Internal Revenue Code Section 104 A 2

Red Flags That Tempt The Tax Auditor Income Tax Brackets Trump Tax Plan Income Tax

Pin On Hard Money Loans

Account Suspended

Is Your 529 Savings Plan In The Red Tuition May Still Be Due How To Plan Education Savings Account 529 Plan

Jane Quinn Doe S Freedom From Fiction Accepted For Value A4v To Discharge Debt How To Fix Credit Debt Knowledge And Wisdom

3 12 179 Individual Master File Imf Unpostable Resolution Internal Revenue Service

Except in the case of amounts attributable to and not in excess of deductions allowed under section 213 relating to medical etc expenses for any prior taxable year gross income does not include 1 amounts received under workmen s compensation acts as compensation for personal injuries or sickness.

Internal revenue code section 104 a 2. Internal revenue code section 104 a 2 compensation for injuries or sickness. Internal revenue code 26 usca section 104. Section 104 a 2 also excludes damages not in excess of the amount paid for medical care described in section 213 d 1 a or b for emotional distress.

Received through prosecution of a legal suit or action or through a settlement agreement entered into in lieu of such prosecution 2. 104 a 3. 2 the amount of any damages other than punitive damages received whether by suit or.

104 a 2. The amount of any damages other than punitive damages received whether by suit or agreement and whether as lump sums or as periodic payments on account of personal physical injuries or physical sickness. Based on tort or tort type rights and 3.

The 1996 amendment added to irc 104 a 2 the word physical to the clause on account of personal physical injuries or physical sickness therefore in order for damages to be excludible from income the judgment or settlement must be derived from personal physical injuries or physical sickness. 2053 provided that. The amendments made by this section amending this section and section 692 of this title shall apply to taxable years ending on or after september 11 2001 effective date of 1996 amendment pub.

Internal revenue code section 104 a 2 excludes from gross income compensatory damages. 21 1996 110 stat.

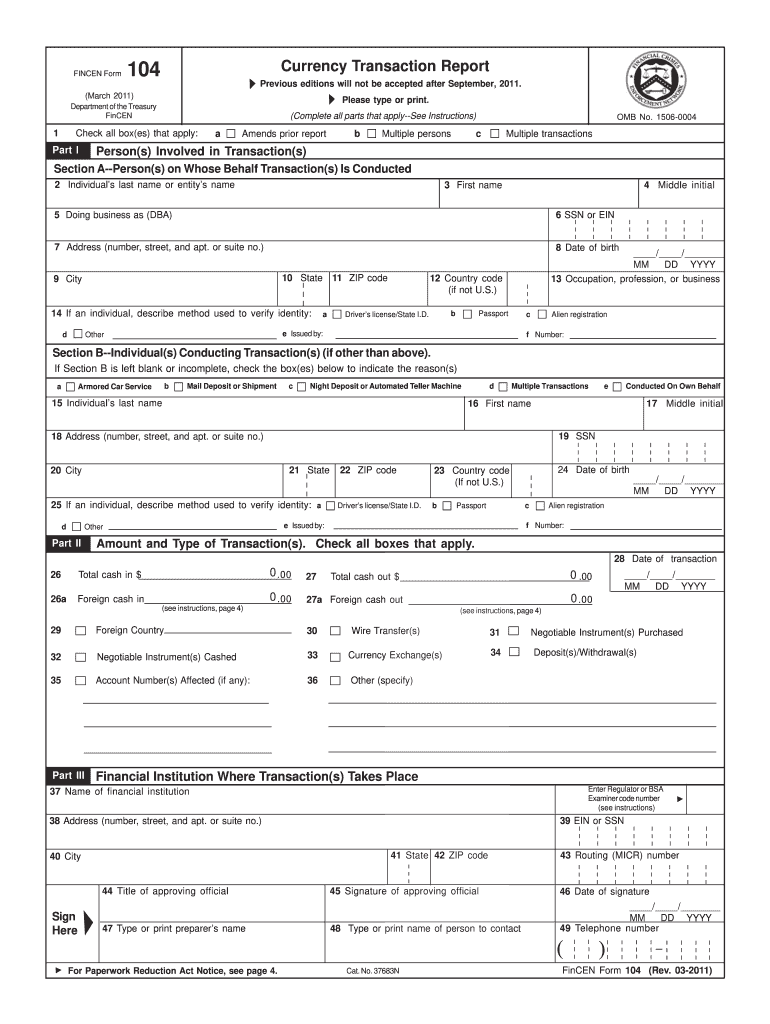

2011 2020 Form Fincen 104 Fill Online Printable Fillable Blank Pdffiller

Account Suspended Losing A Dog Shannon We The People

Account Suspended Height And Weight Medical Conditions Person

Account Suspended Miss Kelly Missing And Exploited Children Person

Account Suspended Houston Police Department Houston Police Get A Life

Kerry Jones Feb 7 2016 Jacksonville Fl Looking For Someone Pell City Jacksonville

Missing Ohio Miss Missing Posters

Infographic 10 Structured Settlement Terms Made Easy Design By Tinystarscreative Com Infographic Finance Make It Simple

Account Suspended In 2020 Eye Color African American Black African American

Us 1040 Tax Form The Us 1040 Individual Income Tax Return Form With Calculator Sponsored Individu Tax Forms Income Tax Return Capital Gains Tax

Account Suspended Losing A Dog Miss Missing Persons

Find Missing Michael Anthony Mcclain Michael Anthony Anthony Michael

Have You Seen Me Amber Alert Losing A Dog Looking For Someone