowed no deduction shall be allowed in respect of any loss from the sale or exchange of property directly or indirectly between persons specified in any of the paragraphs of subsection b. Table of contents retrieve by section number.

Woodmere Accountant Charged With Tax Fraud Herald Community Newspapers Www Liherald Com

4 21 1 Monitoring The Irs Program Internal Revenue Service

Https Www Kirkland Com Media Publications Article 2019 04 Planning At The Eleventh Hour Part Ii Trustsestates Planning At The Eleventh Hourpart Ii Pdf La En

Http Www Kirkland Com Sitefiles Kirkexp Publications 2582 Document1 Transactional 20guide 20to 20new 20code 20section 20197 Pdf

Partnership Taxation Who Owns Me Who Do I Own Toolbox Finance

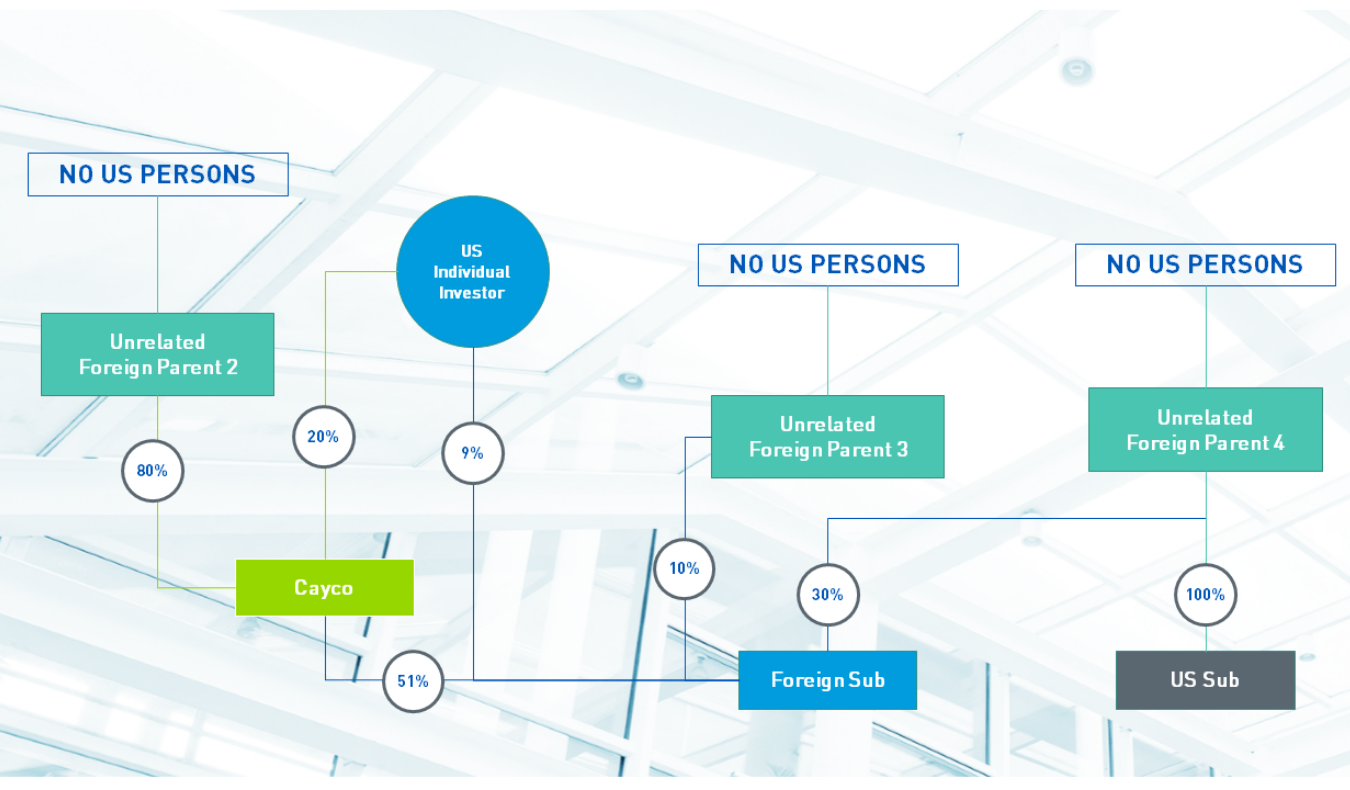

A Closer Look At The Repeal Of Section 958 B 4 Withum

Https Digitalcommons Usu Edu Cgi Viewcontent Cgi Article 1025 Context Rural Tax

Foreign Partners Celebrate More Relaxed Procedures Of Proposed Sec 1446 F Regs Alvarez Marsal Management Consulting Professional Services

Ars 1 A19 6129 3ars Htm Ars 2018 Annual Report Embracing Change Building On Our Mission A Letter From Kathleen Hyle Non Executive Board Chair 2018 Was A Year Of Significant Change For Bunge We Faced Challenges And At The Same Time Had

Https Www Alvarezandmarsal Com Sites Default Files 90507 Tax Pli Section 382 White Paper 03 Pdf

Proposed Rules Implementing Anti Hybrid Provisions Have Broad Reach Grant Thornton

3 13 62 Media Transport And Control Internal Revenue Service

Our Greatest Hits Tax Planning For Distributions In Kind Estates Trusts The Cpa Journal